Narratives are currently in beta

Key Takeaways

- Strategic expansions and partnerships focus on scalability and sustainability, potentially enhancing future revenue and margins through key market growth.

- Strong future revenue and earnings growth are anticipated from substantial leasing volumes, increased pricing, and a significant development pipeline.

- Heavy dependence on hyperscale deals and AI demand sectors, coupled with development risks and infrastructure costs, could jeopardize growth and net margins.

Catalysts

About Digital Realty Trust- Digital Realty brings companies and data together by delivering the full spectrum of data center, colocation, and interconnection solutions.

- Digital Realty's record new leasing volume of $521 million in Q3 2024, including large-scale hyperscale deals, indicates strong future revenue growth as these leases commence.

- The company achieved record pricing on new leases and significant cash renewal spread increases, suggesting potential improvements in future net margins as new pricing structures take effect.

- A substantial development pipeline, which increased by nearly 50% to 644 megawatts under construction and is 74% pre-leased, positions Digital Realty for future earnings growth through increased capacity and utilization.

- The investment in PlatformDIGITAL and the recorded increase in Americas to EMEA exports highlight growth in international markets, expected to drive future revenue growth through global market expansion.

- Continued strategic expansion in key markets and partnerships for sustainable energy solutions suggest an operational focus on scalability and long-term sustainable growth, which could enhance both revenue and margins.

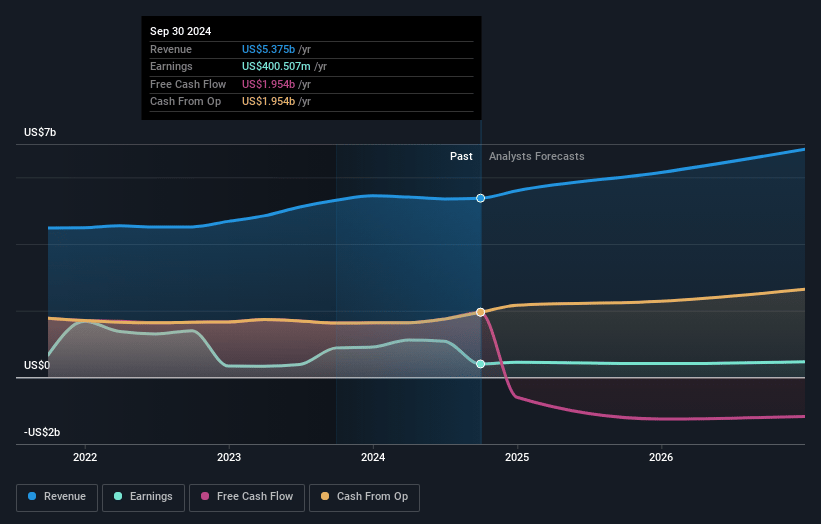

Digital Realty Trust Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Digital Realty Trust's revenue will grow by 12.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.5% today to 9.9% in 3 years time.

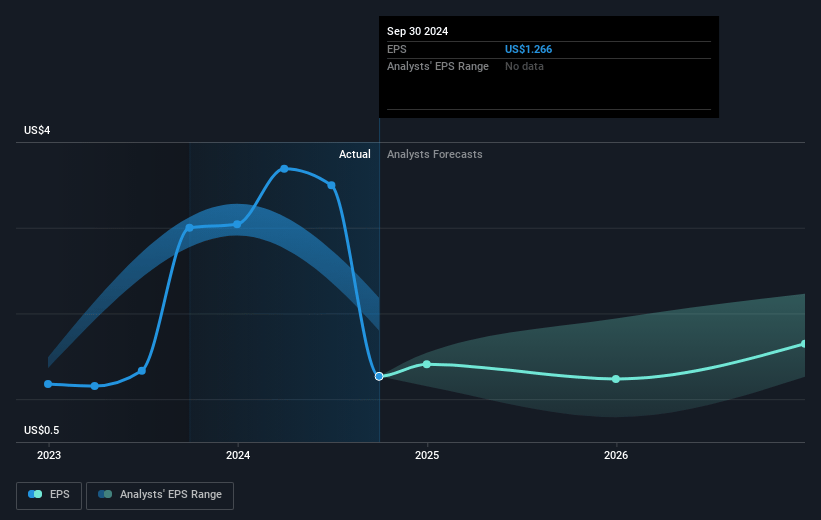

- Analysts expect earnings to reach $750.0 million (and earnings per share of $2.36) by about December 2027, up from $400.5 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 91.7x on those 2027 earnings, down from 149.4x today. This future PE is greater than the current PE for the US Specialized REITs industry at 24.8x.

- Analysts expect the number of shares outstanding to decline by 2.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.14%, as per the Simply Wall St company report.

Digital Realty Trust Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Digital Realty Trust's reliance on large hyperscale deals and substantial AI use cases could make it vulnerable to any slowdown in those demand sectors, affecting its future revenues and top-line growth.

- The company's significant increase in development under construction, with 644 megawatts underway, raises concerns about potential oversupply risks and the ability to maintain expected yields, which could impact net margins.

- Competition for power resources, such as in Northern Virginia, highlights risks of delivery delays or increased costs for power infrastructure, potentially impacting project timelines and financial performance.

- Adjustments in pricing or capacity costs, particularly with high inflationary trends in building costs, may pressure net margins if rental rates do not sufficiently offset these increased expenses.

- The reliance on maintaining a robust pipeline of interconnected systems and global enterprise expansions involves execution challenges and potential risks in market share retention, impacting earnings consistency.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $180.96 for Digital Realty Trust based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $212.0, and the most bearish reporting a price target of just $114.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $7.6 billion, earnings will come to $750.0 million, and it would be trading on a PE ratio of 91.7x, assuming you use a discount rate of 6.1%.

- Given the current share price of $180.4, the analyst's price target of $180.96 is 0.3% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives