Key Takeaways

- Strong leasing activity and high tenant retention in the Defense/IT sector could enhance revenue growth and net margins with stabilized cash flows.

- Strategic developments and budget reallocation towards defense priorities indicate potential long-term earnings growth by aligning with increasing defense spending.

- Uncertain factors like defense reallocation and data center delays may impact leasing demand, revenue growth, and the company's financial flexibility under volatile market conditions.

Catalysts

About COPT Defense Properties- COPT Defense, an S&P MidCap 400 Company, is a self-managed REIT focused on owning, operating and developing properties in locations proximate to, or sometimes containing, key U.S.

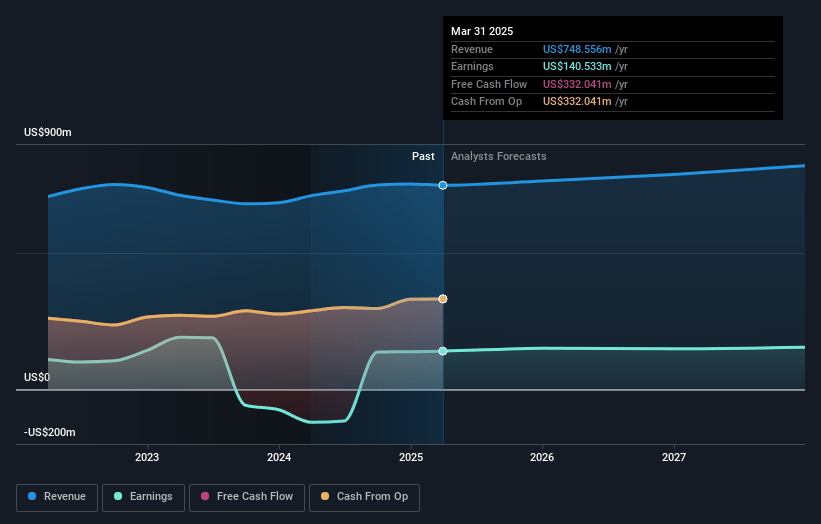

- Strong leasing activity within the Defense/IT sector suggests continued revenue growth, including 179,000 square feet of vacancy leasing and 100,000 square feet of investment leasing year-to-date, indicating potential increases in future revenue streams.

- High tenant retention rates and successful leasing expansions, especially with the Department of Defense and cyber contractors, could result in improved net margins by minimizing vacancy costs and stabilizing cash flows.

- The expectation of increases in defense spending and the reallocation of the defense budget towards priority missions such as cybersecurity and missile defense suggests potential for earnings growth, as COPT’s portfolio supports these key defense priorities.

- Ongoing development projects, like the 150,000 square foot building at Advanced Gateway and strong development leasing pipeline, are likely to drive future revenue increments and support consistent FFO growth.

- Plans for new investments primarily through developments in high-demand areas, while maintaining the balance sheet through self-funded equity components, are expected to provide leverage-neutral growth, positively impacting long-term earnings stability.

COPT Defense Properties Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming COPT Defense Properties's revenue will grow by 3.9% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 18.8% today to 18.4% in 3 years time.

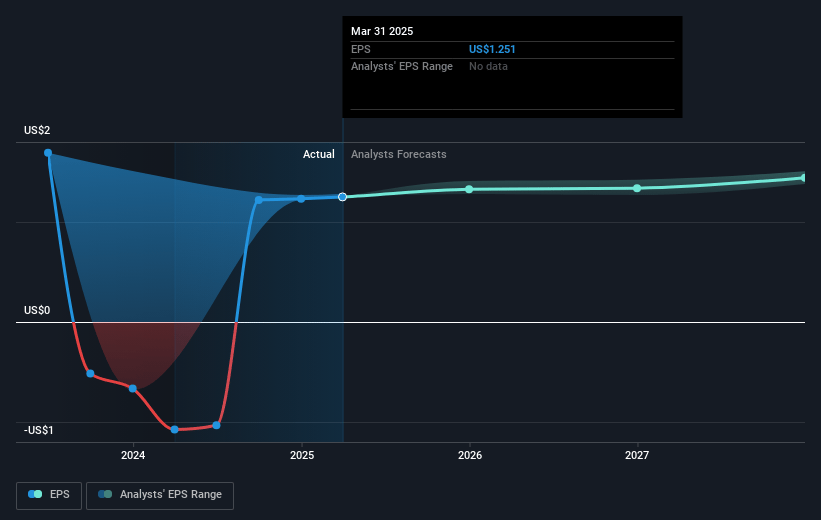

- Analysts expect earnings to reach $154.0 million (and earnings per share of $1.45) by about July 2028, up from $140.5 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $172.8 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 29.5x on those 2028 earnings, up from 22.7x today. This future PE is lower than the current PE for the US Office REITs industry at 50.1x.

- Analysts expect the number of shares outstanding to grow by 0.2% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.48%, as per the Simply Wall St company report.

COPT Defense Properties Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Potential risks from DOGE and defense spending reallocations could create uncertainty in the market. If these lead to budget adjustments affecting COPT tenants, this could impact leasing demand and revenue growth.

- The timing of power availability for data center projects, such as in Iowa, has become more uncertain, potentially elongating expected timelines to 3-4 years, which could delay anticipated revenue from these developments.

- The overall real estate market could be impacted by tariffs and construction cost fluctuations, affecting COPT's ability to maintain targeted yields on new developments, potentially straining net margins.

- With interest rates and credit spreads in the fixed income market experiencing recent volatility, COPT's ability to maintain attractive financing for debt maturities and capital investment could become challenging, impacting their net earnings and financial flexibility.

- Though they anticipate strong retention, COPT's pipeline has a large share of government leases and if any of these face unexpected renewals that are delayed or not executed as planned, this could impact occupancy rates and same-property net operating income growth targets.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $31.857 for COPT Defense Properties based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $38.0, and the most bearish reporting a price target of just $29.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $838.5 million, earnings will come to $154.0 million, and it would be trading on a PE ratio of 29.5x, assuming you use a discount rate of 7.5%.

- Given the current share price of $28.38, the analyst price target of $31.86 is 10.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.