Key Takeaways

- Strategic shift towards broader advertising and self-service capabilities aims to drive revenue growth and operational efficiency, enhancing net margins.

- Focus on AI enhancements and core high-margin advertising operations suggests improved earnings and monetization rates.

- Transition challenges and cost pressures could hinder revenue growth, while divestitures and e-commerce reliance introduce uncertainty in operational stability.

Catalysts

About AppLovin- Engages in building a software-based platform for advertisers to enhance the marketing and monetization of their content in the United States and internationally.

- AppLovin's expansion beyond gaming into broader advertising categories, such as e-commerce, is expected to drive future revenue growth as it taps into a larger advertiser base, allowing for incremental demand from over 10 million potential businesses worldwide.

- The transition to a pure advertising platform with a focus on productivity, automation, and lean operations could enhance net margins, as indicated by the increase in adjusted EBITDA per employee. This operational efficiency aligns with financial growth.

- The development of self-service capabilities is a strategic move to scale the business by making it more accessible to a wide range of advertisers, which could lead to increased revenues as more businesses join the platform.

- The divestiture of the Apps business to focus resources on the core advertising operations suggests a strategic shift to high-margin business segments, potentially improving overall earnings and net margins.

- Enhancements in AI and machine learning models for ad placements are anticipated to further improve monetization rates and advertising effectiveness, supporting sustained improvements in revenue growth and earnings.

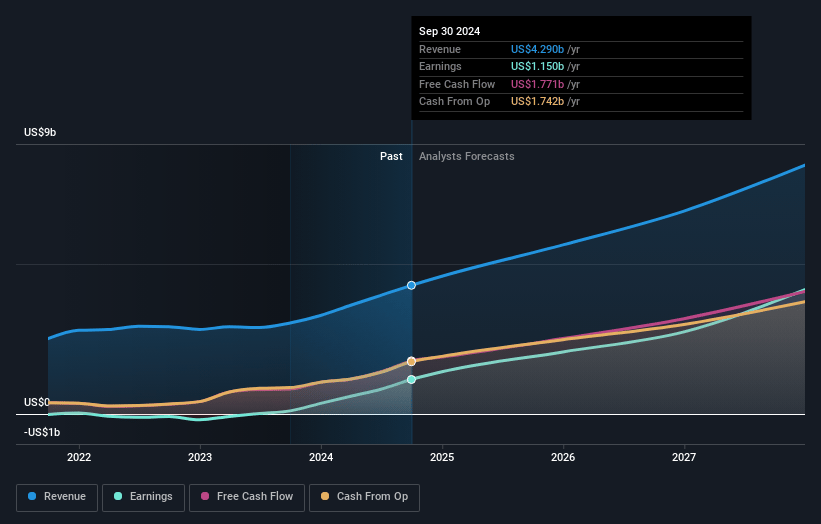

AppLovin Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on AppLovin compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming AppLovin's revenue will grow by 10.7% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 33.5% today to 50.7% in 3 years time.

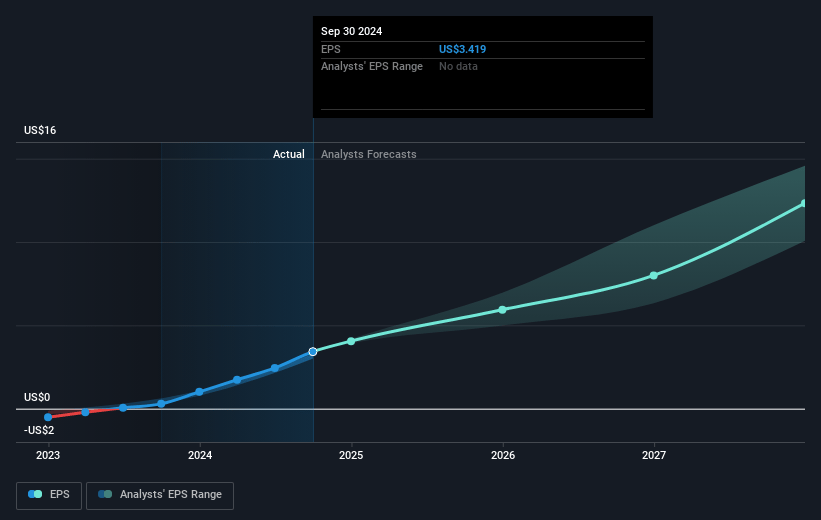

- The bearish analysts expect earnings to reach $3.2 billion (and earnings per share of $9.49) by about April 2028, up from $1.6 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 48.8x on those 2028 earnings, down from 51.4x today. This future PE is greater than the current PE for the US Software industry at 30.0x.

- Analysts expect the number of shares outstanding to grow by 3.33% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.7%, as per the Simply Wall St company report.

AppLovin Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The transition to a new advertising platform is not yet fully scalable due to a lack of automated tools and self-service capabilities, which could impact potential revenue growth.

- The divestiture of the Apps business, generating $373 million in revenue with a 19% margin, might reduce overall revenue stability during the transition phase.

- Increasing data center and GPU costs that led to lower than usual quarter-over-quarter flow-through from revenue to adjusted EBITDA could pressure net margins if not controlled effectively.

- The need to remain diligent and lean to not hire extensively could limit operational capacity, possibly affecting future earnings if demand increases beyond current staffing capabilities.

- Relying heavily on e-commerce success for future growth remains uncertain and unpredictable, and overestimating its contribution might lead to unanticipated revenue shortfalls.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for AppLovin is $337.35, which represents one standard deviation below the consensus price target of $459.34. This valuation is based on what can be assumed as the expectations of AppLovin's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $650.0, and the most bearish reporting a price target of just $200.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $6.4 billion, earnings will come to $3.2 billion, and it would be trading on a PE ratio of 48.8x, assuming you use a discount rate of 7.7%.

- Given the current share price of $238.22, the bearish analyst price target of $337.35 is 29.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is an employee of Simply Wall St, but has written this narrative in their capacity as an individual investor. AnalystLowTarget holds no position in NasdaqGS:APP. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. This narrative is general in nature and explores scenarios and estimates created by the author. The narrative does not reflect the opinions of Simply Wall St, and the views expressed are the opinion of the author alone, acting on their own behalf. These scenarios are not indicative of the company's future performance and are exploratory in the ideas they cover. The fair value estimate's are estimations only, and does not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that the author's analysis may not factor in the latest price-sensitive company announcements or qualitative material.