Last Update 01 Dec 25

NVMI: Increased DRAM Fab Spending Will Strengthen Upcoming AI Market Position

Nova's analyst price target has been raised from $300 to $390. This change reflects an improved outlook and increased optimism among analysts following recent industry discussions and signs of stronger demand in the AI and DRAM sectors.

Analyst Commentary

Analysts have shared a mix of optimism and caution following updates from recent industry events and company meetings, impacting Nova's valuation outlook and growth prospects.

Bullish Takeaways

- Bullish analysts are encouraged by near-term signs of improved investment in DRAM fabrication, which could drive stronger demand for Nova's offerings.

- There have been notable advancements in Nova’s positioning within the AI computing market, suggesting a potential for accelerated growth and enhanced competitive advantage.

- The raised price target reflects growing confidence in management’s execution and the company’s ability to capitalize on semiconductor industry trends.

- Optimism around capital expenditures in wafer fab equipment signals the possibility of sustained revenue growth for Nova.

Bearish Takeaways

- Bearish analysts caution that current expectations for 2026 wafer fab equipment spending might be overly optimistic, posing a risk to long-term forecasts and valuation multiples.

- Execution risk remains a concern as the company seeks to scale within highly competitive AI and DRAM markets.

- Sustaining momentum in a volatile macroeconomic environment may prove challenging for Nova, impacting both top-line growth and profitability.

- Analysts also note the need for continued innovation to maintain and improve the firm's market position, particularly as industry competition intensifies.

What's in the News

- Nova Ltd. issued fourth quarter 2025 guidance, expecting revenue between $215 million and $225 million, with diluted GAAP EPS projected at $1.77 to $1.95 (Corporate Guidance).

- The company announced its ELIPSON materials metrology solution was selected as Tool of Record by a global foundry leader for advanced Gate-All-Around manufacturing. This marks a major milestone as deployments expand in high-volume production settings (Client Announcements).

- Nova Ltd. was added to the PHLX Semiconductor Sector Index, increasing its visibility within the semiconductor investment landscape (Index Constituent Adds).

Valuation Changes

- Fair Value remains unchanged at $365.83 per share, reflecting a stable assessment of Nova's intrinsic worth.

- Discount Rate has decreased slightly from 14.20% to 13.96%, which indicates a marginal reduction in perceived investment risk.

- Revenue Growth projection is stable and holds at approximately 14.44% annually.

- Net Profit Margin has edged down modestly, from 28.95% to 28.81%.

- Future P/E ratio has decreased marginally, from 45.65x to 45.58x.

Key Takeaways

- Demand for Nova's advanced metrology and analytics solutions is rising due to semiconductor complexity and global industry investments, supporting broad, diversified growth.

- Product innovation and recurring, high-margin services are strengthening customer relationships and margins, positioning Nova for increased market share and operational leverage.

- Heavy reliance on key customers, technology adoption risks, higher R&D spending, geopolitical exposure, and rising competition all cloud Nova's revenue and margin outlook.

Catalysts

About Nova- Engages in the design, development, production, and sells of process control systems used in the manufacture of semiconductors in Taiwan, the United States, China, Korea, and internationally.

- The accelerating complexity of semiconductor devices-driven by AI, larger die sizes, advanced nodes, and heterogeneous packaging-continues to fuel demand for Nova's advanced metrology solutions across both logic/foundry and memory segments, which is poised to lift long-term revenue growth as global digitization trends expand.

- Ongoing global investments in semiconductor manufacturing capacity (including reshoring, new fabs in multiple regions, and government incentives) are broadening Nova's customer base and diversifying revenue streams, supporting sustained top-line growth and reducing reliance on any single geography or customer.

- Expansion of Nova's software-driven analytics, AI/ML integration, and value-added services is deepening customer relationships and driving a recurring revenue mix with higher margins, which is likely to support stable or improving net margins over time.

- Introduction and ramp of new product platforms (e.g., Sentronics integration, VeraFlex, METRION, and ELIPSON tools) for advanced logic, memory, and 3D NAND applications positions Nova to capture additional market share and opens new cross-selling opportunities, further boosting future revenue trajectories.

- Operational excellence achieved through diversified revenue streams, a resilient business model, and continued efficiency investments positions Nova to leverage scale and expand operating margins as their solutions proliferate through industry inflection points.

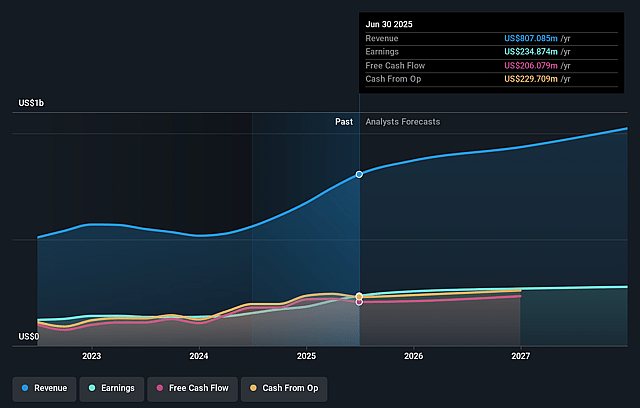

Nova Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Nova's revenue will grow by 9.8% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 29.1% today to 27.5% in 3 years time.

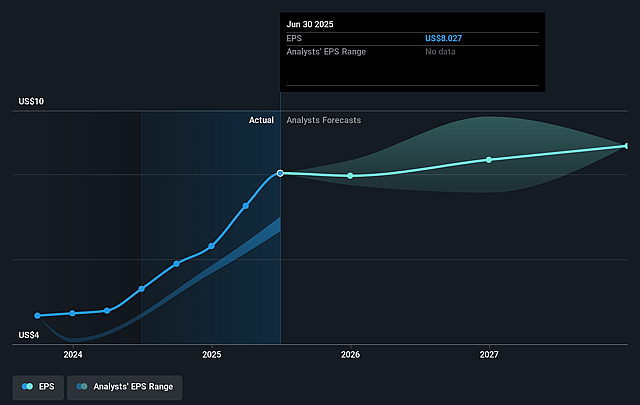

- Analysts expect earnings to reach $293.1 million (and earnings per share of $8.67) by about September 2028, up from $234.9 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 45.5x on those 2028 earnings, up from 34.7x today. This future PE is greater than the current PE for the US Semiconductor industry at 33.5x.

- Analysts expect the number of shares outstanding to grow by 1.9% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 13.01%, as per the Simply Wall St company report.

Nova Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Nova's significant exposure to a few major "gate-all-around" and advanced node customers increases concentration risk-if any large customer reduces or delays CapEx, as hinted at for one IDM customer, it could result in uneven revenue growth and threaten earnings stability over time.

- The company's ongoing growth depends on successful adoption and commercialization of new technologies like ELIPSON, METRION, and advanced material metrology platforms; failure to reach "process tool of record" status or slower-than-expected lab-to-fab conversion could stall product diversification and limit future top-line expansion.

- Heightened investments in R&D and integration of new acquisitions (e.g., Sentronics), while necessary for innovation, may pressure net margins if commercialization cycles are longer than planned or if revenue synergy assumptions are not fully realized.

- Nova cites increasing strength in advanced packaging and China, but given potential future shifts in trade restrictions, tariffs, or geopolitical tensions, its global revenue diversification remains vulnerable to external shocks that could negatively impact both revenue and margin profiles.

- The market's current optimism about Nova's competitive leadership in several segments could be undermined by intensified competition in integrated and stand-alone metrology, especially if larger or emerging players launch new products or price aggressively, potentially eroding Nova's gross margins and long-term earnings power.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $298.333 for Nova based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.1 billion, earnings will come to $293.1 million, and it would be trading on a PE ratio of 45.5x, assuming you use a discount rate of 13.0%.

- Given the current share price of $277.22, the analyst price target of $298.33 is 7.1% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.