Key Takeaways

- Exiting the office sector creates a new AFFO baseline, enhancing W. P. Carey's earnings stability and growth potential.

- Strategic asset sales and leveraging euro-denominated debt support earnings growth and shareholder value without issuing new equity.

- Economic uncertainties, tenant credit concerns, and increased competition could impact W. P. Carey's revenue growth, margins, and investment returns.

Catalysts

About W. P. Carey- W. P. Carey ranks among the largest net lease REITs with a well-diversified portfolio of high-quality, operationally critical commercial real estate, which includes 1,430 net lease properties covering approximately 172 million square feet and a portfolio of 78 self-storage operating properties as of September 30, 2024.

- W. P. Carey's recent strategic exit from the office sector is expected to create a new baseline for AFFO, setting a foundation for future growth and potentially enhancing earnings stability.

- The strong investment volume in the fourth quarter of 2024, with anticipated future benefits accruing in 2025, suggests revenue growth as the returns from these investments, which averaged yields above 9%, start to materialize in the company's financials.

- The company's ability to fund new investments without issuing equity, leveraging its competitively priced debt, particularly in the euro-denominated debt market, positions it to grow earnings while preserving shareholder value.

- Potential asset sales of noncore properties, priced favorably relative to reinvestment opportunities, are expected to fund accretive net lease investments, maximizing earnings and improving net margins.

- Prospects for larger-scale M&A activities and potential onshoring or nearshoring trends present additional opportunities for growth in investment activity and portfolio expansion, potentially increasing future revenue streams.

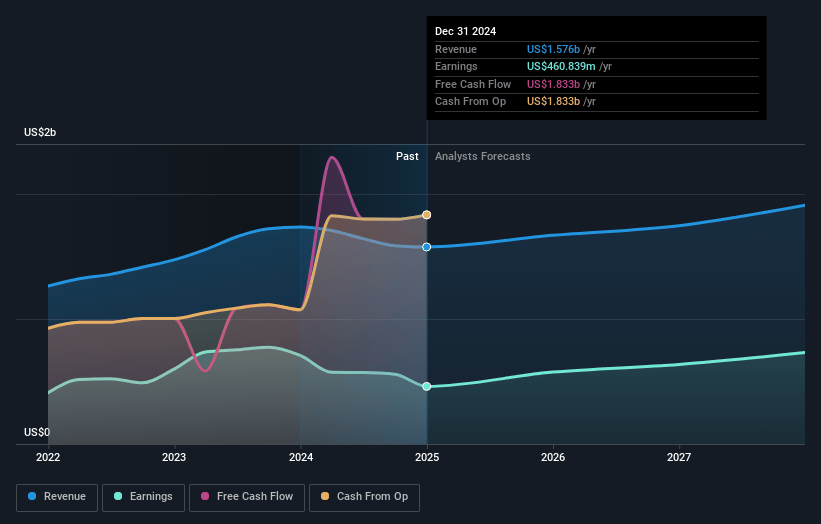

W. P. Carey Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming W. P. Carey's revenue will grow by 6.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 29.2% today to 38.3% in 3 years time.

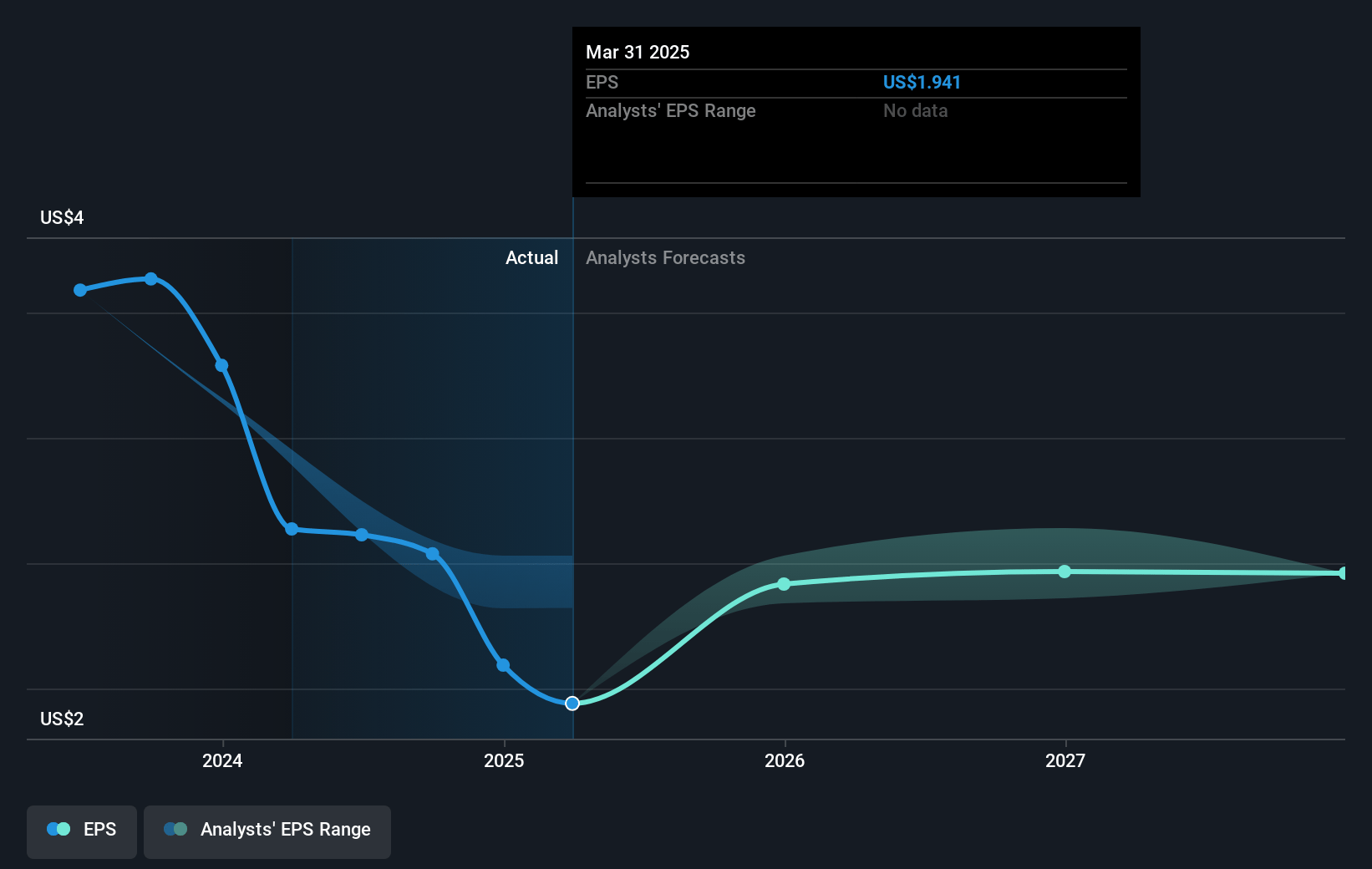

- Analysts expect earnings to reach $731.6 million (and earnings per share of $2.66) by about April 2028, up from $460.8 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $814.2 million in earnings, and the most bearish expecting $649 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 23.2x on those 2028 earnings, down from 29.1x today. This future PE is lower than the current PE for the US REITs industry at 25.1x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.91%, as per the Simply Wall St company report.

W. P. Carey Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Economic uncertainties such as inflation, interest rates, and potential impacts from new tariffs or administrations could negatively influence investment strategies and cost of capital, impacting revenue growth projections.

- The potential widening of bid-ask spreads from spiking 10-year treasury rates could slow deal activity, potentially affecting future earnings and investment volume.

- Ongoing tenant credit concerns with significant tenants like Hellweg and Hearthside, coupled with possible rent disruptions, are factored into a cautious outlook, potentially impacting net margins due to credit loss reserves.

- Exposure to foreign markets, while aiming for more significant spreads in Europe, introduces currency and geopolitical risks that may impact revenue predictability and financial outcomes.

- Increased competition from private equity and market environment shifts could pressure acquisition yields and margins, impacting overall investment returns and revenue growth expectations.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $63.364 for W. P. Carey based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.9 billion, earnings will come to $731.6 million, and it would be trading on a PE ratio of 23.2x, assuming you use a discount rate of 6.9%.

- Given the current share price of $61.28, the analyst price target of $63.36 is 3.3% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.