Key Takeaways

- Internalization of management and acquisition strategies are expected to enhance financial performance and operational alignment, leading to improved margins and efficiency.

- Expansion through synthetic royalties and strategic share repurchases demonstrates focus on new revenue streams and maximizing shareholder value.

- Integration challenges and potential legal uncertainties may delay revenue and savings, impacting net margins, cash flow, and future earnings stability.

Catalysts

About Royalty Pharma- Operates as a buyer of biopharmaceutical royalties and a funder of innovation in the biopharmaceutical industry in the United States.

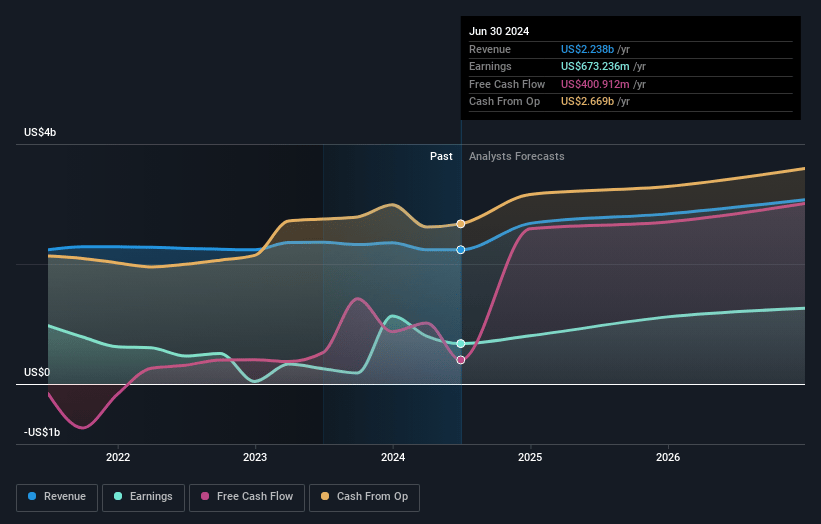

- The internalization of management is projected to yield financial benefits by eliminating the 6.5% management fee that Royalty Pharma has historically paid. This will improve net margins and increase net returns on royalty investments, with cash savings expected to surpass $100 million by 2026 and a cumulative $1.6 billion over the next decade.

- The planned acquisition of the external manager, expected to close in the second quarter of 2025, will enhance operational alignment and continuity, potentially improving earnings due to greater integration and efficiencies within Royalty Pharma's operations.

- A significant catalyst for revenue growth is the projected addition of $430 million to annual Portfolio Receipts from five launching therapies that are either first or best-in-class, with total consensus peak sales forecasts reaching over $10 billion.

- Royalty Pharma's strategic focus on synthetic royalties is seen as a true win-win for partners, enabling the company to create new revenue streams and potentially achieving high returns on investment. This sector represents a growing contribution to revenue, with synthetic royalty transactions more than doubling since 2020 to $925 million in 2024.

- The aggressive share repurchase program, authorized at $3 billion with an intention to repurchase $2 billion in 2025, suggests a strategic capital allocation to increase earnings per share, signaling confidence in the intrinsic value of their stock and potential undervaluation in the current market.

Royalty Pharma Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on Royalty Pharma compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Royalty Pharma's revenue will grow by 16.0% annually over the next 3 years.

- The bullish analysts assume that profit margins will shrink from 37.9% today to 26.1% in 3 years time.

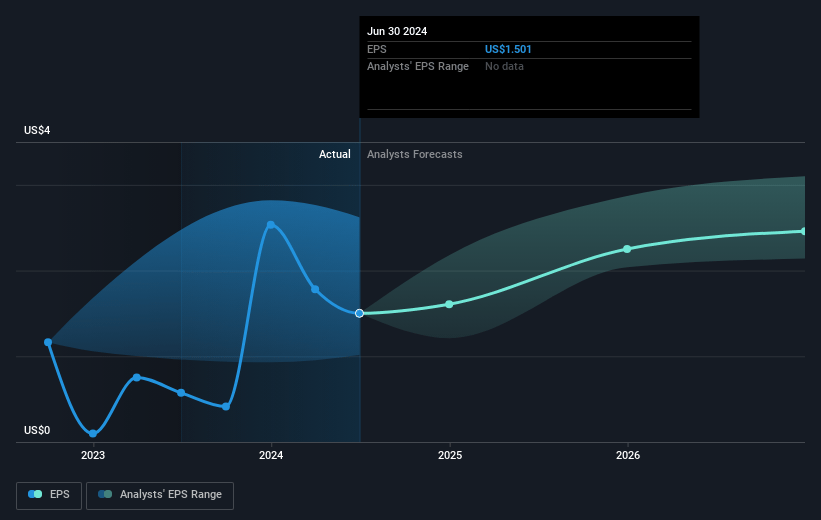

- The bullish analysts expect earnings to reach $922.0 million (and earnings per share of $2.6) by about April 2028, up from $859.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 31.2x on those 2028 earnings, up from 16.2x today. This future PE is greater than the current PE for the US Pharmaceuticals industry at 16.1x.

- Analysts expect the number of shares outstanding to decline by 3.92% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.21%, as per the Simply Wall St company report.

Royalty Pharma Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company faces execution risk in integrating its external manager, which might impact its ability to realize expected cash savings, thus affecting net margins and earnings.

- There is uncertainty around the Vertex royalty and Alyftrek arbitration process, which could delay revenue streams and create potential legal costs, thus impacting net income and cash flow.

- Legislative and policy changes related to healthcare by the administration could pose unexpected risks to royalties, potentially affecting revenue outlook and net margins.

- The company's investment strategy heavily relies on synthetic royalties, a relatively new market approach, posing risks if market demand or conditions change, thereby impacting future earnings and revenue stability.

- The anticipated benefits from the internalization do not reflect in the current cost structure, and any delay or issue with this integration could add unforeseen expenses or savings delays, thereby affecting the bottom line profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for Royalty Pharma is $47.0, which is the highest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Royalty Pharma's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $47.0, and the most bearish reporting a price target of just $30.14.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be $3.5 billion, earnings will come to $922.0 million, and it would be trading on a PE ratio of 31.2x, assuming you use a discount rate of 6.2%.

- Given the current share price of $32.19, the bullish analyst price target of $47.0 is 31.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is an employee of Simply Wall St, but has written this narrative in their capacity as an individual investor. AnalystHighTarget holds no position in NasdaqGS:RPRX. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. This narrative is general in nature and explores scenarios and estimates created by the author. The narrative does not reflect the opinions of Simply Wall St, and the views expressed are the opinion of the author alone, acting on their own behalf. These scenarios are not indicative of the company's future performance and are exploratory in the ideas they cover. The fair value estimate's are estimations only, and does not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that the author's analysis may not factor in the latest price-sensitive company announcements or qualitative material.