Key Takeaways

- Ignite transformation aims to boost growth through new pricing, digital improvements, and cost savings, enhancing revenues and margins.

- Collaboration with ABB Robotics and Infinity series launches strengthen market position, driving revenue through automation and integrated solutions.

- Fluctuations in currency, economic conditions, and governmental policies could impact Agilent's revenue and growth, introducing risks and potential volatility.

Catalysts

About Agilent Technologies- Provides application focused solutions to the life sciences, diagnostics, and applied chemical markets worldwide.

- The implementation of Agilent's Ignite transformation is expected to drive growth through new pricing mechanisms, improved digital ecosystem, and procurement cost savings, aiming to increase core revenues by 5-7% annually and expand operating margins by 50 to 100+ basis points per year, thus enhancing revenue and net margins.

- Agilent's collaboration with ABB Robotics to produce automated laboratory solutions is intended to transform lab operations in multiple markets, aiming to improve workflow efficiency and flexibility, which could boost revenue by attracting more customers seeking integrated lab solutions.

- The successful launch and adoption of the Infinity III series, with its advanced automation and backward compatibility, is creating an opportunity to replace and upgrade customers' instruments across Agilent's legacy LC platforms, contributing to future revenue growth as customers choose Agilent for their technology refreshes.

- Agilent continues to focus on software and informatics as a key area of opportunity, with products like the Infinity LabAssist automation software and OpenLab CDS seeing positive customer responses, which could enhance earnings through higher-margin software sales.

- Agilent's market leadership and increased win rates in China, especially due to capturing stimulus-related tenders and the demand for PFAS testing solutions, highlight an opportunity for revenue growth in the region and globally as environmental regulations drive demand for testing solutions.

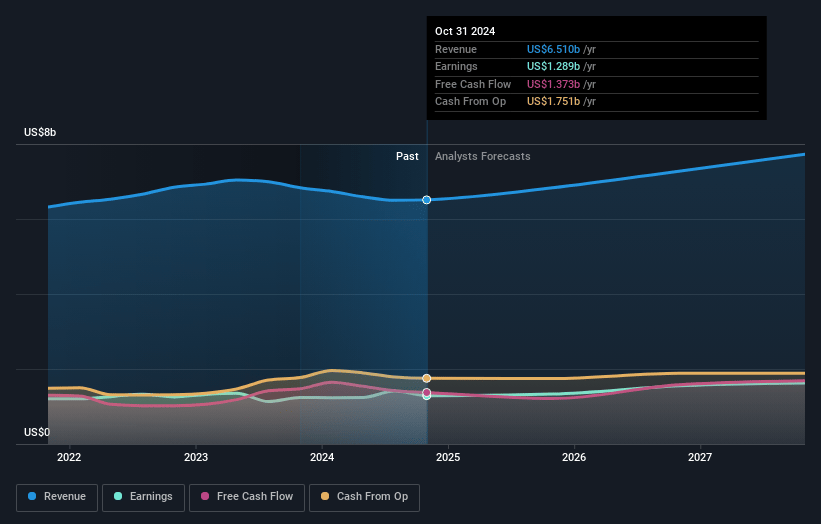

Agilent Technologies Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Agilent Technologies's revenue will grow by 5.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 19.3% today to 22.3% in 3 years time.

- Analysts expect earnings to reach $1.7 billion (and earnings per share of $6.27) by about April 2028, up from $1.3 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 27.0x on those 2028 earnings, up from 24.3x today. This future PE is lower than the current PE for the US Life Sciences industry at 37.8x.

- Analysts expect the number of shares outstanding to decline by 2.28% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.0%, as per the Simply Wall St company report.

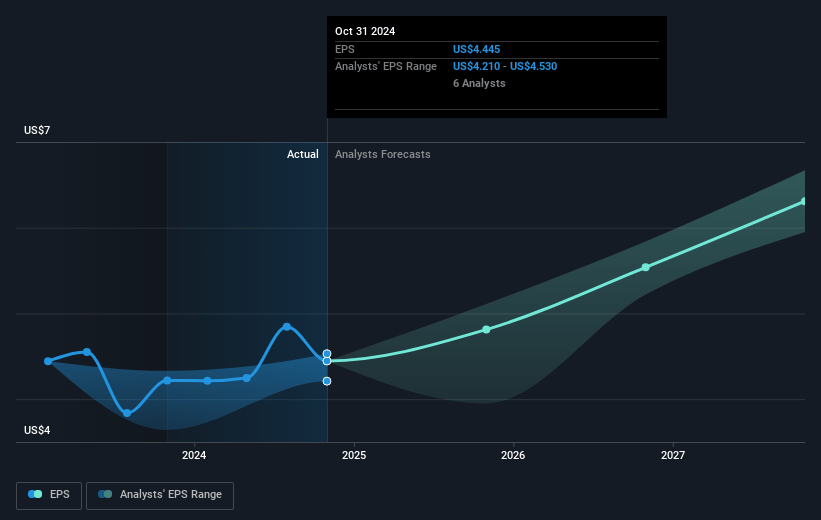

Agilent Technologies Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Agilent's exposure to NIH-related programs is limited, but potential reductions in funding could still have some impact on their revenue.

- The strengthening of the U.S. dollar is expected to create a currency headwind, impacting Agilent’s reported revenue and potentially affecting net margins.

- The cyclical nature of product replacement, like LC and GC instruments, might lead to an uneven revenue stream, affecting earnings if replacement cycles slow down.

- Concerns regarding the impact of possible U.S. federal budget uncertainty may introduce financial risk, potentially impacting revenue outlooks.

- China's economic and political environment, including stimulus timelines and stimulus budget allocations, creates uncertainties that could affect Agilent's revenue and growth outlook in that region.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $142.765 for Agilent Technologies based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $165.0, and the most bearish reporting a price target of just $115.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $7.7 billion, earnings will come to $1.7 billion, and it would be trading on a PE ratio of 27.0x, assuming you use a discount rate of 7.0%.

- Given the current share price of $107.46, the analyst price target of $142.76 is 24.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.