Key Takeaways

- Camden expects decreased supply pressure and strong regional demand to improve revenue, net operating income, and occupancy rates.

- Strategic capital recycling and geographic portfolio balancing are anticipated to enhance earnings and return on invested capital.

- Camden's earnings may be pressured by market challenges, rising interest expenses, low revenue growth, high acquisition activity, and potential economic downturns.

Catalysts

About Camden Property Trust- An S&P 500 Company, is a real estate company primarily engaged in the ownership, management, development, redevelopment, acquisition, and construction of multifamily apartment communities.

- Camden anticipates that new supply pressure in the multifamily housing market will decrease throughout 2025, leading to improved revenue and net operating income growth as demand exceeds supply. This expected reduction in supply pressure is likely to enhance Camden's revenue and margins in the near future.

- Camden's strategic plan involves capital recycling by acquiring newer properties and selling older, more capital-intensive properties. This strategy aims to keep their portfolio competitive and lower capital expenses, which should lead to increased earnings and improved return on invested capital.

- The ongoing population growth in Camden's core Sunbelt markets, particularly in Texas and Florida, is projected to continue, offering a robust demand backdrop for Camden's properties. This demographic trend is expected to drive revenue growth and improve occupancy rates.

- Camden plans upticks in acquisitions and dispositions, with a forecast of $750 million for each, as part of restructuring their portfolio for greater geographic balance and efficiency, potentially enhancing their overall earnings profile.

- Camden's expected flat to slightly positive lease trade-out and rental growth, particularly in stronger markets like Tampa and Houston, coupled with high resident retention and favorable economic conditions, are expected to support revenue growth and improve net margin performance going forward.

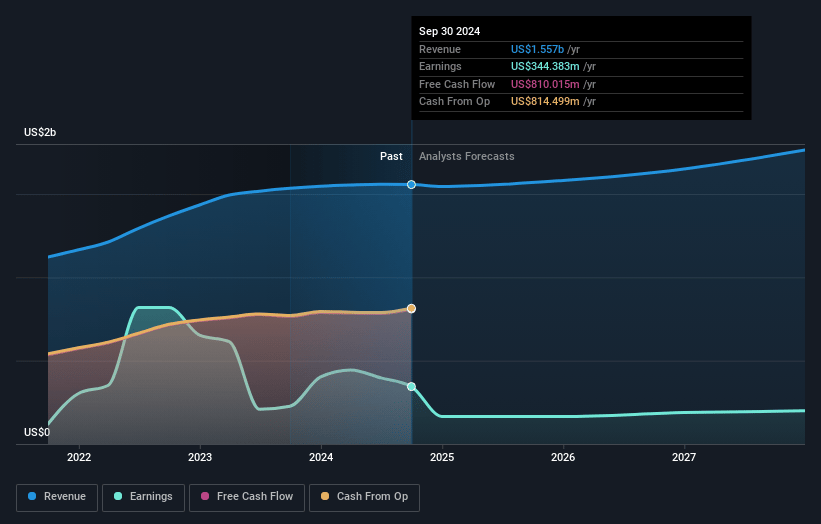

Camden Property Trust Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Camden Property Trust's revenue will grow by 4.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 10.5% today to 13.8% in 3 years time.

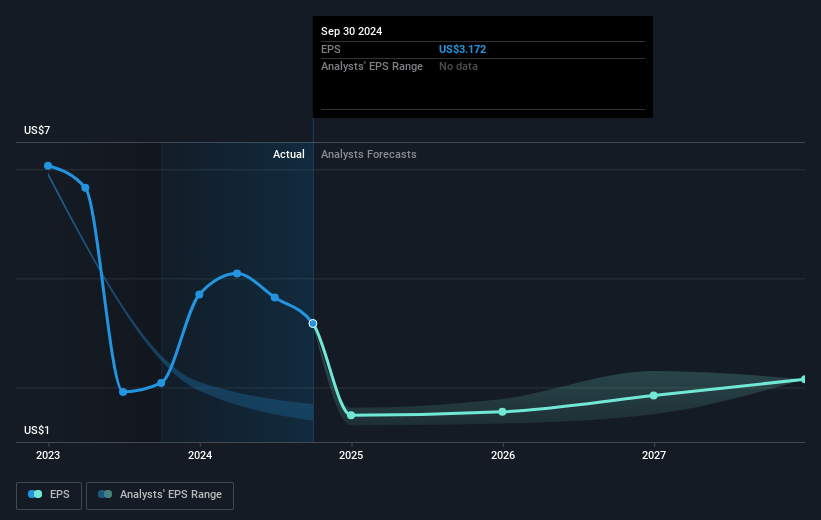

- Analysts expect earnings to reach $241.7 million (and earnings per share of $2.42) by about April 2028, up from $163.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $323.3 million in earnings, and the most bearish expecting $181 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 71.2x on those 2028 earnings, down from 75.5x today. This future PE is greater than the current PE for the US Residential REITs industry at 46.1x.

- Analysts expect the number of shares outstanding to grow by 0.21% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.48%, as per the Simply Wall St company report.

Camden Property Trust Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Camden's significant exposure to markets such as Nashville and Austin, which faced revenue declines in 2024 and are expected to remain challenged due to new supply, could negatively impact revenue growth and result in lower earnings.

- A projected decrease in core FFO per share for 2025, primarily due to increased interest expenses from higher anticipated debt balances, could put pressure on earnings.

- The guidance of same-store revenue growth of only 1% for 2025, with expected expense growth of 3%, indicates potential pressure on net margins and earnings.

- Increased acquisition activity, which involves buying properties before selling others to achieve tax efficiency, could temporarily lead to a negative FFO yield differential, impacting short-term earnings and financial performance.

- Potential adverse effects of fluctuating market conditions, such as unanticipated recessionary pressures impacting economic performance, could dampen broader revenue growth prospects in Camden's markets and affect their overall earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $128.304 for Camden Property Trust based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $148.0, and the most bearish reporting a price target of just $115.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.8 billion, earnings will come to $241.7 million, and it would be trading on a PE ratio of 71.2x, assuming you use a discount rate of 6.5%.

- Given the current share price of $113.16, the analyst price target of $128.3 is 11.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.