Key Takeaways

- VICI Properties' strategic investments in Las Vegas and partner properties indicate potential for significant revenue growth and enhanced net operating income.

- A disciplined approach to capital allocation and market independence positions VICI for stable earnings and dividend growth in market volatility.

- Volatility in interest rates, niche investment focus, and regional market challenges could impact VICI's growth, revenues, and earnings.

Catalysts

About VICI Properties- An S&P 500 experiential real estate investment trust that owns one of the largest portfolios of market-leading gaming, hospitality and entertainment destinations, including Caesars Palace Las Vegas, MGM Grand and the Venetian Resort Las Vegas, three of the most iconic entertainment facilities on the Las Vegas Strip.

- VICI Properties' philosophy of capital markets independence, with projected internal cash resources of up to $1 billion, suggests the company is well-positioned for accretive external growth regardless of external capital market conditions, likely impacting earnings positively.

- The ongoing investment in Las Vegas, like the Venetian partner property growth fund, indicates potential for future expansion and development, which could lead to increased revenue streams.

- The strategic focus on casino gaming, especially around the burgeoning Las Vegas market and its entertainment assets, suggests anticipated revenue growth opportunities as the area continues to evolve.

- VICI's continued use of Partner Property Growth Fund investments with operators like Century Casinos to develop projects, such as transitioning riverboat casinos to land-based facilities, hints at a strategy that may maximize future net operating income (NOI) growth.

- A disciplined capital allocation strategy, maintaining growth even in a volatile market, suggests that compounded earnings and dividend growth may benefit from prudent investment decisions across cycles, impacting net margins positively over time.

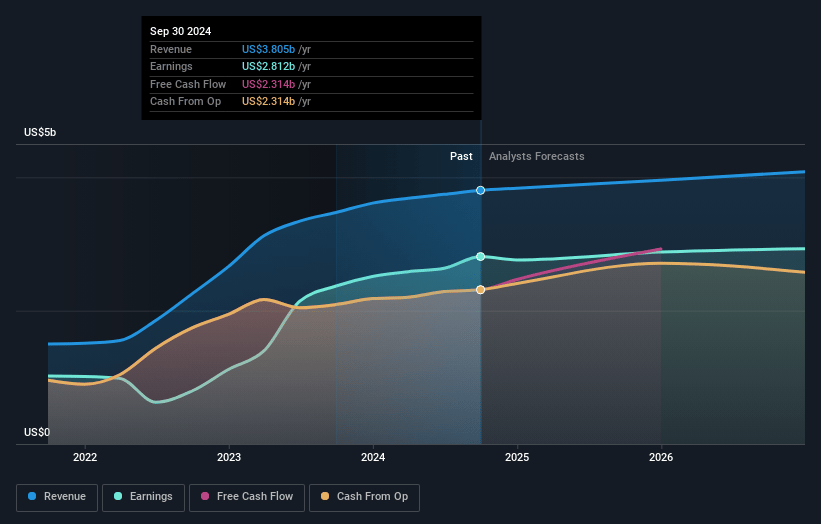

VICI Properties Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming VICI Properties's revenue will grow by 5.4% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 73.9% today to 65.2% in 3 years time.

- Analysts expect earnings to reach $2.9 billion (and earnings per share of $2.86) by about January 2028, up from $2.8 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 15.1x on those 2028 earnings, up from 11.3x today. This future PE is lower than the current PE for the US Specialized REITs industry at 25.3x.

- Analysts expect the number of shares outstanding to decline by 1.27% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.64%, as per the Simply Wall St company report.

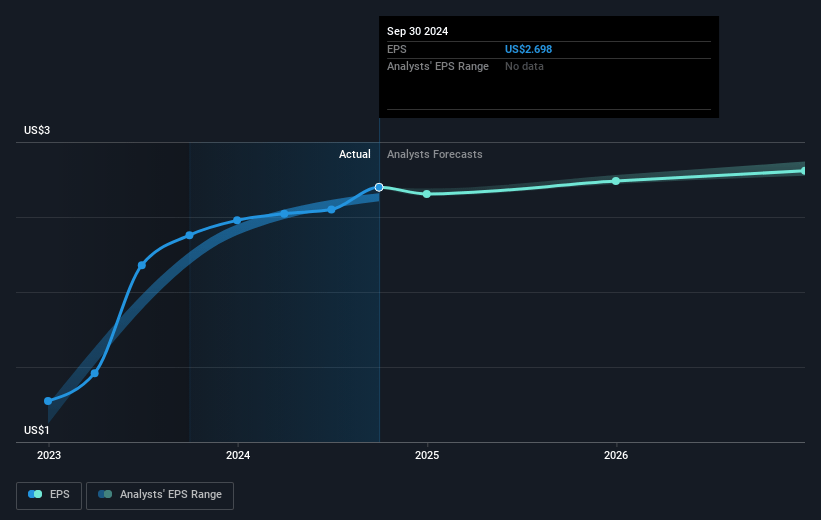

VICI Properties Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The significant volatility in interest rates, as illustrated by the substantial rise in the 10-year yield, could impact VICI's ability to fund investments cost-effectively, potentially affecting net margins and earnings.

- The REIT's focus on niche experiential investments and smaller, less frequent transactions could limit its capacity for larger-scale growth opportunities, impacting long-term revenue expansion.

- Regional gaming markets might face challenges due to the potential oversupply of casinos, leading to cannibalization and lower profits, which could affect VICI's revenue if they are invested in such markets.

- VICI's investment focus on Las Vegas presents risks if there are fluctuating economic conditions or consumer spending patterns, potentially impacting rental revenues.

- Challenges in expanding into tribal gaming on tribal land due to unique legislative and structural issues add additional risk and complexity, which could impact future earnings and capital allocation decisions.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $35.55 for VICI Properties based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $43.0, and the most bearish reporting a price target of just $32.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $4.5 billion, earnings will come to $2.9 billion, and it would be trading on a PE ratio of 15.1x, assuming you use a discount rate of 6.6%.

- Given the current share price of $30.01, the analyst's price target of $35.55 is 15.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives