Key Takeaways

- Expanding ZYNLONTA into earlier lines of DLBCL through trials could significantly boost revenue by accessing a larger patient population.

- Strategic advancements and research collaborations are poised to enhance profitability and strengthen long-term growth prospects.

- Intense competition and limited market access for treatments, coupled with reliance on uncertain trial outcomes, threaten revenue growth and financial stability.

Catalysts

About ADC Therapeutics- Focuses on advancing its proprietary antibody drug conjugate (ADC) technology platform to transform the treatment paradigm for patients with hematologic malignancies and solid tumors.

- ADC Therapeutics is focused on expanding the use of ZYNLONTA into earlier lines of DLBCL through the LOTIS-5 and LOTIS-7 trials, which could significantly increase revenue if successful due to a larger patient population.

- The company anticipates potential peak revenue of $600 million to $1 billion in the U.S. for ZYNLONTA, driven by expansion into second-line DLBCL and indolent lymphomas, positively impacting earnings and profitability.

- Strategic advancements in ZYNLONTA's clinical profile in combination with other therapies could lead to higher response rates and enhanced market penetration, bolstering revenue growth prospects.

- Successful completion and positive results from upcoming trials and regulatory approvals could enhance the financial stability of ADC Therapeutics by increasing net margins and operating income.

- Potential research collaborations to advance the early-stage solid tumor pipeline and ongoing cost-reduction initiatives could further drive profitability and bolster earnings in the long term.

ADC Therapeutics Future Earnings and Revenue Growth

Assumptions

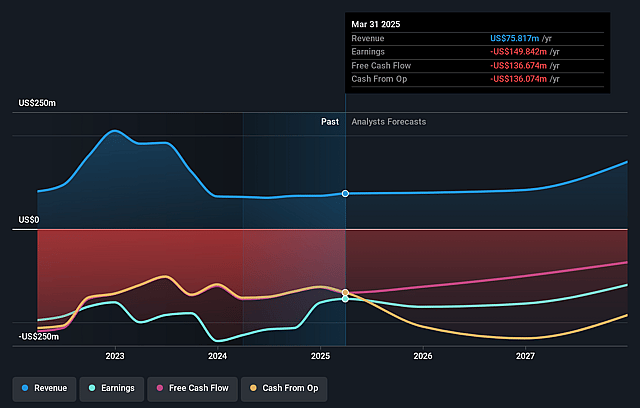

How have these above catalysts been quantified?- Analysts are assuming ADC Therapeutics's revenue will grow by 31.9% annually over the next 3 years.

- Analysts are not forecasting that ADC Therapeutics will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate ADC Therapeutics's profit margin will increase from -197.6% to the average US Biotechs industry of 10.5% in 3 years.

- If ADC Therapeutics's profit margin were to converge on the industry average, you could expect earnings to reach $18.3 million (and earnings per share of $0.15) by about July 2028, up from $-149.8 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 68.8x on those 2028 earnings, up from -2.3x today. This future PE is greater than the current PE for the US Biotechs industry at 16.5x.

- Analysts expect the number of shares outstanding to grow by 2.62% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.35%, as per the Simply Wall St company report.

ADC Therapeutics Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company faces significant competition in the highly competitive third-line plus DLBCL market, impacting revenue stability and growth potential.

- Despite ongoing efforts to expand ZYNLONTA's use in earlier lines of therapy, market research indicates only about 50% of the second-line population may access or be suitable for these treatments, potentially limiting revenue growth.

- Clinical trial outcomes are uncertain, and the reliance on pivotal trials such as LOTIS-5 and LOTIS-7 to meet regulatory approval and market acceptance poses execution risk, potentially affecting earnings.

- Continued progression in the exatecan-based preclinical candidates involves inherent risk, and any delay or failure in research collaborations could impact future revenue prospects.

- The company has reported consistent net losses despite reduced operating expenses, and failure to achieve projected peak revenues could further strain net margins and financial health.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $8.2 for ADC Therapeutics based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $10.0, and the most bearish reporting a price target of just $5.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $174.0 million, earnings will come to $18.3 million, and it would be trading on a PE ratio of 68.8x, assuming you use a discount rate of 8.4%.

- Given the current share price of $3.05, the analyst price target of $8.2 is 62.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.