Key Takeaways

- Datadog's innovations in product offerings and AI observability aim to boost customer value and capture demand, potentially driving increased revenue growth.

- Strategic focus on expanding into cloud security and less mature geographies could lead to higher net margins and new revenue opportunities.

- Datadog's cautious revenue growth outlook and heavy investment in R&D and marketing pose risks to stable long-term earnings amidst potential customer behavior shifts.

Catalysts

About Datadog- Operates an observability and security platform for cloud applications in the United States and internationally.

- Datadog's focus on expanding its product offerings with innovations like Kubernetes autoscaling and OCI monitoring is expected to enhance its customer value proposition, potentially leading to increased revenue through more comprehensive platform adoption.

- The company highlighted a significant opportunity to grow its existing customer base, particularly within the Fortune 500, where the median ARR per customer suggests considerable room for growth. This potential increase in customer spend could meaningfully boost revenues over the coming years.

- With strategic moves into AI and LLM (Large Language Models) observability, Datadog positions itself to capture increasing demand as more companies integrate AI capabilities, potentially driving higher revenues from these emerging technologies.

- Datadog's growth strategy appears to leverage recent technology advances in cloud security, which could enhance its net margins by offering higher-value, integrated security solutions to customers, many of whom are shifting resources to improving overall cloud security posture.

- By expanding its sales and marketing teams and tapping into less mature geographies, Datadog expects to capture new revenue growth opportunities that could lead to higher net earnings as these investments start to contribute to growth in future periods.

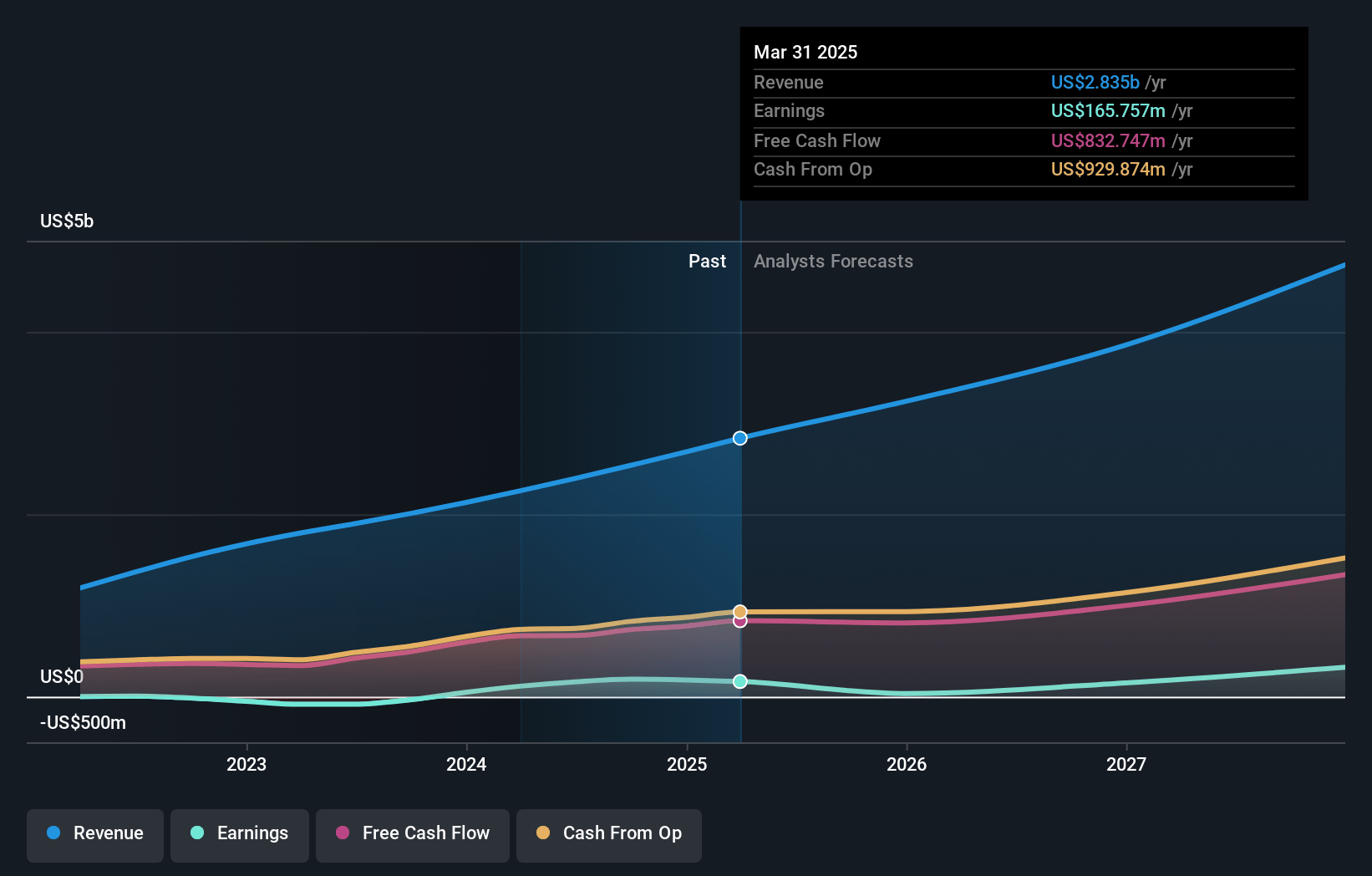

Datadog Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Datadog compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Datadog's revenue will grow by 17.3% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 6.8% today to 5.3% in 3 years time.

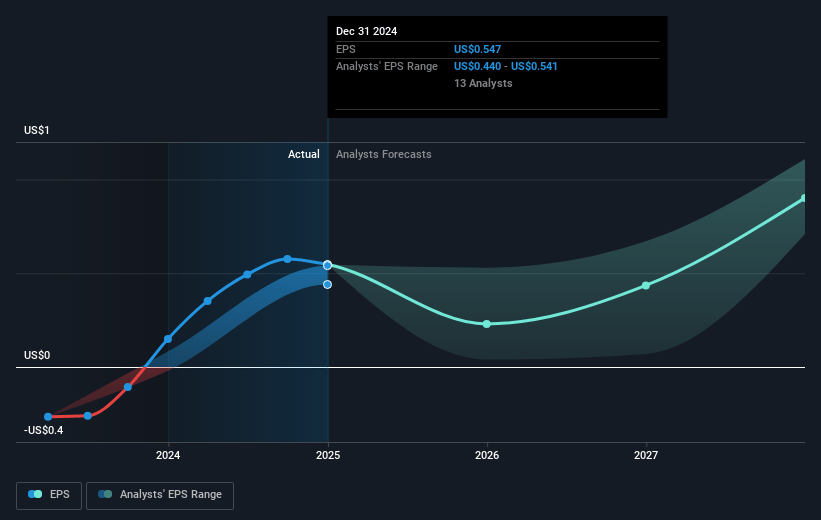

- The bearish analysts expect earnings to reach $228.0 million (and earnings per share of $0.71) by about April 2028, up from $183.7 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 253.0x on those 2028 earnings, up from 171.4x today. This future PE is greater than the current PE for the US Software industry at 29.6x.

- Analysts expect the number of shares outstanding to grow by 2.47% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.74%, as per the Simply Wall St company report.

Datadog Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Despite the increase in revenue, challenges such as cost-conscious customer behavior and potential optimization of cloud and observability usage could potentially affect Datadog's long-term revenue growth.

- The company's guidance for revenue growth in fiscal year 2025 is conservative at 18% to 19% year-over-year, down from previous levels, which could imply risks to revenue and earnings if growth rates do not accelerate beyond current levels.

- The possibility of large customers choosing to in-house their observability solutions, although currently economically irrational for most, poses a risk to future revenue if any decide to internalize these functions.

- With the company's heavy investment in sales and marketing and R&D set to grow at high rates, Datadog faces the risk that these investments may not immediately translate into proportionate increases in revenue, impacting net margins.

- The volatility in revenue growth, especially among AI native customers as they renew contracts on different terms, could lead to fluctuations in usage and revenue, posing a risk to stable earnings growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Datadog is $125.37, which represents one standard deviation below the consensus price target of $149.25. This valuation is based on what can be assumed as the expectations of Datadog's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $230.0, and the most bearish reporting a price target of just $115.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $4.3 billion, earnings will come to $228.0 million, and it would be trading on a PE ratio of 253.0x, assuming you use a discount rate of 7.7%.

- Given the current share price of $91.88, the bearish analyst price target of $125.37 is 26.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is an employee of Simply Wall St, but has written this narrative in their capacity as an individual investor. AnalystLowTarget holds no position in NasdaqGS:DDOG. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. This narrative is general in nature and explores scenarios and estimates created by the author. The narrative does not reflect the opinions of Simply Wall St, and the views expressed are the opinion of the author alone, acting on their own behalf. These scenarios are not indicative of the company's future performance and are exploratory in the ideas they cover. The fair value estimate's are estimations only, and does not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that the author's analysis may not factor in the latest price-sensitive company announcements or qualitative material.