Key Takeaways

- CCC's strategic partnerships and tech innovations in AI-driven insurance transformations position it for significant revenue growth and market expansion.

- New acquisitions and solution rollouts, like IX Cloud, aim to drive adoption and support long-term earnings through expanded offerings and efficient implementations.

- Slowing growth, margin pressures, and reliance on non-GAAP measures could challenge CCC's financial health and affect future revenue and earnings perceptions.

Catalysts

About CCC Intelligent Solutions Holdings- Operates as a software as a service (SaaS) company for the property and casualty insurance economy in the United States and China.

- The digitization of the insurance economy and CCC's positioning as a key partner for AI-driven transformation offers significant potential for revenue growth as more claims and repair processes are expected to be managed using CCC's solutions.

- The acquisition of EvolutionIQ and its integration offers potential to expand CCC's addressable markets into disability and workers' compensation, complementing existing capabilities and driving revenue growth through new customer additions.

- The introduction of IX Cloud and AI-enabled workflows aims to accelerate customer adoption of new solutions, potentially improving revenue velocity as more insurers and repair facilities leverage these tools.

- Emerging solutions, such as Estimate-STP and Build Sheets, are the fastest-growing portion of CCC's portfolio, representing significant future revenue drivers as their adoption scales and inflection points are achieved.

- Continued investment in change management and realignment of customer-facing functions, combined with leadership changes, are expected to support clients' transformations and drive long-term earnings growth by enhancing the efficiency and effectiveness of solution rollouts.

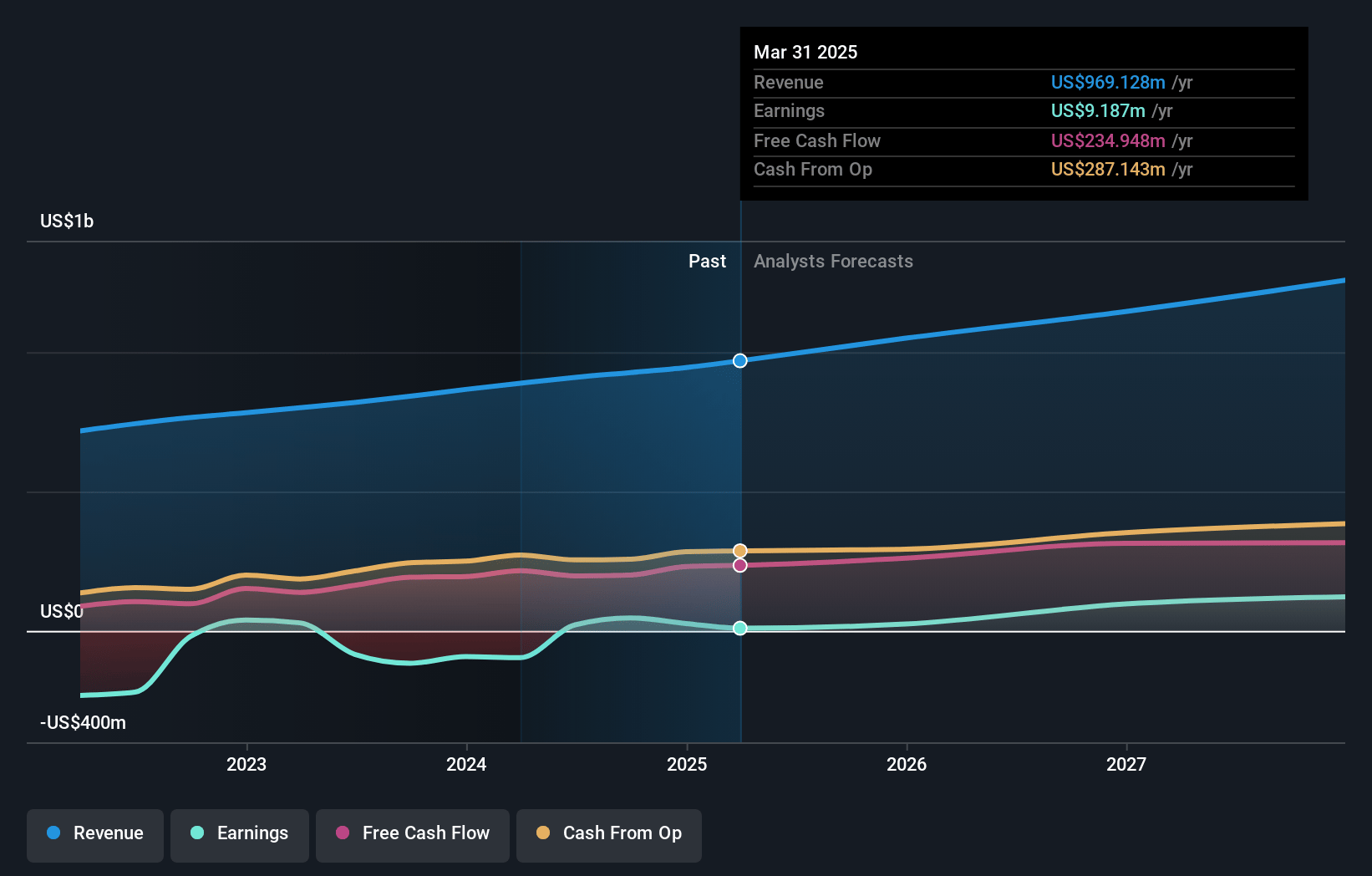

CCC Intelligent Solutions Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming CCC Intelligent Solutions Holdings's revenue will grow by 9.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 2.8% today to 14.8% in 3 years time.

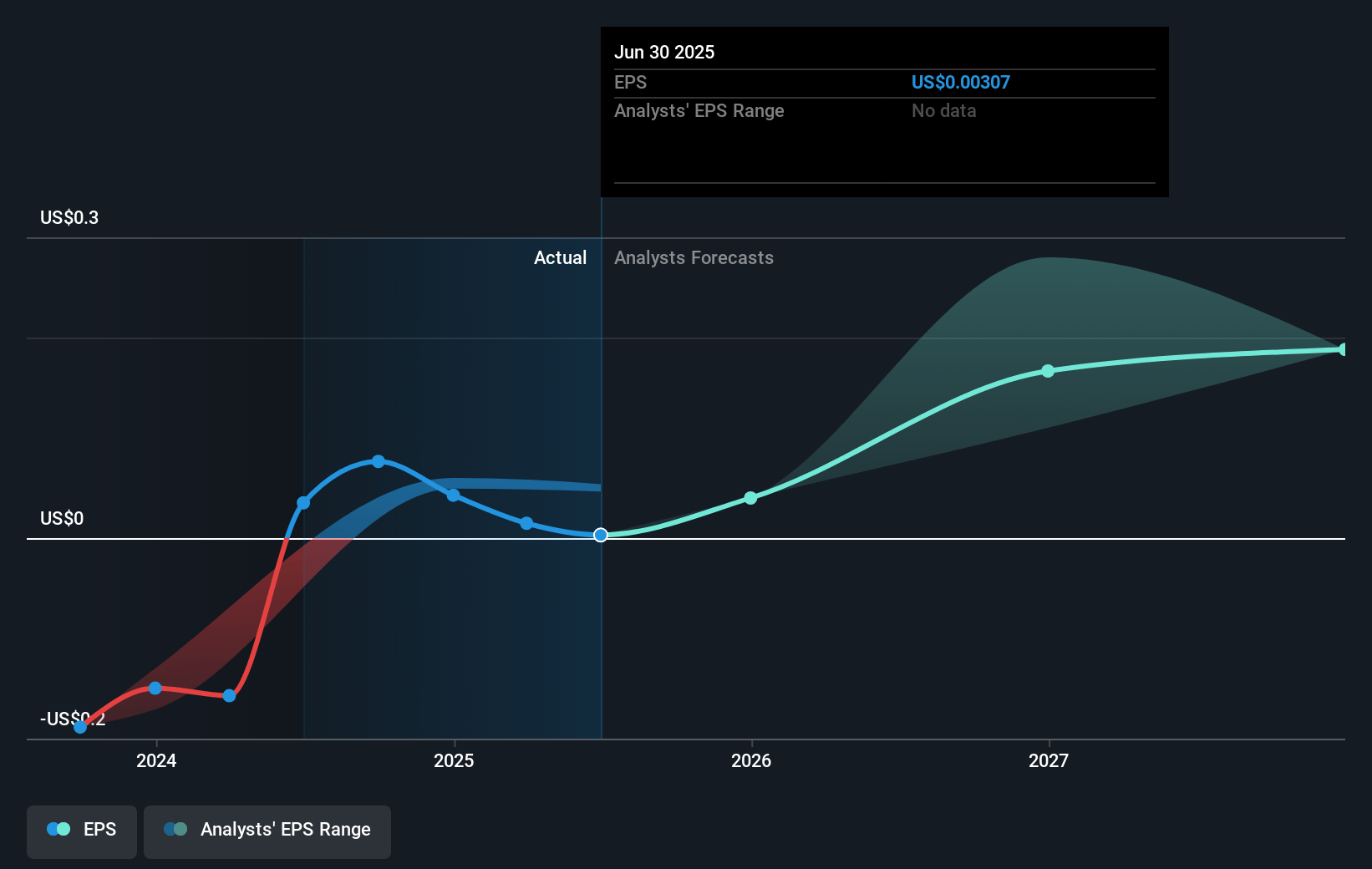

- Analysts expect earnings to reach $184.9 million (and earnings per share of $0.28) by about April 2028, up from $26.1 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 68.7x on those 2028 earnings, down from 217.0x today. This future PE is greater than the current PE for the US Software industry at 29.6x.

- Analysts expect the number of shares outstanding to grow by 6.87% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.99%, as per the Simply Wall St company report.

CCC Intelligent Solutions Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's slowing organic growth in 2025, projected at the lower end of their 7% to 10% long-term range, may suggest challenges in accelerating revenue growth, potentially impacting future revenue projections.

- The integration and moderate EBITDA loss from EvolutionIQ could lead to margin pressures, as margins are expected to decline by about 200 basis points, affecting net earnings in the short term.

- Continued softness in claims volumes, with a significant consumer self-pay segment, may affect the company's revenue performance, especially since much of CCC's solutions are tied to claims handling.

- Potentially slower customer adoption and ramp-up of new AI solutions, due to change management complexities, might delay revenue realization and impact the net margins.

- The reliance on non-GAAP financial measures and adjustments like stock-based compensation, resulted in a projected 2025 share-based compensation increase, which could dilute earnings and affect the perception of financial health.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $12.539 for CCC Intelligent Solutions Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $14.0, and the most bearish reporting a price target of just $11.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.3 billion, earnings will come to $184.9 million, and it would be trading on a PE ratio of 68.7x, assuming you use a discount rate of 8.0%.

- Given the current share price of $8.61, the analyst price target of $12.54 is 31.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.