Key Takeaways

- Advanced SiP and 2.5D investments in AI and ARM-based PCs could drive future revenue growth in high-performance computing and AI markets.

- Strategic partnerships and global manufacturing expansion enhance operational efficiency, technology innovation, and competitive positioning, supporting revenue growth and market presence.

- Weakness in automotive and industrial sectors, factory underutilization, and Vietnam ramp-up costs pressure Amkor’s margins and earnings, challenging near-term revenue growth.

Catalysts

About Amkor Technology- Provides outsourced semiconductor packaging and test services in the United States, Japan, Europe, the Middle East, Africa, and the Asia Pacific.

- Amkor's investment in advanced SiP and 2.5D capacity for AI devices and ARM-based PCs positions the company to capitalize on the growing demand in the high-performance computing and AI processor markets, potentially driving future revenue growth.

- Strategic partnerships with industry leaders such as TSMC and Infineon strengthen Amkor's position in the semiconductor market, which could positively impact future revenues and margins through collaborative innovation and shared technology.

- The expansion of Amkor’s global manufacturing footprint, including new production facilities in Vietnam and planned facilities in Arizona, is expected to improve operational efficiency and reliability of supply chains, potentially enhancing margins and supporting revenue growth.

- Amkor’s broadening technology portfolio with investments in RF capabilities and next-generation packaging technologies may enhance its competitive edge, fostering revenue growth in areas like premium smartphones, consumer IoT devices, and automotive applications.

- Long-term growth in the automotive market, including expansion into ADAS processors and EV-related power modules, aligns with secular trends and could lead to significant revenue contributions once inventory issues stabilize and end-market demand rebounds.

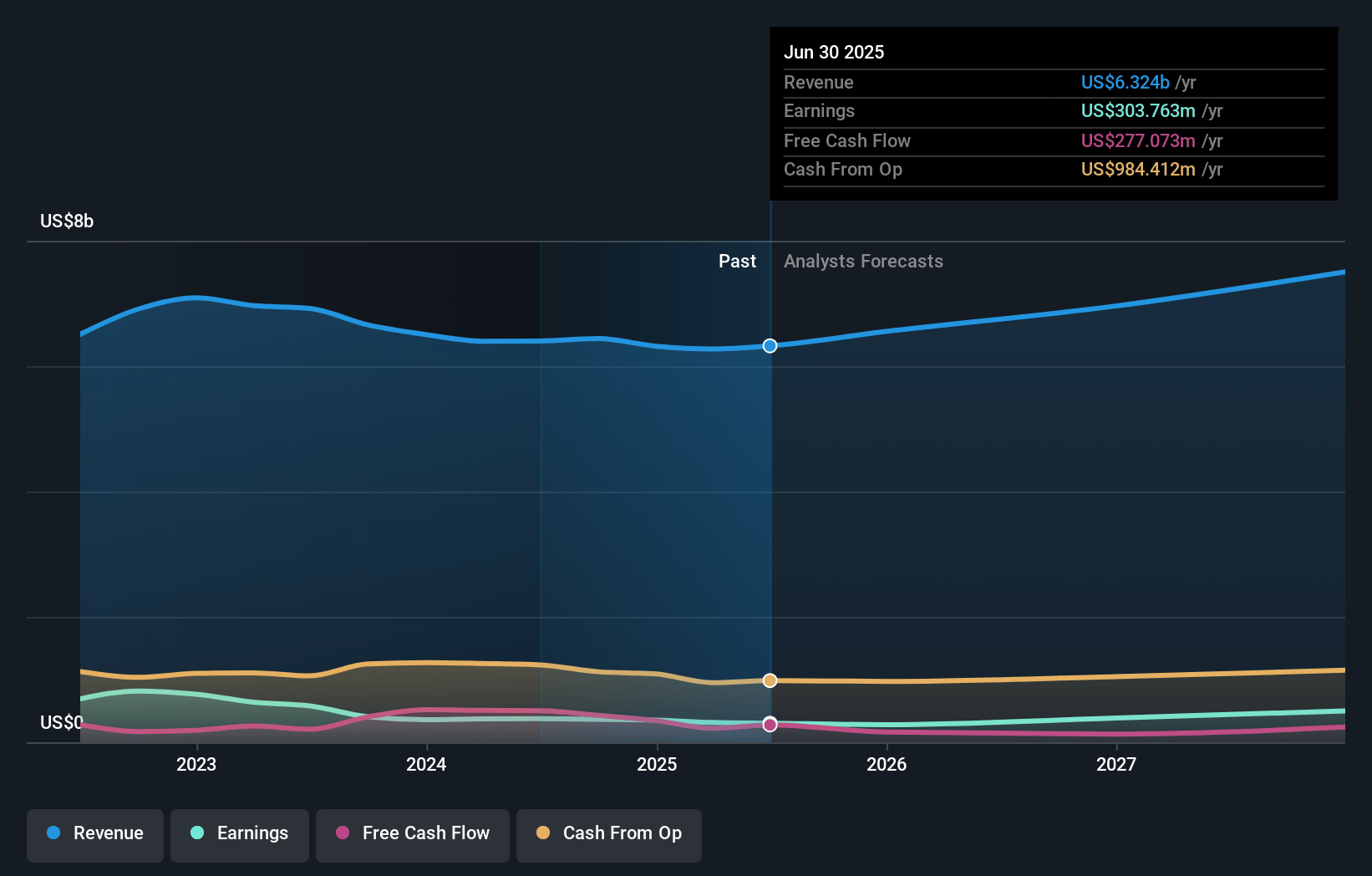

Amkor Technology Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Amkor Technology's revenue will grow by 4.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.7% today to 10.2% in 3 years time.

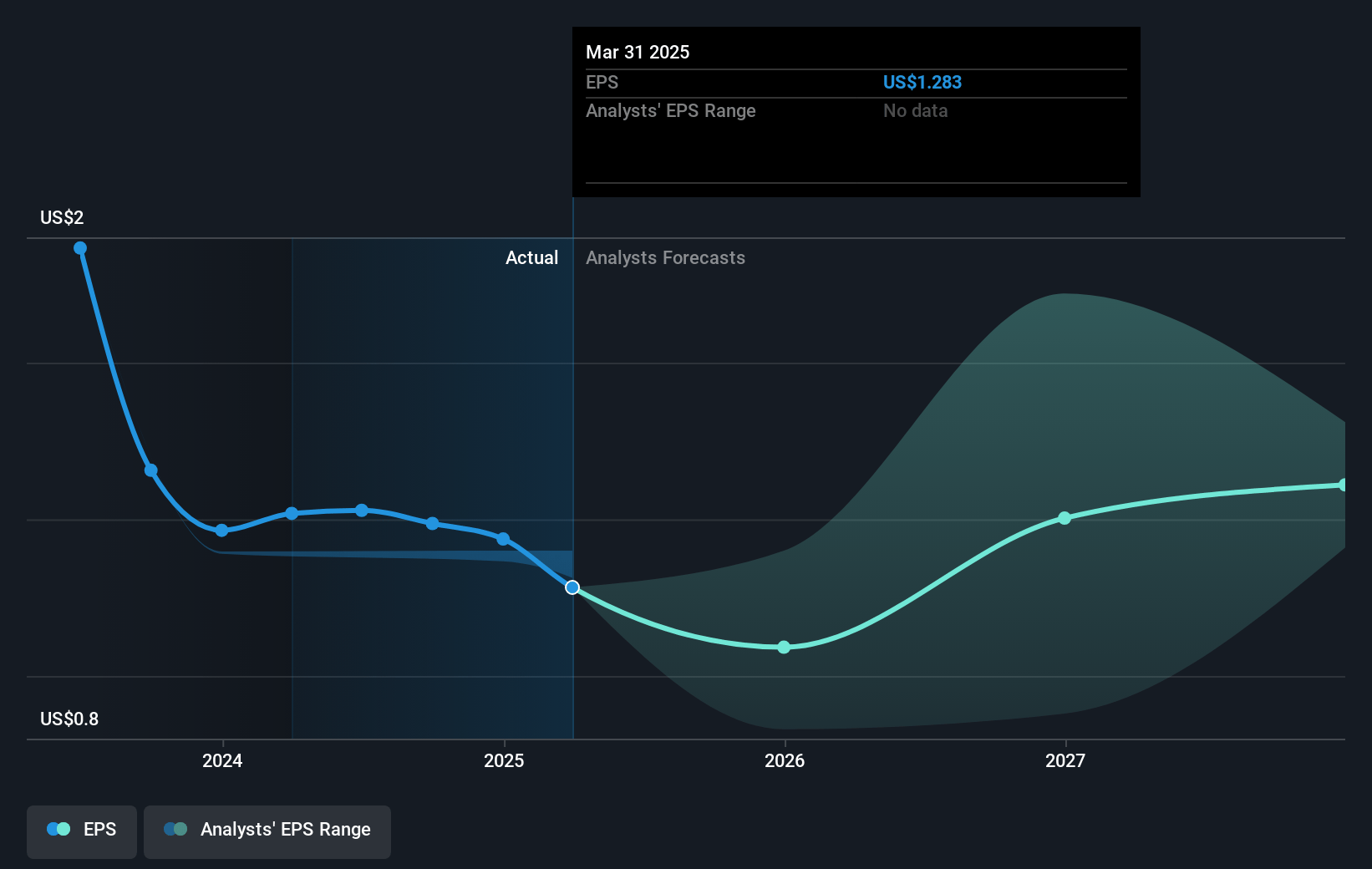

- Analysts expect earnings to reach $751.9 million (and earnings per share of $2.53) by about January 2028, up from $365.9 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $380.1 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 17.2x on those 2028 earnings, up from 16.2x today. This future PE is lower than the current PE for the US Semiconductor industry at 31.2x.

- Analysts expect the number of shares outstanding to grow by 6.48% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.58%, as per the Simply Wall St company report.

Amkor Technology Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Amkor is experiencing a prolonged weakness in the automotive and industrial sectors, resulting in a year-to-date revenue decline of 24% for its mainstream business. This could negatively impact future revenue growth if these sectors do not recover as anticipated.

- The company's gross margin is constrained by higher than seasonal material content and underutilization in its mainstream factories, particularly in automotive lines, which could affect net margins if this continues.

- There's uncertainty in the premium tier smartphone build plan, deviating from historical trends, which is expected to lead to a more than seasonal revenue decline in the fourth quarter of 2024, impacting earnings.

- The underutilization of Amkor’s factories in the Philippines, Japan, and Korea due to weak demand in the automotive sector is affecting cost efficiency and could pressure profit margins.

- Amkor’s Vietnam facility ramp-up is expected to exert a dilution effect on gross margins due to the burden of transitioning costs to COGS, which could lead to lower net earnings in the short-term until scale is achieved.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $33.93 for Amkor Technology based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $42.0, and the most bearish reporting a price target of just $26.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $7.4 billion, earnings will come to $751.9 million, and it would be trading on a PE ratio of 17.2x, assuming you use a discount rate of 8.6%.

- Given the current share price of $24.07, the analyst's price target of $33.93 is 29.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives