Narratives are currently in beta

Key Takeaways

- Strong leasing activity and strategic capital recycling initiatives are boosting revenue growth and improving net margins.

- Potential risks from compressed cap rate acquisitions and shareholder dilution could impact future earnings growth and projections.

- Robust growth in net operating income and strategic acquisitions boost revenue, occupancy rates, and net margins, supporting strong earnings and future growth.

Catalysts

About Urban Edge Properties- A NYSE listed real estate investment trust focused on owning, managing, acquiring, developing, and redeveloping retail real estate in urban communities, primarily in the Washington, D.C.

- The company is actively engaging in capital recycling by acquiring high-quality shopping centers at attractive cap rates and funding these acquisitions through the sale of non-core and single-tenant assets. This could temporarily inflate revenue projections and impact net margins positively due to expected asset appreciation and efficient capital allocation.

- New leasing activity is strong, with a significant increase in shop occupancy and favorable lease spreads, which will boost future revenue growth, but competitive leasing markets may tighten margins over time.

- Their focus on low-risk redevelopment projects with an anticipated strong unlevered yield could inflate earnings projections. However, these projects carry inherent execution risks that could impact net margins if not completed on time and within budget.

- The company is pursuing acquisitions in core markets at compressed cap rates, which could imply overestimation of earnings growth if market conditions change or if acquisitions do not yield the expected financial performance.

- Issuing new shares to raise capital for acquisitions could lead to shareholder dilution, potentially impacting earnings per share projections negatively if the expected acquisition returns do not materialize.

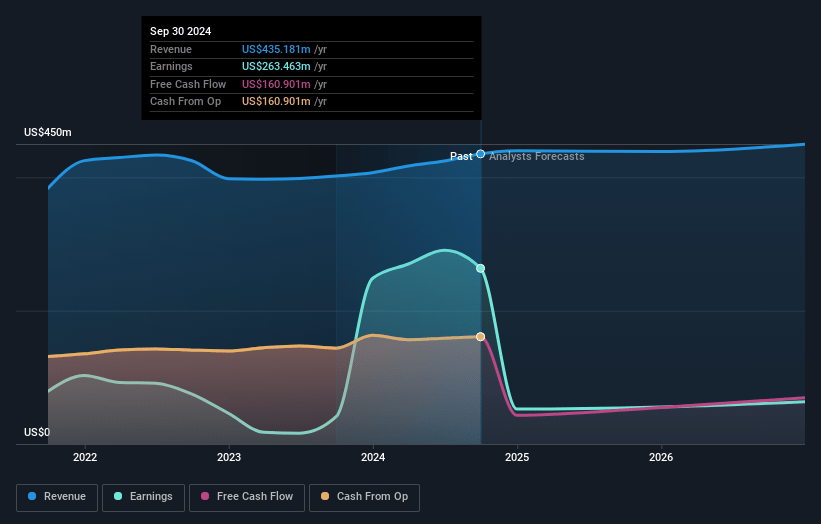

Urban Edge Properties Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Urban Edge Properties's revenue will grow by 1.3% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 60.5% today to 5.9% in 3 years time.

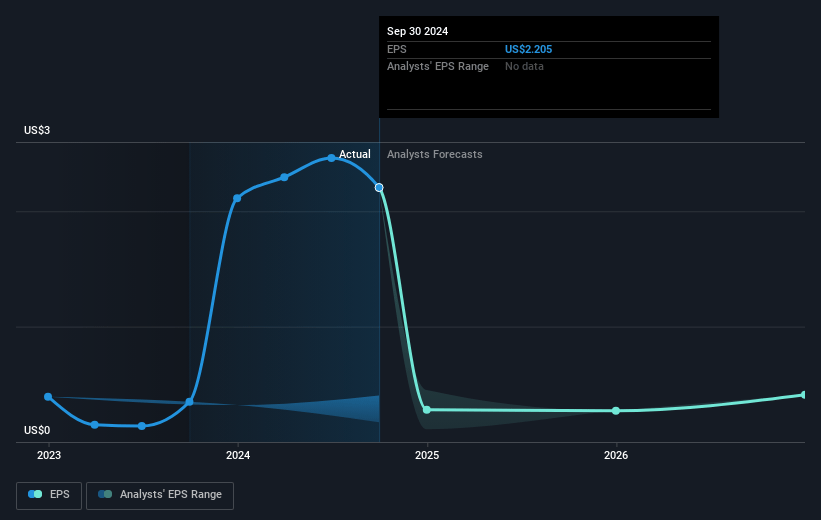

- Analysts expect earnings to reach $26.7 million (and earnings per share of $0.1) by about January 2028, down from $263.5 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 291.3x on those 2028 earnings, up from 10.2x today. This future PE is greater than the current PE for the US Retail REITs industry at 34.2x.

- Analysts expect the number of shares outstanding to grow by 26.6% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.78%, as per the Simply Wall St company report.

Urban Edge Properties Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Urban Edge Properties has seen robust FFO growth, driven by a 5.1% increase in same-property net operating income, indicating strong underlying performance which could positively impact earnings and net margins.

- The acquisition strategy focuses on high-quality shopping centers with strong anchors and shop users, contributing to a substantial expected first year leverage return and indicating potential revenue growth.

- Leasing activity remains high, with a significant increase in occupancy rates and strong retail fundamentals, suggesting continued improvement in net margins through higher occupancy and rental income.

- Strong acquisition and disposition strategy has allowed for capital recycling that results in accretion, supporting stable growth in earnings through advantageous asset swaps.

- The company has a low-risk redevelopment program contributing a strong unlevered yield on cost, providing additional avenues for improving net margins and driving future earnings growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $23.25 for Urban Edge Properties based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $26.0, and the most bearish reporting a price target of just $20.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $452.1 million, earnings will come to $26.7 million, and it would be trading on a PE ratio of 291.3x, assuming you use a discount rate of 7.8%.

- Given the current share price of $21.5, the analyst's price target of $23.25 is 7.5% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives