Key Takeaways

- New product launches and late-stage developments are expected to drive future revenue growth and improve net margins through higher-margin innovations.

- Operational expense reviews aim to enhance efficiencies and reduce costs, supporting margin improvements and boosting long-term economic value.

- Compliance and operational challenges, alongside financial pressures and shareholder priorities, may impede Viatris' revenue stability, margin growth, and long-term strategic investments.

Catalysts

About Viatris- Operates as a healthcare company in North America, Europe, China, Taiwan, Hong Kong, Japan, Australia, New Zealand, rest of Asia, Africa, Latin America, and the Middle East.

- The expansion of Viatris' innovative portfolio with new products like selatogrel, cenerimod, and sotagliflozin, and late-stage development milestones planned in 2025, are expected to bolster future revenue and net margin improvements through higher-margin innovations.

- The focus on several notable new product launches in 2025, including ten unique molecules in Phase III development, is anticipated to drive revenue growth and increase earnings potential in future years with planned launches in both generic and innovative segments.

- The enterprise-wide initiative to review global infrastructure with the aim to deliver operational expense savings in 2026 and beyond is expected to improve net margins by reducing costs and enhancing operational efficiencies.

- The strategic decision to increase territories for cenerimod in Asia and reduce contingent milestone payments in a collaboration with Idorsia is likely to benefit long-term economic value, potentially impacting revenue and sustaining margin expansion.

- A committed capital return strategy prioritizing share repurchases (target $500 million to $650 million in 2025) alongside sustaining dividends is intended to enhance EPS, supported by strong free cash flow generation and disciplined capital allocation.

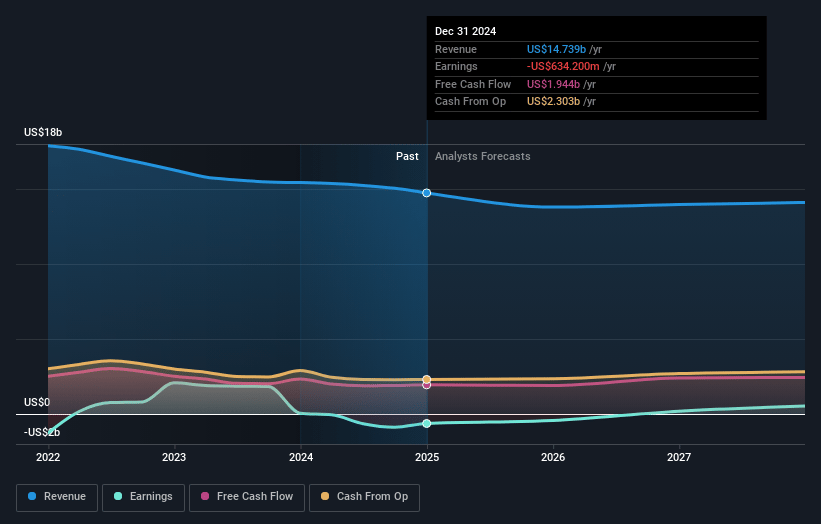

Viatris Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Viatris's revenue will decrease by 1.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from -4.3% today to 3.7% in 3 years time.

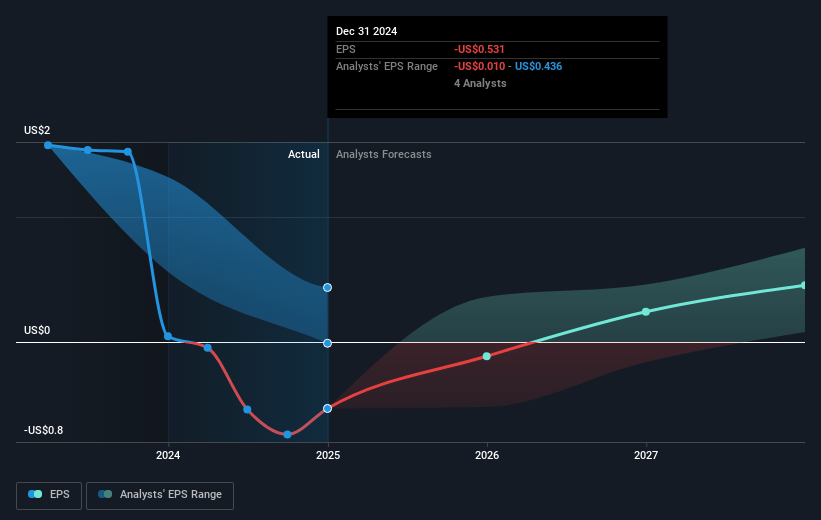

- Analysts expect earnings to reach $525.2 million (and earnings per share of $0.45) by about April 2028, up from $-634.2 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $840.9 million in earnings, and the most bearish expecting $86 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 33.1x on those 2028 earnings, up from -14.2x today. This future PE is greater than the current PE for the US Pharmaceuticals industry at 15.9x.

- Analysts expect the number of shares outstanding to grow by 0.25% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.23%, as per the Simply Wall St company report.

Viatris Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The FDA warning letter and import alert concerning the Indore facility could negatively impact Viatris’ ability to distribute 11 key products in the U.S., leading to a significant estimated $500 million reduction in 2025 revenues and a $385 million hit to adjusted EBITDA, affecting overall profitability and financial stability.

- The inability to secure FDA exceptions for key products such as lenalidomide, coupled with expected additional generic competition by 2026, highlights risks to maintaining revenue streams and margin pressures for the company.

- There is potential for broader quality control issues as seen with the pending classification of the Nashik, India facility inspection. This uncertainty can strain operational continuity and potentially jeopardize corporate reputation, which might impact revenue and expenses.

- The need for significant spending on facility remediation and uncertainties around FDA reinspections could delay revenue recovery, pressuring net margins with additional remedial costs and penalties.

- Viatris’ commitment to increasing capital return to shareholders over business development in the near term may limit financial resources available for strategic investments needed to drive longer-term revenue growth and diversification away from at-risk and declining product lines.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $11.747 for Viatris based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $14.0, and the most bearish reporting a price target of just $8.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $14.1 billion, earnings will come to $525.2 million, and it would be trading on a PE ratio of 33.1x, assuming you use a discount rate of 7.2%.

- Given the current share price of $7.57, the analyst price target of $11.75 is 35.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.