Narratives are currently in beta

Key Takeaways

- Smartphone upgrades and AI advancements could drive higher demand for RF solutions, boosting future revenue and earnings.

- Strong design wins and cash flow support strategic investments for long-term revenue growth, particularly in next-gen WiFi and automotive sectors.

- High inventory levels and concentration risk from a major customer pose potential revenue and earnings volatility for Skyworks Solutions.

Catalysts

About Skyworks Solutions- Designs, develops, manufactures, and markets proprietary semiconductor products in the United States, China, South Korea, Taiwan, Europe, the Middle East, Africa, and the rest of Asia-Pacific.

- Skyworks Solutions is well-positioned to capitalize on a smartphone upgrade cycle driven by advancements in AI, which could increase demand for high-performance RF solutions, thereby boosting future revenue and earnings.

- The integration of advanced packaging in mobile platforms, reducing footprint and increasing energy efficiency, suggests potential improvements in net margins through cost reductions and operational efficiencies.

- Securing design wins for high-content, next-gen WiFi 6E and 7 systems indicates an upcoming period of revenue growth, as these products carry higher dollar content than previous generations.

- The company's strong design pipeline in automotive markets, including 5G front-end modules and digital isolators, even amidst current muted demand, signals potential revenue growth as the automotive sector recovers.

- Skyworks' solid free cash flow generation positions it to invest in technology and product roadmaps, potentially driving long-term revenue growth and enhanced earnings per share through strategic R&D and capital investments.

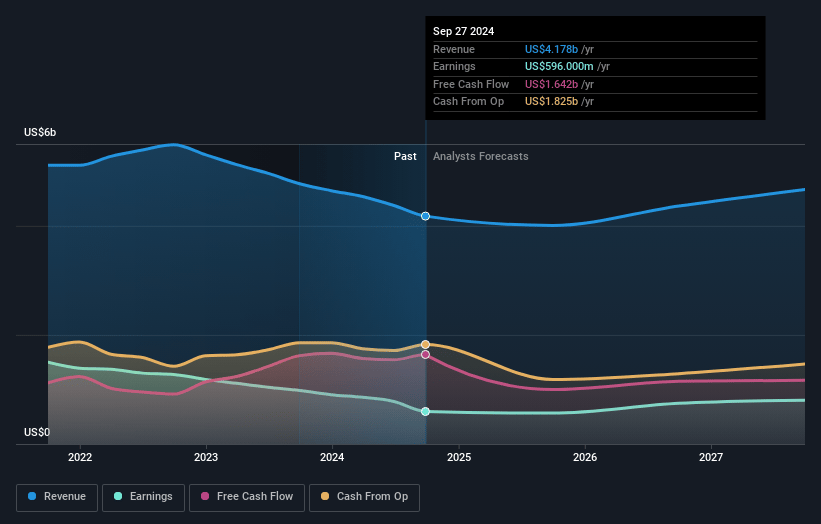

Skyworks Solutions Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Skyworks Solutions's revenue will grow by 3.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 14.3% today to 17.4% in 3 years time.

- Analysts expect earnings to reach $809.5 million (and earnings per share of $5.3) by about January 2028, up from $596.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $1.1 billion in earnings, and the most bearish expecting $564 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 22.5x on those 2028 earnings, down from 24.9x today. This future PE is lower than the current PE for the US Semiconductor industry at 31.8x.

- Analysts expect the number of shares outstanding to decline by 1.53% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.18%, as per the Simply Wall St company report.

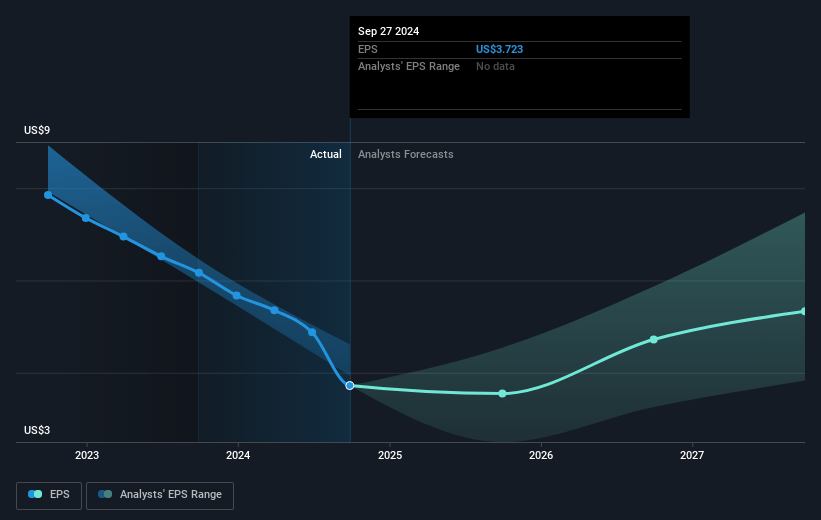

Skyworks Solutions Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- High inventory levels in traditional data centers and wireless infrastructure are delaying recovery, which may negatively impact revenue and earnings in those segments.

- Global demand in automotive and industrial markets remains muted as companies work to reduce excess inventory, potentially affecting revenue growth and net margins in these sectors.

- Broad markets show uneven demand and excess inventory in industrial, automotive, and networking segments, which could lead to lower than anticipated revenue and slower recovery.

- Continued under-shipment of natural demand due to high inventory might affect revenue growth and gross margins in the near term.

- Skyworks has significant exposure to its largest customer (around 69% of total revenue), which poses concentration risk and potential volatility in revenue and earnings if demand dynamics change unfavorably.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $94.78 for Skyworks Solutions based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $120.0, and the most bearish reporting a price target of just $72.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $4.7 billion, earnings will come to $809.5 million, and it would be trading on a PE ratio of 22.5x, assuming you use a discount rate of 8.2%.

- Given the current share price of $92.66, the analyst's price target of $94.78 is 2.2% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives