Key Takeaways

- Lam Research's lead in critical NAND processes and new material use will drive significant growth opportunities and improved margins.

- AI-driven demands in advanced packaging and logic nodes position Lam to capture high market share, enhancing revenue and earnings.

- Geopolitical risks and export restrictions in China, alongside technology reliance and market challenges, pose threats to Lam Research's revenue and earnings growth.

Catalysts

About Lam Research- Designs, manufactures, markets, refurbishes, and services semiconductor processing equipment used in the fabrication of integrated circuits.

- Lam Research expects significant growth opportunities in 2025 due to technology transitions in NAND, which include upgrades to more advanced nodes. These transitions are expected to disproportionately benefit Lam because of their leading position in critical NAND processes, impacting revenue and potentially enhancing net margins.

- Increased investments in leading-edge logic nodes, advanced packaging, and high-bandwidth memory are driven by AI and other advanced technologies. Lam is positioned to capture high market share in these etch and deposition-intensive areas, which should support revenue growth and improve earnings.

- The company is benefiting from the introduction of new materials like molybdenum, which help address challenges such as wordline resistance in NAND. This materials migration, where Lam leads in deposition technology, is expected to be a key driver of growth in 2025, contributing positively to Lam's revenue and margins.

- Advanced packaging, driven by AI demands, has been a significant growth area, with Lam's SABRE 3D technology gaining market share. Continued complexity and performance requirements in packaging should enhance Lam's revenue and market share, expanding earnings.

- Lam's Customer Support Business Group is seeing stronger customer interest in productivity enhancements and equipment intelligence services. This focus on extending and upgrading the installed base optimizes value for customers and could lead to growth in revenue and profitability from service offerings.

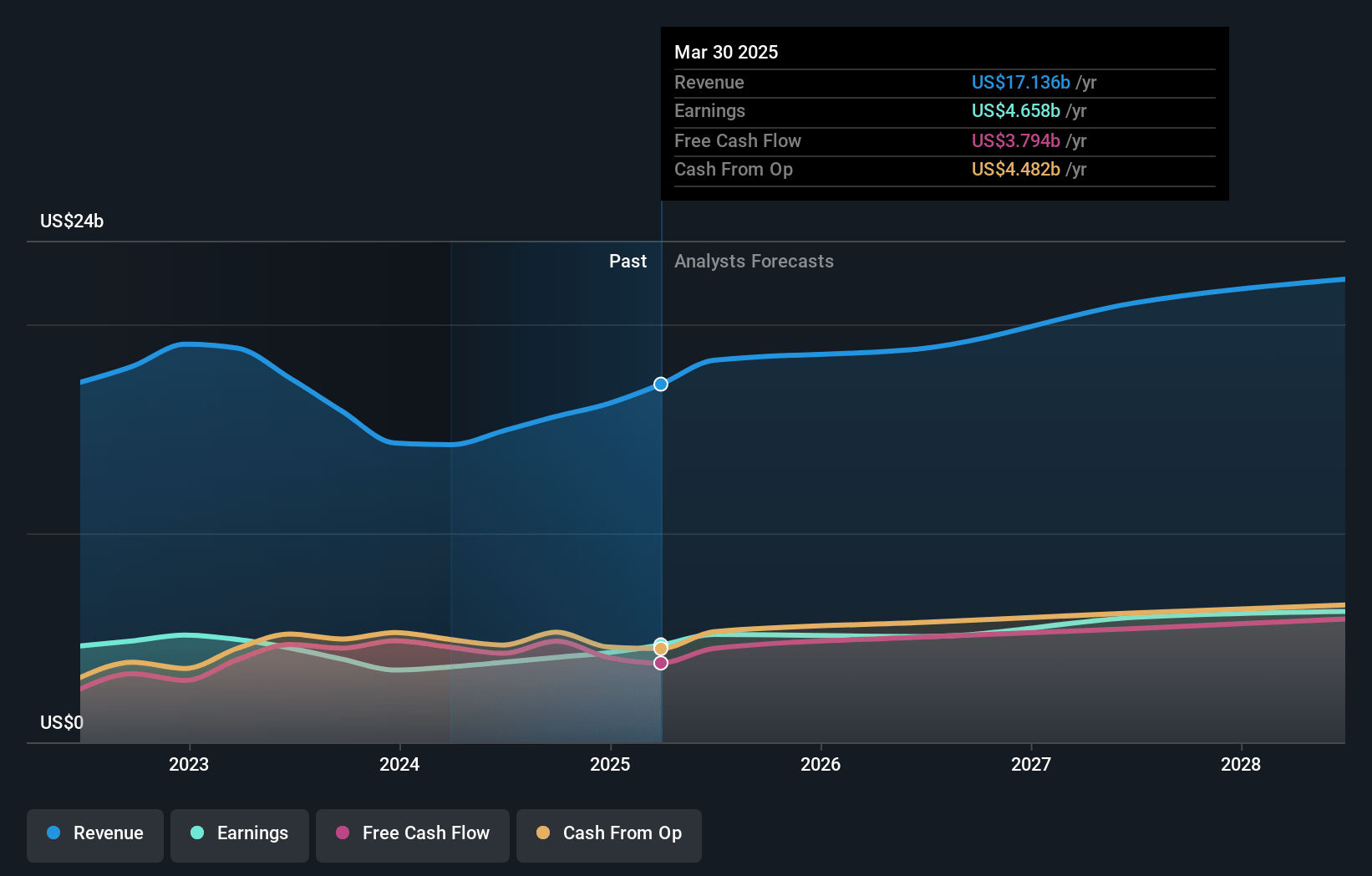

Lam Research Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Lam Research's revenue will grow by 11.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 26.0% today to 28.3% in 3 years time.

