Key Takeaways

- Strategic partnerships and biotech opportunities are set to enhance revenue growth and influence future revenue streams.

- Automation and AI-driven digital innovation aim to improve efficiencies and stabilize earnings through cost savings and faster trial completions.

- Growing reliance on digital innovation and automation investments may risk margins if cost efficiencies are not achieved as anticipated.

Catalysts

About ICON- A clinical research organization, provides outsourced development and commercialization services in Ireland, rest of Europe, the United States, and internationally.

- Significant strategic partnerships beyond the top 20 pharma cohort and improved opportunities in the biotech sector indicate a boost in revenue growth as the transition period concludes, impacting upcoming revenue streams.

- New solutions launching this year to enhance efficiencies, such as resource forecasting and site contracting, indicate improvement in ICON’s service delivery, potentially increasing net margins through operational efficiencies.

- Ongoing digital innovation integrating AI and technology improvements in clinical delivery could result in faster, cheaper, and more efficient trial completions, positively influencing future earnings.

- Progression in therapeutic areas like cardiometabolic diseases and oncology, with increased new award growth on a full-service basis, suggests future revenue streams as these awards transition into active projects.

- Comprehensive automation strategies aiming to save over $100 million annually highlight efforts to streamline costs, likely indicating improved net margins and subsequent earnings stability.

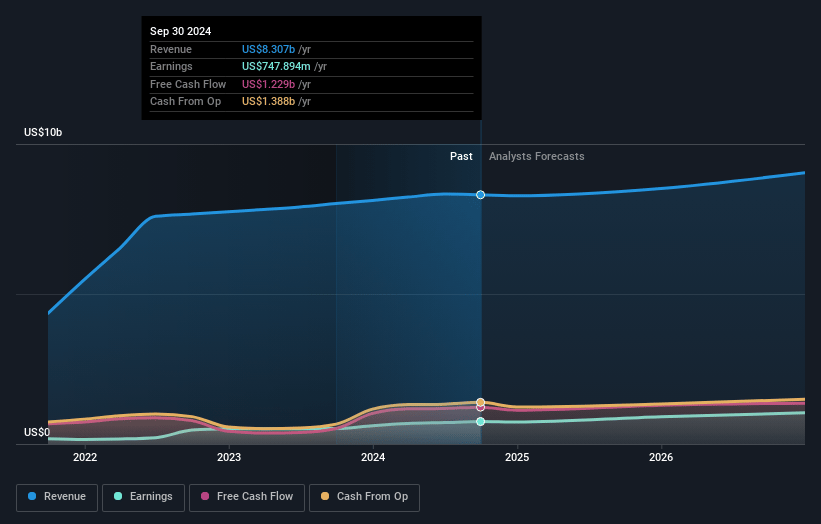

ICON Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming ICON's revenue will grow by 4.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 9.6% today to 11.6% in 3 years time.

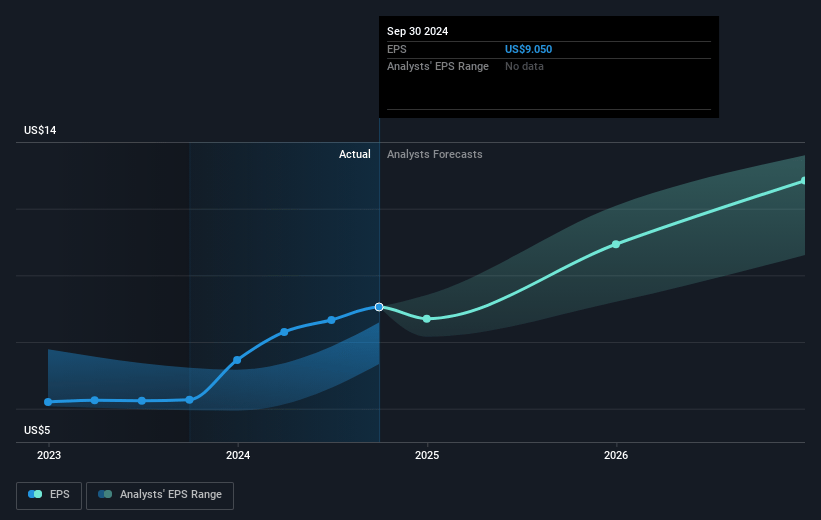

- Analysts expect earnings to reach $1.1 billion (and earnings per share of $14.25) by about March 2028, up from $791.5 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $1.3 billion in earnings, and the most bearish expecting $976 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 21.7x on those 2028 earnings, up from 19.0x today. This future PE is lower than the current PE for the US Life Sciences industry at 42.5x.

- Analysts expect the number of shares outstanding to decline by 2.33% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.01%, as per the Simply Wall St company report.

ICON Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The biotech market is experiencing careful capital allocation and cautiousness, leading to delays in decision-making and trial starts, which could negatively impact revenue growth and margins.

- Increased cancellations in various divisions, including biotech and large pharma, represent a risk to near-term revenue and margin stability.

- The company's focus on digital innovation and automation strategy requires ongoing investment, which, while driving efficiency, also poses a risk to net margins if cost savings do not materialize as planned.

- The mixed outlook for R&D spending in large pharma, with some facing budgetary pressures, may lead to disruptions in overall spend, affecting revenue flow and earnings.

- The reliance on new strategic partnerships for future growth may introduce execution risks if these partnerships do not perform as expected, potentially impacting revenue and earnings projections.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $249.353 for ICON based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $290.0, and the most bearish reporting a price target of just $203.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $9.4 billion, earnings will come to $1.1 billion, and it would be trading on a PE ratio of 21.7x, assuming you use a discount rate of 8.0%.

- Given the current share price of $186.56, the analyst price target of $249.35 is 25.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives