Last Update 27 Apr 26

Fair value Decreased 1.83%ADSK: Margin Expansion And Sales Model Shift Will Support Future Rebound

The Analyst Price Target for Autodesk has been adjusted modestly to $325.55 from $331.62 as analysts balance Q4 strength, solid FY27 guidance and margin support with lower sector multiples and recent target cuts across several covering firms.

Analyst Commentary

Recent research on Autodesk reflects a split view, with many firms trimming price targets while still highlighting execution, margin potential and long term growth initiatives, and at least one downgrade pointing to sector and sentiment pressures.

Bullish Takeaways

- Bullish analysts highlight strong Q4 results and an initial FY27 outlook that they describe as better than expected, with commentary pointing to 9% to 10% constant currency revenue growth after adjusting for the new transaction model and operating margin expansion of about 75 basis points at the midpoint.

- Several firms maintain positive ratings even as they recalibrate targets, citing solid execution across Autodesk's portfolio and the view that recent go to market changes could be absorbed without major disruption.

- Some research points to Autodesk as relatively insulated from perceived AI related risk within software, with at least one large firm grouping the stock among Buy rated names that it believes are well placed to embed AI into existing platforms.

- Target increases from firms such as JPMorgan and others emphasize continued confidence in Autodesk's margin trajectory, with one analyst referencing comfort in margins pacing toward a 41% target for FY29.

Bearish Takeaways

- Bearish analysts and more cautious research pieces have reduced price targets, in several cases tying cuts directly to broad software multiple compression rather than company specific issues.

- One downgrade at a large global bank underscores concerns that sector sentiment for software has weakened, with vertical SaaS names reacting more to headlines than fundamentals, which can weigh on Autodesk's valuation even when execution is described as solid.

- Some commentary points to mixed reseller survey feedback ahead of results, as well as expectations that investors will focus closely on FY27 guidance details and the impact of Autodesk's sales and marketing optimization plans.

- A few firms frame their lower targets around caution on macro factors and the need for conservatism in guidance, which, in their view, justifies using lower sector multiples despite positive feedback from customer checks.

What's in the News

- Autodesk has filed a lawsuit against Alphabet's Google, alleging that Google's "Flow" software infringes Autodesk's "Flow" trademark for visual effects and production management tools that Autodesk says it has used since September 2022, with both offerings aimed at similar media and entertainment customers (Reuters).

- Prestige Estates Projects Limited announced a three year partnership to use Autodesk Forma, Autodesk Construction Cloud and the Autodesk AEC Collection across its enterprise, with plans to standardize workflows, adopt 4D and 5D capabilities and create a connected digital ecosystem across its real estate portfolio.

- Globant has been named an Autodesk Tandem Digital Twin Solution Provider, expanding a 15 year collaboration to help deploy Autodesk's cloud based digital twin platform across airports, smart buildings, manufacturing facilities and logistics environments worldwide.

- Autodesk issued guidance for the first quarter ending April 30, 2026, with expected revenue of US$1,885m to US$1,900m and GAAP EPS of US$1.68 to US$1.83, and for the full fiscal year ending January 31, 2027, with expected revenue of US$8.1b to US$8.17b, GAAP operating margin of 26% to 28% and GAAP EPS of US$7.76 to US$8.39.

- The company reported that from November 1, 2025 to January 31, 2026 it repurchased 1,135,000 shares for US$330.82m, completing a total of 9,154,600 shares bought back for US$2,516.02m under the repurchase program announced on November 22, 2022.

Valuation Changes

- Fair Value has edged lower, with the model output moving from $331.62 to $325.55.

- Discount Rate has risen slightly from 8.55% to 8.60%, implying a modestly higher required return in the model.

- Revenue Growth assumption is broadly unchanged, moving from 11.36% to 11.39%.

- Net Profit Margin assumption has increased modestly, from 24.04% to 24.40%.

- Future P/E multiple has been trimmed from 35.82x to 34.66x, reflecting a lower valuation ratio applied to projected earnings.

Key Takeaways

- Expanding cloud and AI-driven solutions, plus SaaS models, are enhancing recurring revenue, margin stability, and differentiation in core AEC markets.

- Strategic acquisitions and focus on sustainability are growing Autodesk's product ecosystem, customer value, and positioning as a key enabler of digital transformation.

- Rising competition from open-source and alternative platforms, evolving customer preferences, and regulatory challenges threaten Autodesk's pricing power, market share, and long-term profitability.

Catalysts

About Autodesk- Provides 3D design, engineering, and entertainment technology solutions worldwide.

- Strength in Autodesk's core AEC (Architecture, Engineering, Construction) markets is driven by sustained investment in infrastructure, data centers, and industrial buildings, underpinned by increased global urbanization and infrastructure buildout, which is likely to fuel ongoing growth in Autodesk's addressable market and support robust revenue expansion.

- Accelerating adoption of cloud-based platforms-such as Autodesk Construction Cloud and Fusion 360-and ongoing rollout of subscription and SaaS models are increasing recurring revenue, improving revenue visibility, and enhancing net margin stability due to higher operating leverage and sales efficiency improvements.

- Continued innovation and integration of AI-driven tools (e.g., generative design, AutoConstrain) and industry-specific foundation models are boosting customer productivity and differentiating Autodesk's offerings, supporting premium pricing and driving margin expansion and long-term earnings growth.

- Focused strategic tuck-in acquisitions and strong cross-sell activity are expanding Autodesk's product ecosystem, allowing deeper integration and higher customer lifetime value, raising the potential for long-term revenue acceleration and resilient net margin improvement.

- Rising importance of sustainability and regulatory-driven climate action, together with increased demand for digitally-enabled energy efficiency solutions, are positioning Autodesk as an essential technology provider for customers' sustainable transformation efforts, driving higher-value software adoption and supporting both topline growth and higher-margin service offerings.

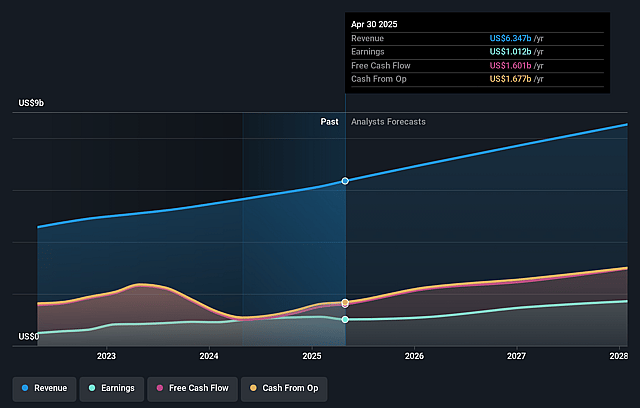

Autodesk Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Autodesk's revenue will grow by 11.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 15.6% today to 24.4% in 3 years time.

- Analysts expect earnings to reach $2.4 billion (and earnings per share of $11.46) by about April 2029, up from $1.1 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $2.8 billion in earnings, and the most bearish expecting $2.2 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 34.7x on those 2029 earnings, down from 44.6x today. This future PE is greater than the current PE for the US Software industry at 30.5x.

- Analysts expect the number of shares outstanding to decline by 1.4% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.6%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The increasing adoption of open-source and lower-cost software solutions globally could erode Autodesk's pricing power, as evidenced by customer examples switching from competitive solutions, potentially leading to price compression and pressure on long-term revenue growth.

- Ongoing customer adaptation to the new transaction model and frequent migrations may cause friction, slowing net new customer acquisition and risking higher churn rates, which can negatively affect recurring revenue streams and overall earnings.

- Rapid advances in AI and generative design-areas in which Autodesk is investing but where emerging competitors and start-ups are active-could enable new entrants to leapfrog Autodesk's technology if Autodesk's own innovation pace slows, threatening its competitive moat and long-term margins.

- Heightened data privacy and global regulatory requirements, as Autodesk continues its transition to cloud-based and AI-enabled solutions, may increase compliance costs and operational complexity, creating headwinds for operating margins over time.

- Accelerated adoption of alternative, agile, or in-house software platforms-particularly as the construction industry explores modular and industrialized construction methods-may bypass legacy Autodesk solutions, constraining Autodesk's total addressable market in its traditional AEC business and impacting future revenue growth.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $325.55 for Autodesk based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $456.0, and the most bearish reporting a price target of just $246.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $10.0 billion, earnings will come to $2.4 billion, and it would be trading on a PE ratio of 34.7x, assuming you use a discount rate of 8.6%.

- Given the current share price of $237.44, the analyst price target of $325.55 is 27.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Autodesk?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.