Key Takeaways

- Strategic licensing and partnerships are set to enhance revenue potential, cash flow, and international earnings, improving the company's financial outlook.

- Expansion through new and planned product launches, complemented by promising Phase III trials, could drive growth in revenues and net margins.

- Ionis Pharmaceuticals faces revenue growth uncertainties due to FDA changes, patient identification challenges, costly product launches, and reliance on volatile licensing deals.

Catalysts

About Ionis Pharmaceuticals- A commercial-stage biotechnology company, provides RNA-targeted medicines in the United States.

- Ionis Pharmaceuticals has completed two strategic licensing transactions that have improved their 2025 financial guidance by enabling higher expected revenue and cash, as well as improved operating loss, likely impacting future revenue and earnings.

- The recent successful commercial launch of TRYNGOLZA, the first FDA-approved treatment for Familial Chylomicronemia Syndrome, exceeded expectations and is anticipated to contribute to ongoing revenue growth.

- With three additional independent product launches planned over the next two years, including donidalorsen for Hereditary Angioedema, Ionis expects substantial growth potential, likely impacting revenue and net margins.

- Ionis plans to report data from two Phase III programs later this year, which, if positive, could extend their product offerings and enhance revenue streams through new indications.

- They are expanding global reach via partnerships, such as their recent agreement for Sobi to commercialize olezarsen outside the U.S., which would increase international revenue and royalties, thus improving the overall earnings outlook.

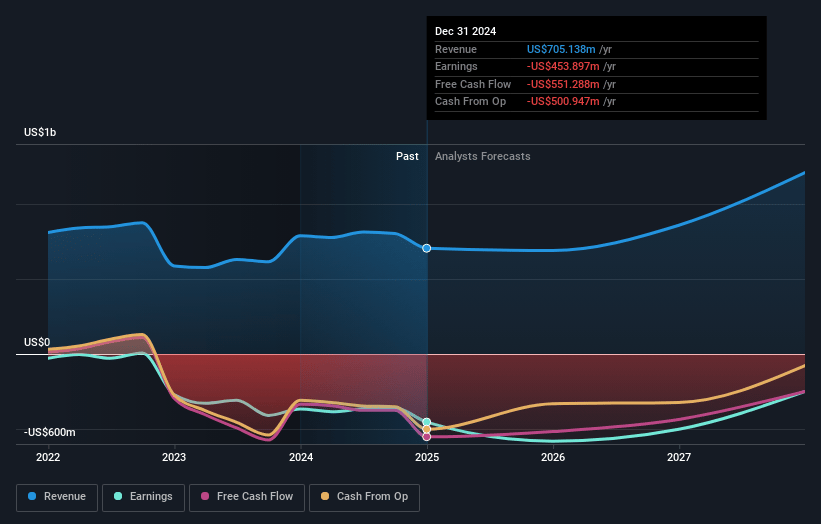

Ionis Pharmaceuticals Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Ionis Pharmaceuticals's revenue will grow by 18.8% annually over the next 3 years.

- Analysts are not forecasting that Ionis Pharmaceuticals will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Ionis Pharmaceuticals's profit margin will increase from -64.4% to the average US Biotechs industry of 15.9% in 3 years.

- If Ionis Pharmaceuticals's profit margin were to converge on the industry average, you could expect earnings to reach $187.6 million (and earnings per share of $0.97) by about May 2028, up from $-453.9 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 72.8x on those 2028 earnings, up from -10.4x today. This future PE is greater than the current PE for the US Biotechs industry at 20.4x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.12%, as per the Simply Wall St company report.

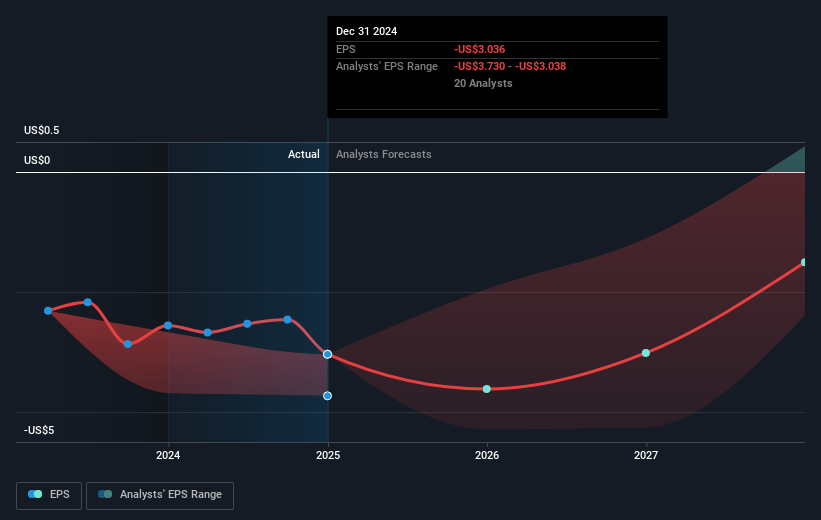

Ionis Pharmaceuticals Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Recent changes at the FDA and the introduction of new tariff policies have introduced uncertainty, which could potentially disrupt the industry and impact Ionis's future revenue growth.

- While TRYNGOLZA has had a successful initial launch, the vast majority of the estimated 3,000 FCS patients in the U.S. remain unidentified, highlighting significant challenges in patient identification that could slow revenue growth.

- The Phase III studies are not powered for certain secondary endpoints like AP reduction in acute pancreatitis, leading to uncertainties in obtaining favorable label outcomes, which could affect market uptake and revenue.

- The cost structure is expected to rise as SG&A expenses increase due to the support needed for ongoing and planned product launches, which could impact net margins.

- Ionis has streamlined P&L reporting but the heavy reliance on successful licensing transactions to boost revenue guidance suggests potential volatility and dependency on licensing deals, impacting earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $57.31 for Ionis Pharmaceuticals based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $78.0, and the most bearish reporting a price target of just $37.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.2 billion, earnings will come to $187.6 million, and it would be trading on a PE ratio of 72.8x, assuming you use a discount rate of 7.1%.

- Given the current share price of $29.81, the analyst price target of $57.31 is 48.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.