Last Update01 May 25Fair value Increased 0.18%

AnalystConsensusTarget made no meaningful changes to valuation assumptions.

Read more...Key Takeaways

- Strategic partnerships and agreements are expected to drive significant revenue and market expansion, particularly in MRD testing and tumor profiling.

- Investments and collaborations with major companies should enhance distribution and efficiency, improving revenue and margins through economies of scale.

- Dependence on partnerships, Medicare reimbursement, and competitive market dynamics could impact Personalis's revenue growth and financial stability significantly.

Catalysts

About Personalis- Develops, markets, and sells advanced cancer genomic tests and services in the United States and internationally.

- Personalis is poised to capitalize on the growing MRD (minimal residual disease) testing market, expected to mature into a $20 billion market, with its ultra-sensitive test, NeXT Personal, which can improve early cancer detection and patient therapy effectiveness. This is anticipated to drive significant revenue growth.

- The long-term extension of Personalis' agreement with Moderna to support clinical trials and commercialization with their personalized tumor profiling capabilities represents a key expected driver of revenue growth over the next decade.

- Achieving CMS reimbursement for at least two cancer-related indications in 2025, bolstered by anticipated publications of clinical evidence in peer-reviewed journals, is expected to significantly increase clinical test volume and revenue, as well as improve net margins through higher reimbursement rates.

- Strategic investments by Tempus and Merck, and the partnership with these companies, are expected to boost distribution, expand commercial reach, and increase test volumes, leading to increased revenue and potentially improved net margins due to economies of scale.

- The focus on expanding the biopharma customer base through the ImmunoID NeXT platform and evolving tumor profiling products is anticipated to drive growth in biopharma revenue, while also potentially enhancing earnings through improved efficiency in clinical trial processes.

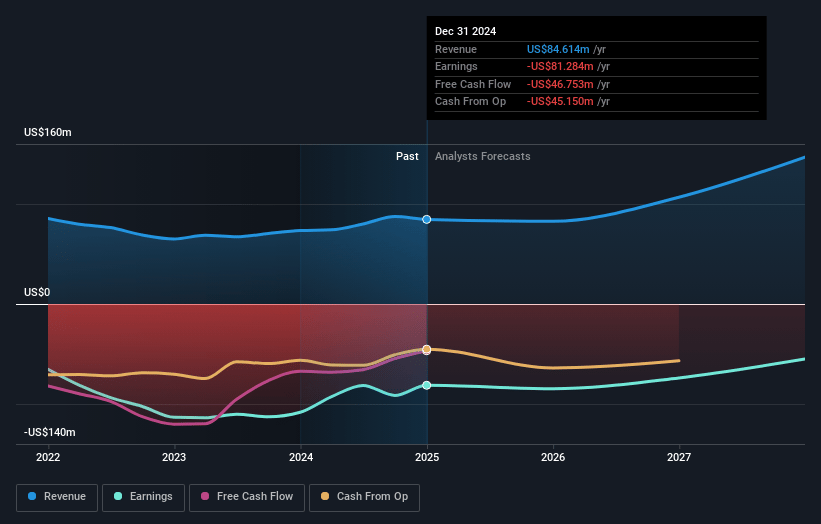

Personalis Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Personalis's revenue will grow by 20.2% annually over the next 3 years.

- Analysts are not forecasting that Personalis will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Personalis's profit margin will increase from -96.1% to the average US Life Sciences industry of 12.9% in 3 years.

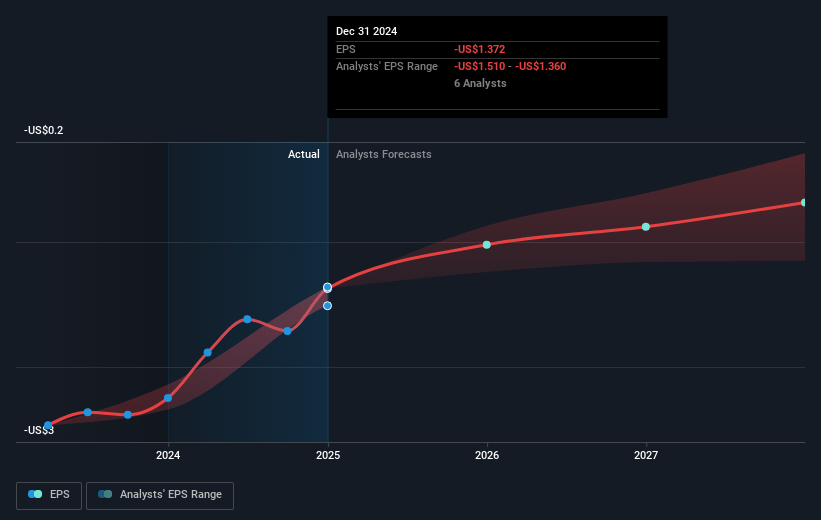

- If Personalis's profit margin were to converge on the industry average, you could expect earnings to reach $18.9 million (and earnings per share of $0.18) by about May 2028, up from $-81.3 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 51.3x on those 2028 earnings, up from -4.1x today. This future PE is greater than the current PE for the US Life Sciences industry at 37.8x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.03%, as per the Simply Wall St company report.

Personalis Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's dependency on partnerships, such as the long-term agreement with Moderna and the critical role of Tempus in clinical distribution, represents a risk if these partnerships do not yield the expected results or dissolve, which could impact future revenue growth and market penetration.

- The financial performance is heavily reliant on achieving Medicare reimbursement for specific cancer indications; delays or failures in obtaining reimbursement for some indications may significantly hinder revenue expectations and bottom-line outcomes.

- Personalis faces competition within the rapidly evolving MRD testing market. The progress and breakthrough by competitors with alternative technologies could eat into market share and negatively affect revenue growth.

- The reliance on biopharma customers and clinical trials, notably those associated with Moderna, exposes the company to volatility in biopharma R&D cycles and clinical trial funding, potentially impacting revenue stability and growth forecasts.

- Unreimbursed test costs currently weigh down profitability, impacting gross margins significantly. Prolonged periods before reimbursement is achieved could lead to sustained financial pressures, including net margins and cash usage, thereby exacerbating the risk of needing additional capital beyond current reserves.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $7.333 for Personalis based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $9.0, and the most bearish reporting a price target of just $5.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $146.9 million, earnings will come to $18.9 million, and it would be trading on a PE ratio of 51.3x, assuming you use a discount rate of 7.0%.

- Given the current share price of $3.8, the analyst price target of $7.33 is 48.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.