Narratives are currently in beta

Key Takeaways

- Redevelopment and technology initiatives are set to enhance operational efficiency, boosting net margins and earnings.

- Strategic focus on high-growth markets and lower-priced housing may maintain strong occupancy and support stable revenue growth.

- Elevated supply and competition in key markets, alongside rising operating expenses, could pressure rental revenue growth and compress net margins.

Catalysts

About Mid-America Apartment Communities- MAA, an S&P 500 company, is a real estate investment trust (REIT) focused on delivering full-cycle and superior investment performance for shareholders through the ownership, management, acquisition, development and redevelopment of quality apartment communities primarily in the Southeast, Southwest and Mid-Atlantic regions of the United States.

- MAA expects the peak of new supply deliveries impacting their markets has passed, leading to improved leasing conditions by spring 2025. This should positively affect revenue and occupancy rates.

- The company is undertaking significant redevelopment plans and technology initiatives to gain operational efficiencies, which should boost net margins and earnings.

- MAA's in-house development projects, joint ventures, and new acquisitions provide a strong pipeline for external growth, potentially enhancing revenue and net asset value.

- With new construction costs declining in some areas, MAA expects to start additional projects at favorable yields in 2025, potentially impacting future net operating income and earnings positively.

- MAA is strategically focused on high-growth markets, offering lower-priced housing alternatives, which could help maintain low resident turnover and strong occupancy rates, thus supporting stable revenue growth.

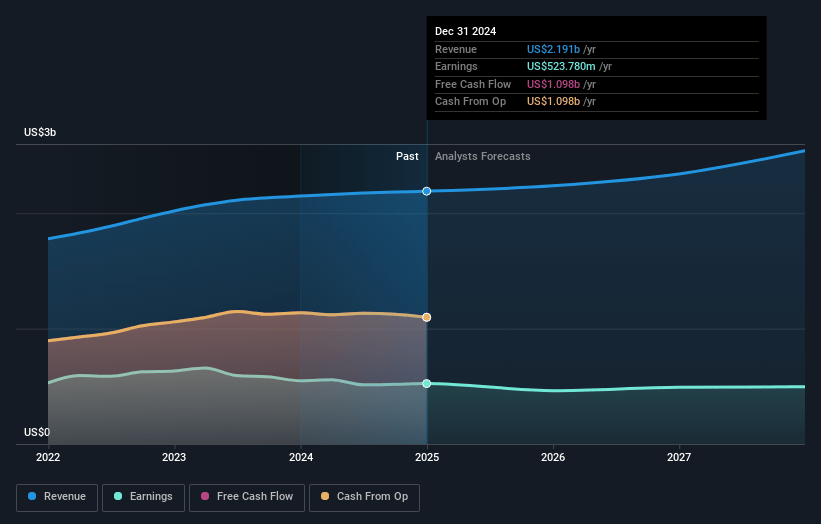

Mid-America Apartment Communities Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Mid-America Apartment Communities's revenue will grow by 4.3% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 23.7% today to 19.5% in 3 years time.

- Analysts expect earnings to reach $483.2 million (and earnings per share of $4.54) by about January 2028, down from $517.5 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $584.6 million in earnings, and the most bearish expecting $416.9 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 43.2x on those 2028 earnings, up from 34.2x today. This future PE is greater than the current PE for the US Residential REITs industry at 34.8x.

- Analysts expect the number of shares outstanding to decline by 3.94% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.44%, as per the Simply Wall St company report.

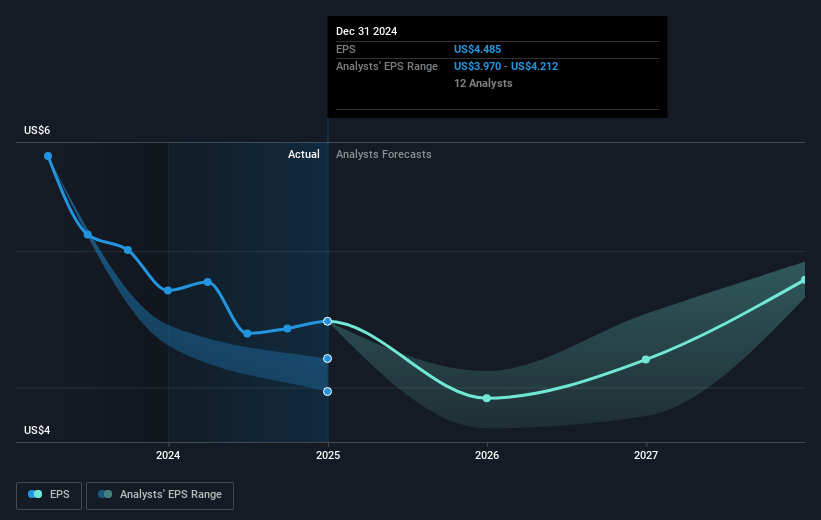

Mid-America Apartment Communities Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Elevated new supply deliveries, particularly in markets like Austin and Atlanta, are impacting new lease pricing growth negatively. This pressure might hinder potential future revenue growth.

- Economic conditions such as rising property operating expenses, including potential insurance and real estate tax increases, could compress net margins if not managed effectively.

- Competition and the concessionary environment in high-supply markets, offering up to three months of rent-free could affect MAA's ability to maintain or grow its rental revenues.

- The strategic emphasis on development projects and acquisitions requires significant capital. Rising construction costs or financing challenges could impact earnings projections if such investments don't yield anticipated returns.

- Potential overestimation of rent growth assumptions given the continuing supply pressures and uncertain macroeconomic conditions could lead to earnings falling short of projections.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $163.27 for Mid-America Apartment Communities based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $187.0, and the most bearish reporting a price target of just $148.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $2.5 billion, earnings will come to $483.2 million, and it would be trading on a PE ratio of 43.2x, assuming you use a discount rate of 6.4%.

- Given the current share price of $151.41, the analyst's price target of $163.27 is 7.3% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives