Narratives are currently in beta

Key Takeaways

- Axcelis is leveraging growth in the silicon carbide market and transitioning wafer capacity to boost revenue and net margins.

- Strategic focus on advanced logic applications and memory market recovery could enhance revenue, with a deeper Japanese market presence driving diversification.

- Heavy reliance on the Chinese market and backlog issues could affect Axcelis's future revenues amid soft demand and geopolitical risks.

Catalysts

About Axcelis Technologies- Designs, manufactures, and services ion implantation and other processing equipment used in the fabrication of semiconductor chips in the United States, Japan, Europe, and Asia Pacific.

- Axcelis is well-positioned in the silicon carbide market, which is expected to grow significantly, potentially boosting future revenue growth due to the critical role of ion implantation in silicon carbide device manufacturing.

- The company is capitalizing on the transition from 150 mm to 200 mm wafer capacity and trench architecture in silicon carbide applications, likely enhancing revenue and net margins due to increased demand for their high-energy tools.

- Axcelis is focused on new application opportunities in advanced logic and exploring share gains, which may positively impact future revenues as they develop new technologies tailored to customer needs.

- The anticipated cyclical recovery in memory market demand, particularly DRAM, could drive substantial revenue growth as Axcelis actively positions itself for an increased demand with prebuilt inventory ready for quick response.

- Axcelis plans to penetrate the Japanese market more deeply, leveraging its existing success in power, which could enhance revenue diversification and create opportunities for earnings growth through expanded market share.

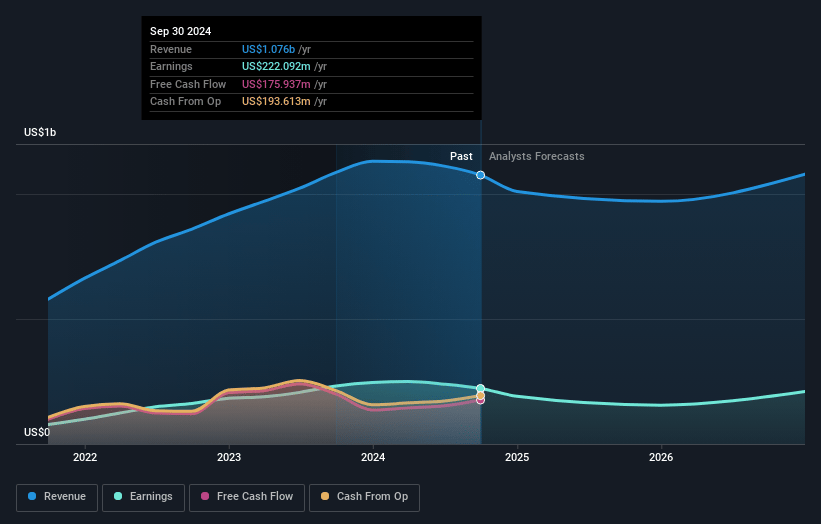

Axcelis Technologies Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Axcelis Technologies's revenue will decrease by -1.4% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 20.6% today to 16.4% in 3 years time.

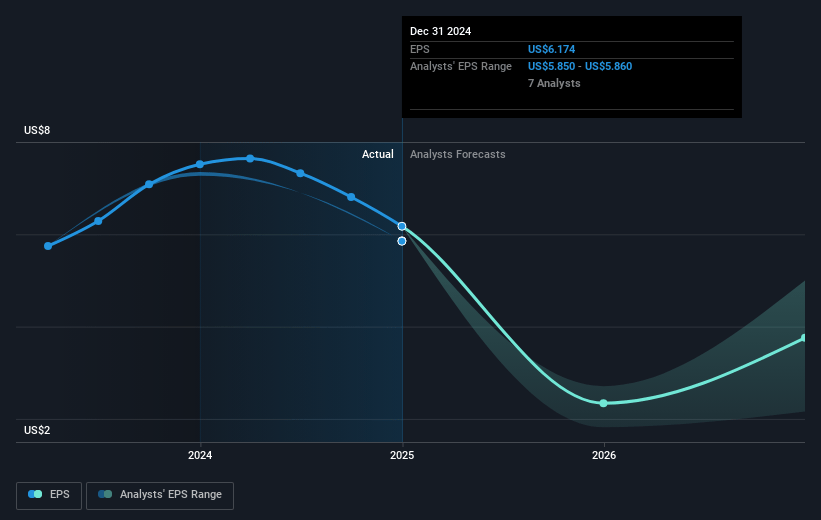

- Analysts expect earnings to reach $169.2 million (and earnings per share of $5.62) by about December 2027, down from $222.1 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 24.9x on those 2027 earnings, up from 10.6x today. This future PE is lower than the current PE for the US Semiconductor industry at 30.0x.

- Analysts expect the number of shares outstanding to decline by 2.53% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.03%, as per the Simply Wall St company report.

Axcelis Technologies Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Bookings were softer than expected due to customers digesting past investments, leading to potential short-term revenue declines. This could negatively impact earnings if trends continue.

- Axcelis is seeing signs of potential revenue reduction in general mature and power markets, particularly in China, which could negatively affect earnings if demand does not recover.

- A backlog error was identified that may raise concerns about financial controls and forecast accuracy, potentially impacting investor confidence and future revenues.

- Revenue predominantly coming from China (71%) increases exposure to geopolitical risks and reliance on a single region, which could affect future revenues if the market realigns or regulations change.

- Softening expectations for future orders and market growth, particularly in power and mature nodes, suggest that the financial outlook could face headwinds, impacting future earnings estimates.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $111.5 for Axcelis Technologies based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $125.0, and the most bearish reporting a price target of just $86.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $1.0 billion, earnings will come to $169.2 million, and it would be trading on a PE ratio of 24.9x, assuming you use a discount rate of 8.0%.

- Given the current share price of $72.1, the analyst's price target of $111.5 is 35.3% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives