Key Takeaways

- Strategic leadership changes and partnerships aim to enhance sales and revenue growth by expanding market reach and customer engagement.

- New initiatives and certifications target government sectors and broad customer bases, driving potential revenue through innovative financial solutions and expanded services.

- Delayed deal closures and FX headwinds could impact revenue growth, while infrastructure investments and economic uncertainties limit short-term profitability.

Catalysts

About BlackLine- Provides cloud-based solutions to automate and streamline accounting and finance operations in the United States and internationally.

- BlackLine's new Chief Commercial Officer, Stuart Van Houten, is expected to enhance sales execution, especially with enterprise customers and strategic partnerships like those with SAP, potentially driving revenue growth.

- The ongoing strategic evolution, including the launch of Studio360, is intended to position BlackLine as a leader in digital finance transformation, which could boost revenue through increased adoption by CFOs and CIOs.

- The pursuit of FedRAMP certification is a step toward capturing new market opportunities in the public sector, offering potential revenue growth by expanding service offerings to government agencies.

- The new packaging and pricing model is gaining early traction and is expected to drive revenue growth by allowing BlackLine to reach broader customer groups beyond traditional accounting teams within organizations.

- Expanding partnerships with global system integrators and companies like Workday is expected to increase BlackLine's market reach and could positively impact net margins through collaborative go-to-market strategies.

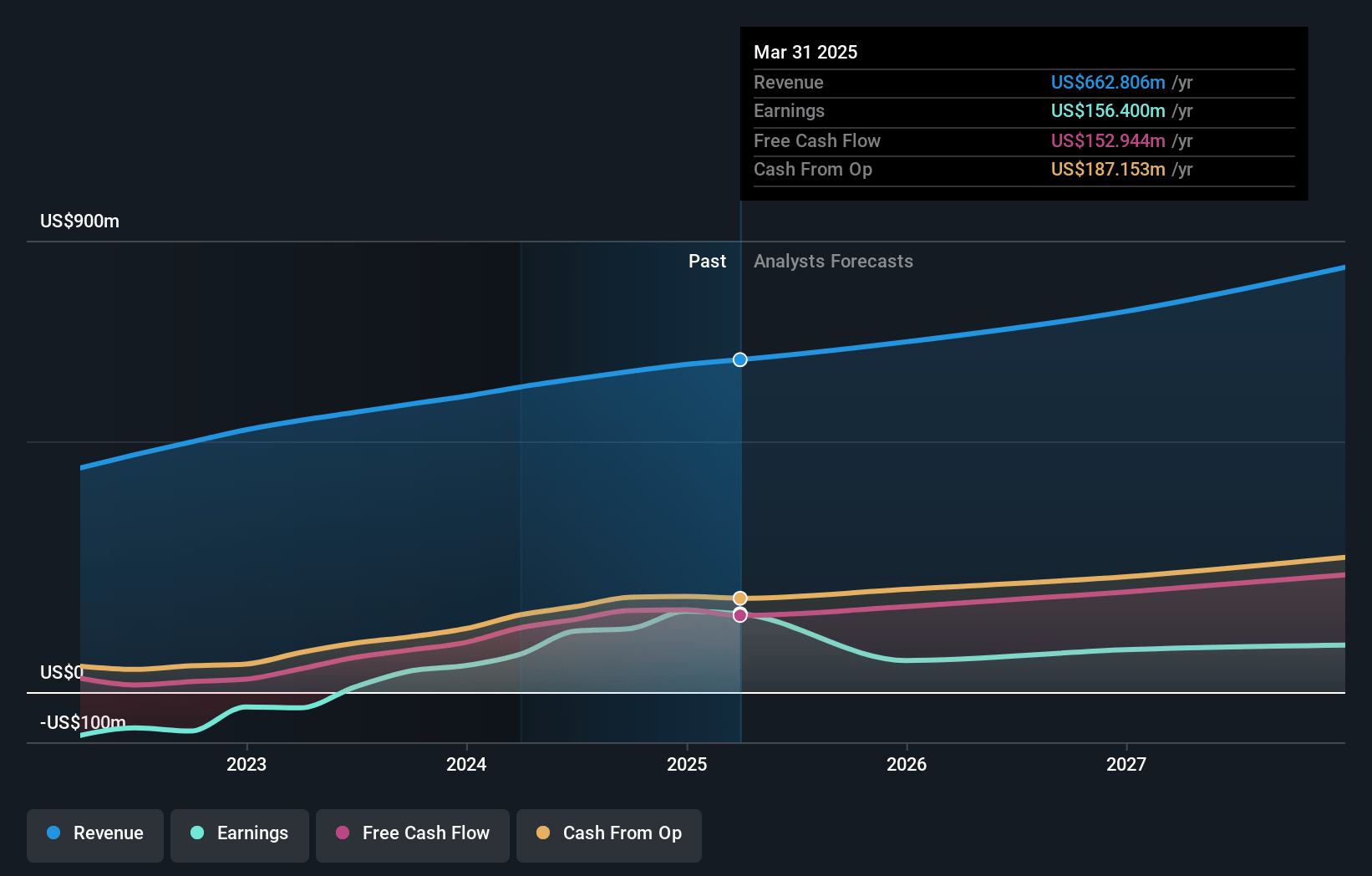

BlackLine Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming BlackLine's revenue will grow by 9.4% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 24.7% today to 5.4% in 3 years time.

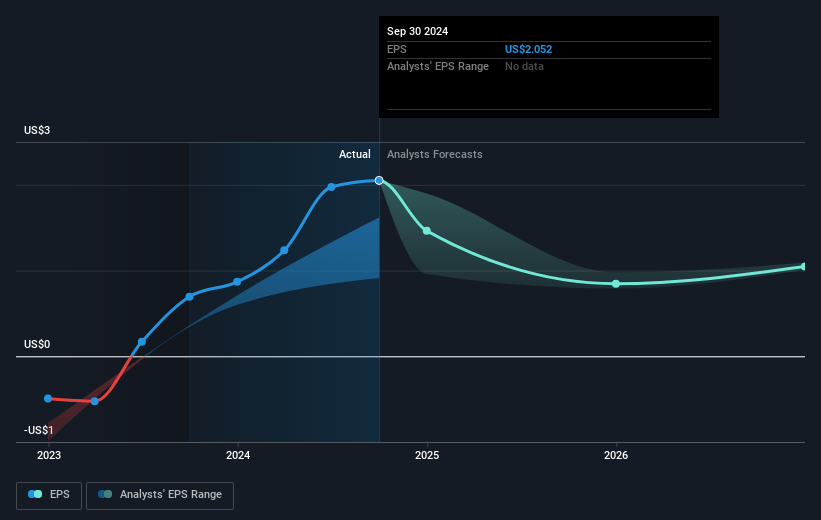

- Analysts expect earnings to reach $45.9 million (and earnings per share of $0.52) by about March 2028, down from $161.2 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 116.1x on those 2028 earnings, up from 19.3x today. This future PE is greater than the current PE for the US Software industry at 28.2x.

- Analysts expect the number of shares outstanding to grow by 1.61% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.13%, as per the Simply Wall St company report.

BlackLine Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Deal velocity, especially in larger late-stage opportunities, slowed in Q4, causing some deals to extend into 2025. This could impact revenue and earnings as delays in closing deals push expected revenue into future periods.

- Foreign exchange (FX) impacts, particularly from a stronger U.S. dollar, represented an approximate 1-point headwind to revenue growth and a 2-point headwind to annual recurring revenue (ARR) and net retention rate (NRR), affecting both revenues and net margins.

- Concerns about tariffs and economic uncertainty could lead to customer hesitance to make decisions swiftly, potentially impacting future revenue and ongoing deals.

- Challenges in executing pricing and packaging changes over the next three to four years could lead to slower-than-expected adoption by customers and result in lower-than-anticipated revenue growth.

- The ongoing investment in FedRAMP certification and other infrastructure projects represents a cost that will have a half-point drag on gross margin, which could limit short-term profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $64.8 for BlackLine based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $80.0, and the most bearish reporting a price target of just $51.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $855.6 million, earnings will come to $45.9 million, and it would be trading on a PE ratio of 116.1x, assuming you use a discount rate of 8.1%.

- Given the current share price of $49.58, the analyst price target of $64.8 is 23.5% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.