Key Takeaways

- AXPAXLI's FDA amendment enables better dosing schedules, boosting market penetration and revenue through superior treatment durability.

- SOL-R trial adjustments improve capital efficiency and net margins, while complementary trial designs enhance regulatory approval chances and product differentiation.

- Regulatory uncertainties and trial risks may delay revenue and market approval, while unanticipated costs in NPDR and DME could impact financial stability.

Catalysts

About Ocular Therapeutix- A biopharmaceutical company, engages in the development and commercialization of therapies for retinal diseases and other eye conditions using its bioresorbable hydrogel-based formulation technology in the United States.

- AXPAXLI's FDA approval for an amendment allowing redosing at week 52 and 76 could lead to a 6-12 month dosing label in wet AMD, potentially increasing market penetration and revenue growth due to its best-in-class durability.

- The adjustment in SOL-R trial size from 825 to 555 subjects without compromising statistical power enhances capital efficiency and accelerates the process, likely positively impacting net margins by reducing costs.

- The complementary design of the SOL-1 and SOL-R trials aims to optimize regulatory approval chances and provide extensive data, which can support a differentiated and commercially attractive product label, potentially driving future earnings.

- AXPAXLI's potential expansion into nonproliferative diabetic retinopathy and diabetic macular edema presents a substantial opportunity to capture untreated market segments, likely contributing to revenue growth.

- Ocular Therapeutix is well-financed with cash runway into 2028, allowing for robust execution of strategic objectives without dilutive capital raises, positively affecting earnings and shareholder value.

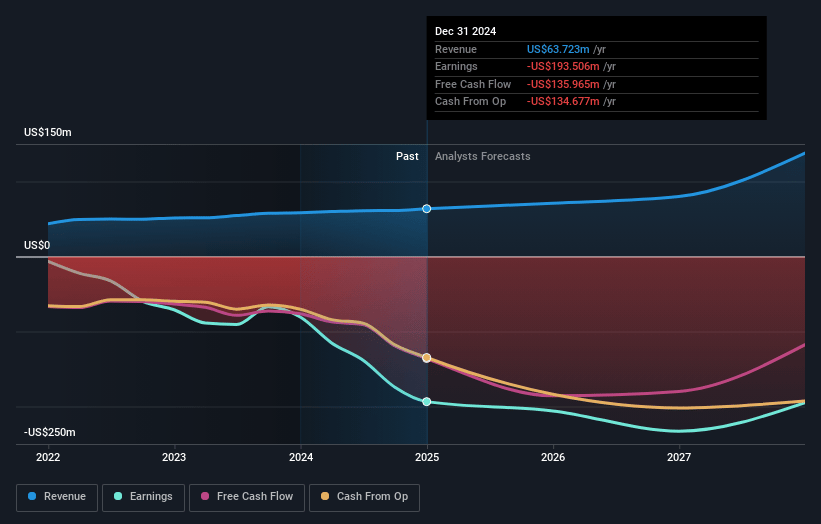

Ocular Therapeutix Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Ocular Therapeutix's revenue will grow by 29.3% annually over the next 3 years.

- Analysts are not forecasting that Ocular Therapeutix will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Ocular Therapeutix's profit margin will increase from -303.7% to the average US Pharmaceuticals industry of 20.5% in 3 years.

- If Ocular Therapeutix's profit margin were to converge on the industry average, you could expect earnings to reach $28.2 million (and earnings per share of $0.16) by about April 2028, up from $-193.5 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 127.6x on those 2028 earnings, up from -5.4x today. This future PE is greater than the current PE for the US Pharmaceuticals industry at 16.2x.

- Analysts expect the number of shares outstanding to grow by 2.67% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.21%, as per the Simply Wall St company report.

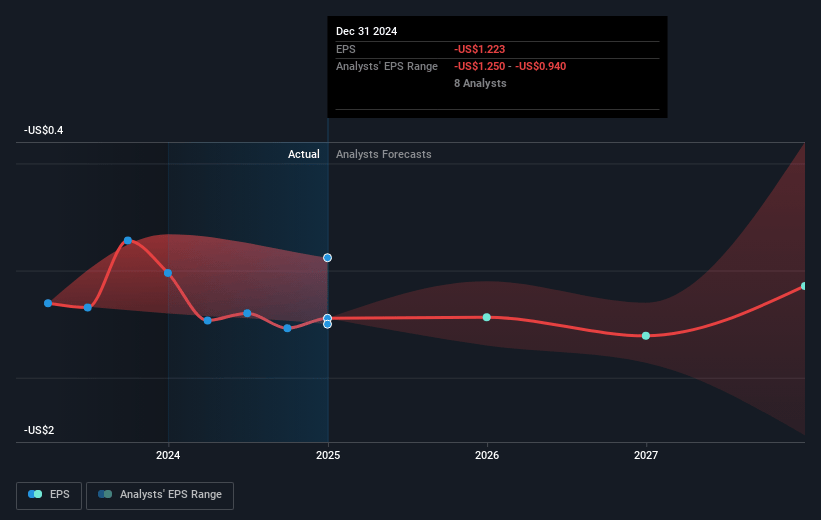

Ocular Therapeutix Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Regulatory and clinical uncertainties remain, particularly around the FDA's requirements and feedback, which could lead to delays in approval and impact timelines for potential revenue generation.

- The reliance on successful trial outcomes for market approval means any negative results could hinder future earnings and market share in the competitive AMD treatment landscape.

- Changes in trial design and reduction in SOL-R study size, although aimed at efficiency, could bring statistical risks that might affect the strength of the regulatory submission and, subsequently, revenue forecasts.

- Limited current market penetration for nonproliferative diabetic retinopathy (NPDR) therapies could indicate challenges in capturing new market segments, potentially constraining future revenue streams.

- Financial projections do not account for all potential clinical trial costs, particularly in NPDR and diabetic macular edema (DME) areas; unforeseen expenses or funding needs could impact cash flow and net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $17.455 for Ocular Therapeutix based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $22.0, and the most bearish reporting a price target of just $14.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $137.8 million, earnings will come to $28.2 million, and it would be trading on a PE ratio of 127.6x, assuming you use a discount rate of 6.2%.

- Given the current share price of $6.54, the analyst price target of $17.45 is 62.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.