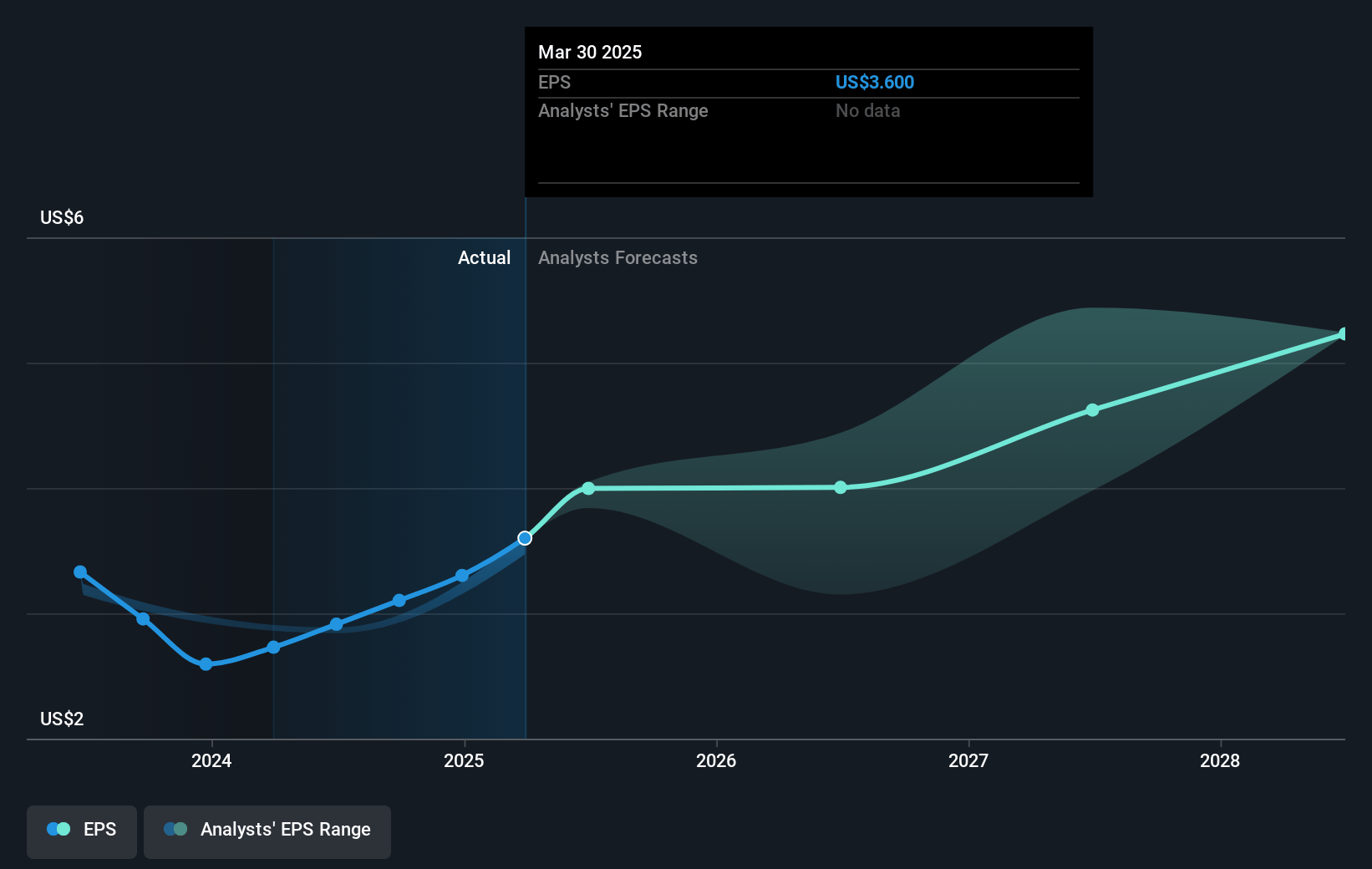

- Analysts expect earnings to reach $6.1 billion (and earnings per share of $4.89) by about January 2028, up from $4.1 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $5.4 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 23.4x on those 2028 earnings, down from 23.6x today. This future PE is lower than the current PE for the US Semiconductor industry at 31.2x.

- Analysts expect the number of shares outstanding to decline by 0.86% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.05%, as per the Simply Wall St company report.

Lam Research Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- There is a prolonged down cycle in the NAND segment, and although spending is anticipated to increase in 2025, the industry's recovery may be slower than expected, impacting Lam’s revenue.

- A significant portion of Lam's revenue comes from China, but expectations of future revenue from China are down due to geopolitical risks and export restrictions, which could affect Lam's revenue and earnings.

- Gross margin improvements hinge on operational efficiencies offsetting negative customer mix effects; failure to maintain or improve operational efficiencies could impact net margins.

- There is a reliance on advanced technologies such as gate-all-around and molybdenum adoption, which may face unforeseen technical or market acceptance challenges impacting Lam’s revenue projections.

- Spending on client-focused investments and customer support through CSBG may not scale as quickly as anticipated, potentially affecting net margins and long-term earnings growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $90.85 for Lam Research based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $110.0, and the most bearish reporting a price target of just $75.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $21.7 billion, earnings will come to $6.1 billion, and it would be trading on a PE ratio of 23.4x, assuming you use a discount rate of 8.1%.

- Given the current share price of $74.51, the analyst's price target of $90.85 is 18.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives