Narratives are currently in beta

Key Takeaways

- Expiring leases and corporate move-outs might reduce occupancy and immediate cash flow, increasing pressure on leasing incentives and compressing margins.

- Required investments in redevelopment projects may strain capital, delaying earnings contributions and potentially impacting net margins negatively.

- Strategic focus on Sun Belt markets, leveraging leasing demand, and low leverage for growth in revenue, occupancy, and long-term earnings.

Catalysts

About Cousins Properties- Cousins Properties Incorporated ("Cousins") is a fully integrated, self-administered, and self-managed real estate investment trust (REIT).

- With the expected expiration of Bank of America’s lease in Charlotte and other smaller move-outs, there may be an intermediate decline in occupancy, impacting short-term revenue and cash flow negatively.

- The need for significant investments and redevelopment projects, such as those at Fifth Third Center and Proscenium, could strain capital resources and affect net margins as these projects require funds and may take time before they contribute to earnings.

- The anticipated market stabilization and convergence of public and private valuations might not happen quickly, which could limit the ability to execute on strategic acquisitions and affect long-term revenue growth projections.

- Competition in key markets like Austin could increase, particularly in the high-demand tech sector, potentially impacting net rents and future revenue growth due to pressures to offer competitive lease terms.

- Continuing operational challenges, such as maintaining occupancy amid corporate move-outs, may require increased leasing incentives or concessions, potentially leading to compressed margins and affecting profitability.

Cousins Properties Future Earnings and Revenue Growth

Assumptions

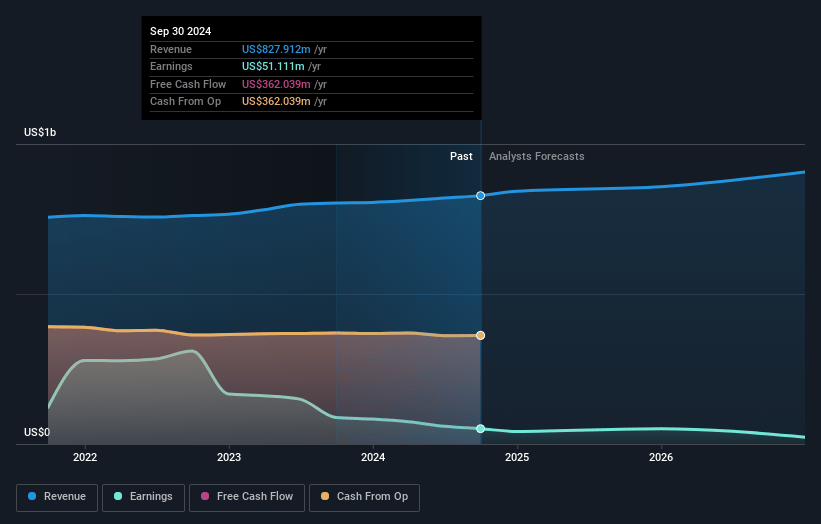

How have these above catalysts been quantified?- Analysts are assuming Cousins Properties's revenue will grow by 4.1% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 6.2% today to 1.0% in 3 years time.

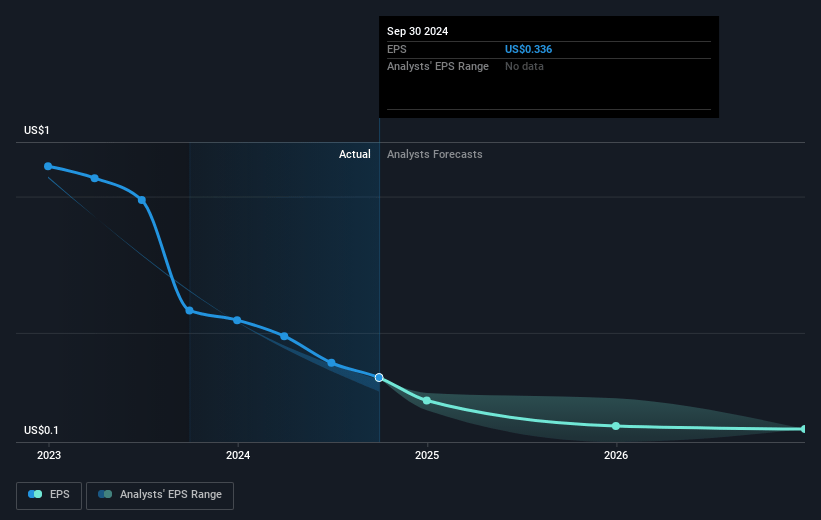

- Analysts expect earnings to reach $9.2 million (and earnings per share of $0.09) by about October 2027, down from $51.1 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 378.5x on those 2027 earnings, up from 91.7x today. This future PE is greater than the current PE for the US Office REITs industry at 63.8x.

- Analysts expect the number of shares outstanding to decline by 13.07% per year for the next 3 years.

- To value all of this in today's dollars, we will use a discount rate of 6.65%, as per the Simply Wall St company report.

Cousins Properties Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's strong third-quarter performance, featuring a high leasing volume and increased cash rent, points to robust revenue growth potential.

- The strategic focus on Sun Belt markets, which are experiencing population and business growth, suggests opportunities for increased occupancy and higher net margins.

- Development of new projects like Neuhoff in Nashville signals potential for future revenue streams and long-term earnings growth.

- Increasing leasing demand and return-to-office trends could lead to higher occupancy rates and bolster the company's revenue.

- With a low leverage and strong credit ratings, Cousins Properties has solid access to capital, which can be advantageous for future investment opportunities and maintaining healthy net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $29.1 for Cousins Properties based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $35.0, and the most bearish reporting a price target of just $19.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $933.7 million, earnings will come to $9.2 million, and it would be trading on a PE ratio of 378.5x, assuming you use a discount rate of 6.7%.

- Given the current share price of $30.81, the analyst's price target of $29.1 is 5.9% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives