Key Takeaways

- Strategic partnerships with top pharma companies and global health initiatives fuel future revenue growth and enhance IQVIA's reputation.

- AI-driven efficiencies and digital expansion are expected to boost margins and unlock new geographical revenue opportunities.

- Economic and geopolitical challenges, alongside regulation effects and foreign currency fluctuations, threaten IQVIA's revenue stability and profitability.

Catalysts

About IQVIA Holdings- Provides clinical research services, commercial insights, and healthcare intelligence to the life sciences and healthcare industries in the Americas, Europe, Africa, and the Asia-Pacific.

- IQVIA's strategic partnerships with 22 of the top 25 pharma companies and expansion of alliances indicate a solid pipeline for future revenue growth as these collaborations often lead to long-term, high-value contracts.

- Significant advancements in global health initiatives, such as collaborations with the World Health Organization and other health entities, enhance IQVIA's reputation and potential revenue streams from similar high-profile engagements.

- The introduction of a substantial number of AI-enabled applications, including the IQVIA AI Assistant, is expected to drive future efficiency and improve net margins by reducing operational costs and enhancing service capabilities.

- Expansion of IQVIA’s digital business into Europe and the doubling of website integrations into its digital network is anticipated to unlock new revenue opportunities, enhancing earnings through geographical diversification.

- Strong free cash flow growth of 41% and a $3 billion share repurchase authorization support earnings per share improvement, providing a substantial catalyst for stock valuation uplift through shareholder returns.

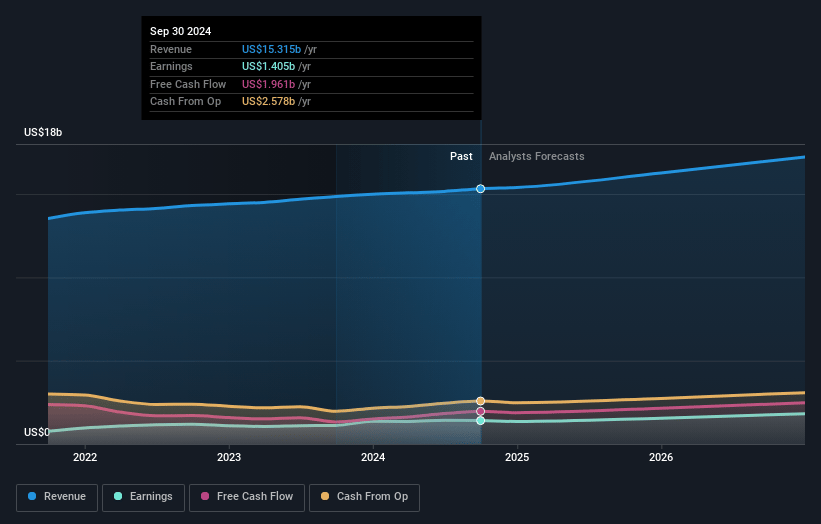

IQVIA Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on IQVIA Holdings compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming IQVIA Holdings's revenue will grow by 6.2% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 8.9% today to 12.6% in 3 years time.

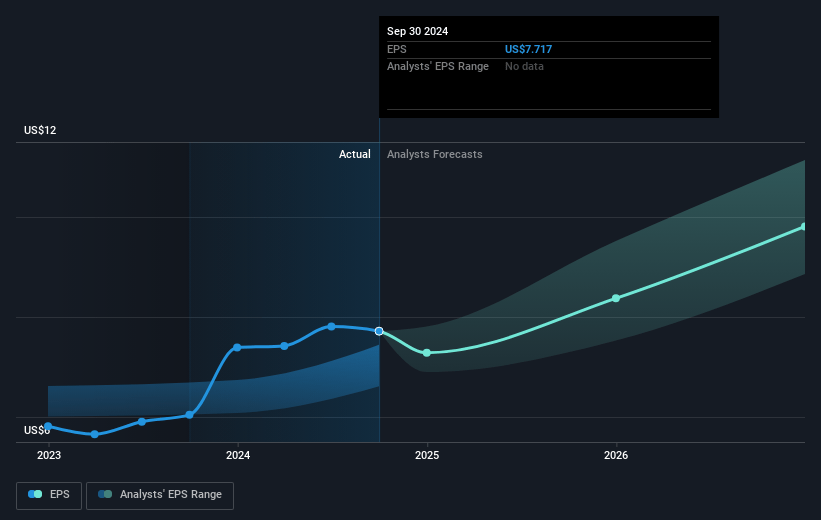

- The bullish analysts expect earnings to reach $2.3 billion (and earnings per share of $12.67) by about April 2028, up from $1.4 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 22.9x on those 2028 earnings, up from 18.4x today. This future PE is lower than the current PE for the US Life Sciences industry at 36.5x.

- Analysts expect the number of shares outstanding to decline by 3.35% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.93%, as per the Simply Wall St company report.

IQVIA Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- IQVIA faced significant cancellations in 2024, nearly 50% higher than the average of the previous three years, which presents challenges in maintaining stable revenue streams.

- The company dealt with a tough macro environment, including geopolitical unrest, high interest rates, and inflation, which could adversely affect its revenue and profitability.

- Gaps caused by the Inflation Reduction Act led to delayed customer decision-making and reduced discretionary spend, potentially impacting IQVIA's revenue and earnings.

- Volatility in the Research & Development Solutions segment, with some large program delays, may affect IQVIA's short-term revenue and gross margins due to stranded costs.

- Continued foreign currency headwinds could impact IQVIA's revenue and earnings, particularly given the fluctuation in exchange rates observed in recent quarters.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for IQVIA Holdings is $268.0, which is the highest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of IQVIA Holdings's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $268.0, and the most bearish reporting a price target of just $165.0.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be $18.5 billion, earnings will come to $2.3 billion, and it would be trading on a PE ratio of 22.9x, assuming you use a discount rate of 7.9%.

- Given the current share price of $143.61, the bullish analyst price target of $268.0 is 46.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is an employee of Simply Wall St, but has written this narrative in their capacity as an individual investor. AnalystHighTarget holds no position in NYSE:IQV. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. This narrative is general in nature and explores scenarios and estimates created by the author. The narrative does not reflect the opinions of Simply Wall St, and the views expressed are the opinion of the author alone, acting on their own behalf. These scenarios are not indicative of the company's future performance and are exploratory in the ideas they cover. The fair value estimate's are estimations only, and does not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that the author's analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives