Narratives are currently in beta

Key Takeaways

- Growth in OLED markets through increased device adoption and expanded production is expected to drive future revenue.

- Innovations in phosphorescent blue materials and strategic R&D initiatives aim to enhance revenue and improve product margins.

- Economic uncertainties and delayed product innovations may lead to volatility in earnings and potential revenue growth challenges.

Catalysts

About Universal Display- Engages in the research, development, and commercialization of organic light emitting diode (OLED) technologies and materials for use in display and solid-state lighting applications in the United States and internationally.

- Expansion in the OLED market, driven by growth in OLED AR/VR devices, smart watches, smartphones, IT, automotive, and TVs, is expected to contribute to future revenue growth as device adoption increases.

- Investments in new OLED production facilities, such as Visionox's and Samsung Display's significant capital expenditures in OLED manufacturing capacities, are expected to increase supply capability and drive revenue.

- Development and future commercialization of phosphorescent blue emissive materials, which offers significant industry benefits, are anticipated to positively impact future revenue and earnings.

- Strategic research and development initiatives and customer collaborations aim to drive innovation and improve product offerings, likely enhancing revenue and improving margins through advanced materials and technology.

- Significant investments are being made in the mid-sized OLED segment, such as for IT and automotive applications, projected to contribute to revenue increases as these nascent markets expand and develop.

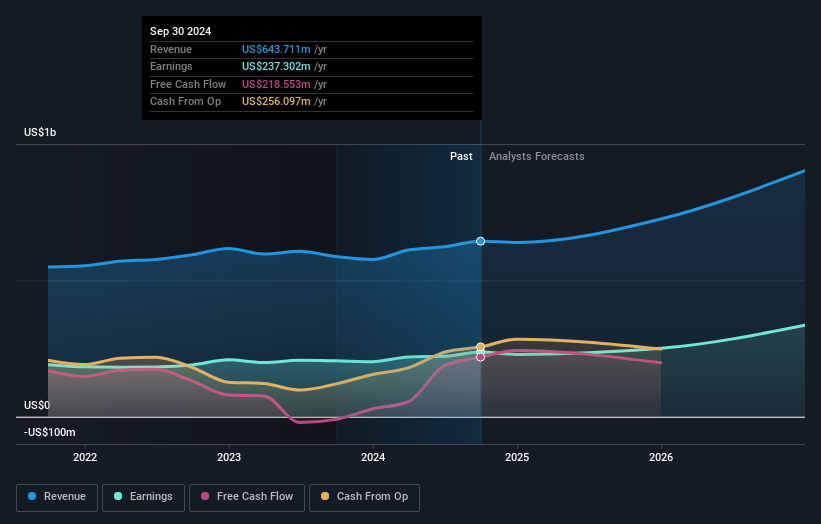

Universal Display Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Universal Display's revenue will grow by 14.1% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 36.9% today to 35.2% in 3 years time.

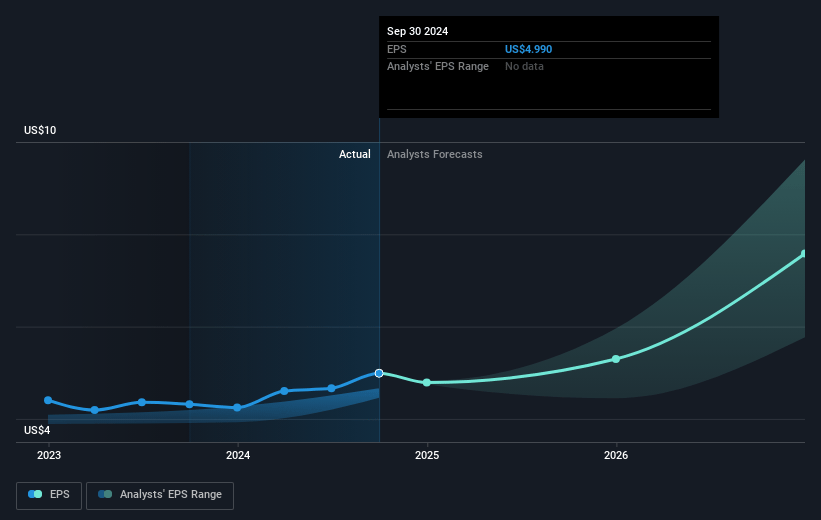

- Analysts expect earnings to reach $336.3 million (and earnings per share of $7.76) by about January 2028, up from $237.3 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $385.3 million in earnings, and the most bearish expecting $239 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 34.4x on those 2028 earnings, up from 30.8x today. This future PE is greater than the current PE for the US Semiconductor industry at 31.8x.

- Analysts expect the number of shares outstanding to decline by 2.96% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.93%, as per the Simply Wall St company report.

Universal Display Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's revenue forecast for 2024 has been revised downward due to lower customer forecasts for Q4, indicating potential weak demand and impact on future revenue growth.

- Material sales, an important revenue source, have decreased compared to the previous year’s quarter, which could negatively affect net margins if the trend continues.

- There is uncertainty around the timing of commercial availability and adoption of the company's phosphorescent blue material, which could delay potential revenue gains from this innovation.

- Inventory adjustments and changes in customer purchasing patterns signal potential volatility in near-term earnings, reflecting supply chain or demand-side issues.

- Economic conditions and consumer sentiment in certain global markets may negatively impact customer orders, leading to possible revenue fluctuations or reductions.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $213.84 for Universal Display based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $260.0, and the most bearish reporting a price target of just $165.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $956.3 million, earnings will come to $336.3 million, and it would be trading on a PE ratio of 34.4x, assuming you use a discount rate of 7.9%.

- Given the current share price of $153.97, the analyst's price target of $213.84 is 28.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives