Key Takeaways

- Expanding Princess Polly stores and adopting a test and repeat model at Culture Kings are expected to drive revenue growth and enhance earnings.

- Strategic partnerships and AI investments aim to broaden market reach, improve cost efficiency, and contribute to top-line and net margin growth.

- Regional sales declines, tariff reliance, and increased expenses pose risks to a.k.a. Brands Holding's revenue growth, profitability, and financial stability.

Catalysts

About a.k.a. Brands Holding- Operates a portfolio of online fashion brands in the United States, Australia, New Zealand, and internationally.

- The expansion of Princess Polly stores in key locations is expected to enhance brand awareness, attract new customers, and generate incremental lift in online sales within store areas, positively impacting revenue growth.

- The transition to a test and repeat merchandising model at Culture Kings is anticipated to improve sales performance, increase gross margins by reducing inventory risk, and boost revenue through the introduction of fresh fashion, driving earnings growth.

- The company's focus on strategic partnerships with major retailers like Nordstrom and global marketplaces like asos.com is expected to broaden market reach and increase wholesale revenue, contributing to overall top-line growth.

- Investments in AI-driven solutions to optimize marketing, inventory planning, and customer experience are likely to streamline operations, improve cost efficiency, and enhance net margins.

- Continued share repurchase initiatives indicate management's confidence in the stock's undervaluation and can contribute to EPS growth as the company reduces the overall share count.

a.k.a. Brands Holding Future Earnings and Revenue Growth

Assumptions

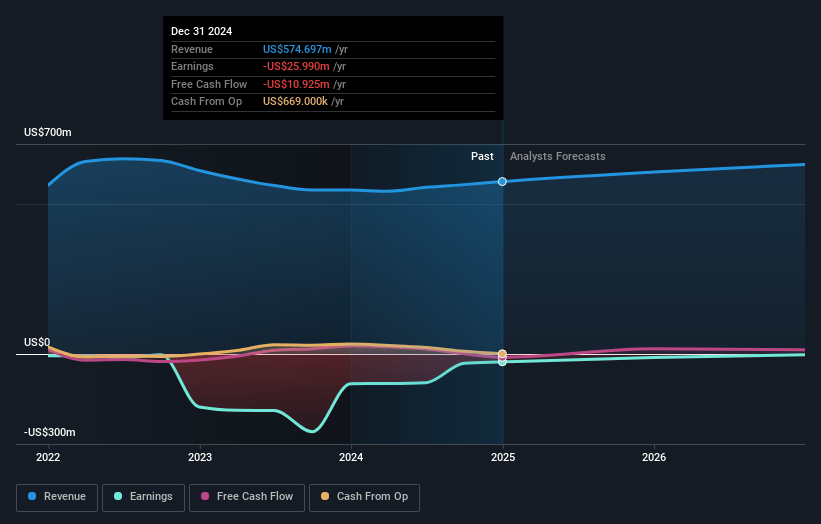

How have these above catalysts been quantified?- Analysts are assuming a.k.a. Brands Holding's revenue will grow by 4.8% annually over the next 3 years.

- Analysts are not forecasting that a.k.a. Brands Holding will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate a.k.a. Brands Holding's profit margin will increase from -4.5% to the average US Specialty Retail industry of 4.4% in 3 years.

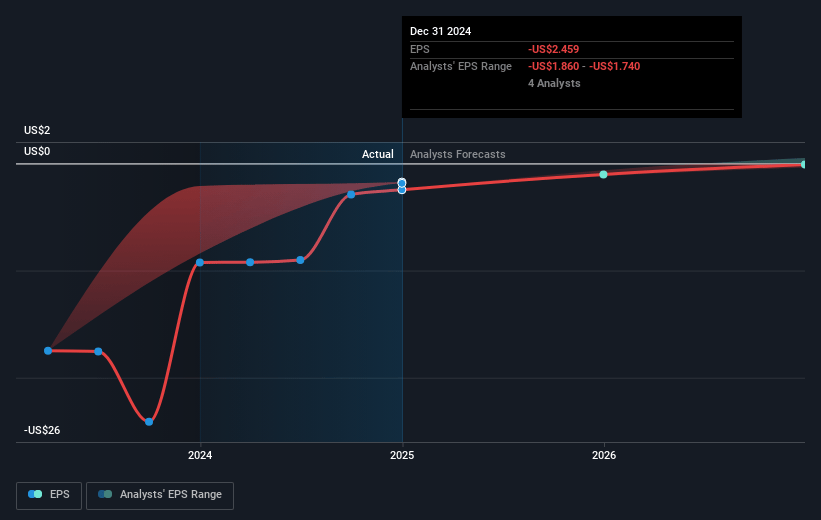

- If a.k.a. Brands Holding's profit margin were to converge on the industry average, you could expect earnings to reach $29.1 million (and earnings per share of $2.65) by about May 2028, up from $-26.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 12.4x on those 2028 earnings, up from -3.2x today. This future PE is lower than the current PE for the US Specialty Retail industry at 15.2x.

- Analysts expect the number of shares outstanding to grow by 1.99% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 11.41%, as per the Simply Wall St company report.

a.k.a. Brands Holding Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The decline in net sales in Australia and New Zealand by 9.6% and in the Rest of World region by 13.5% suggests regional vulnerabilities that could impact future revenue growth if these markets do not stabilize or rebound as expected.

- Tariffs and reliance on sourcing predominantly from China introduce cost pressures and the ability to maintain profit margins, as evidenced by the need to mitigate tariff impacts and seek alternate sourcing strategies.

- Store expansion, while providing growth opportunities, involves significant capital expenditures ($12 million to $14 million in 2025) that could strain financial resources, especially if the new stores do not perform as expected, impacting net margins and profitability.

- The increase in general and administrative expenses due to incentive compensation and non-routine legal matters may continue, potentially constraining net margins if not managed effectively in the long term.

- Despite guidance for 2025, fluctuations in currency exchange rates present risks of FX headwinds, particularly impacting net sales growth and earnings forecasts, given the international presence of the company.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $23.75 for a.k.a. Brands Holding based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $30.0, and the most bearish reporting a price target of just $17.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $662.1 million, earnings will come to $29.1 million, and it would be trading on a PE ratio of 12.4x, assuming you use a discount rate of 11.4%.

- Given the current share price of $7.88, the analyst price target of $23.75 is 66.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.