Key Takeaways

- Medicare Part D reform and competitive oncology dynamics are major challenges, significantly impacting Gilead's revenue growth potential.

- Declining Veklury sales and foreign exchange headwinds further suppress revenue, complicating efforts to improve financial metrics.

- Gilead Sciences anticipates sustained growth through its expanding HIV and liver disease portfolios, oncology advances, and stable patent exclusivity until late 2033.

Catalysts

About Gilead Sciences- A biopharmaceutical company, discovers, develops, and commercializes medicines in the areas of unmet medical need in the United States, Europe, and internationally.

- The implementation of Medicare Part D reform is expected to negatively impact Gilead's revenue by approximately $1.1 billion in 2025, including $900 million in HIV, effectively resulting in flat HIV revenue for the year despite ongoing demand growth. This reform will significantly hamper revenue generation.

- Competitive dynamics in oncology, specifically within the cell therapy landscape, are presenting challenges to market penetration and uptake, thereby constraining revenue and profit growth potential in this therapeutic area.

- The planned commercial launch of anito-cel in 2026 may face hurdles due to the current slower-than-targeted uptake of cell therapy as a class globally, potentially limiting future revenue growth and impacting earnings from the oncology segment.

- With Veklury sales declining due to reduced COVID-19 hospitalizations and expected to decrease by approximately $400 million in 2025, total product revenue growth is facing a downturn, adversely affecting overall revenue.

- Foreign exchange headwinds could further suppress revenue growth by approximately $250 million in 2025, complicating Gilead's efforts to improve financial metrics like revenue and earnings.

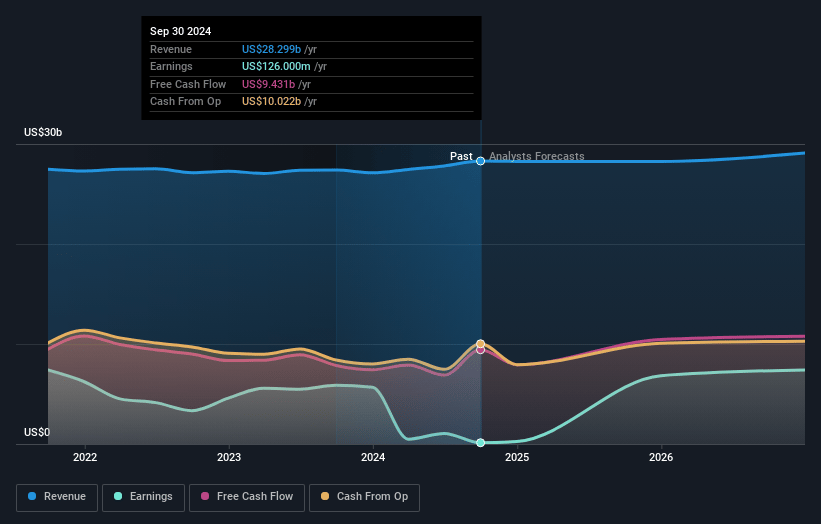

Gilead Sciences Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Gilead Sciences compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Gilead Sciences's revenue will decrease by 0.7% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 1.7% today to 25.8% in 3 years time.

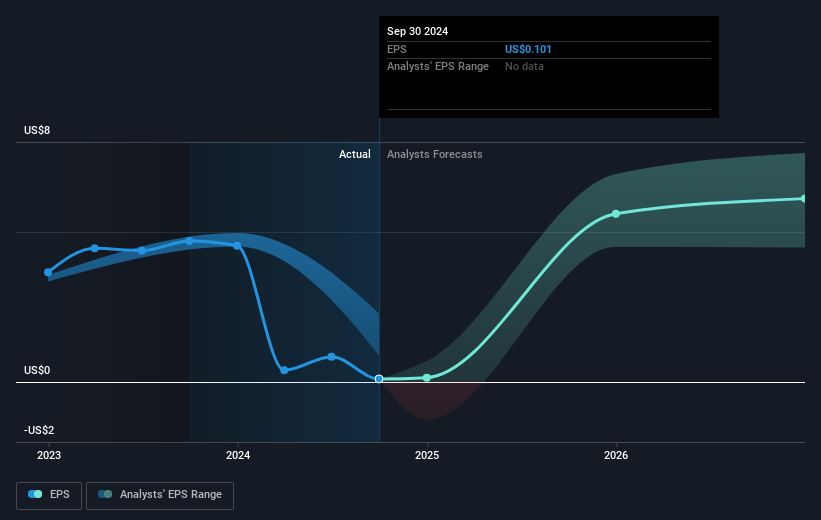

- The bearish analysts expect earnings to reach $7.6 billion (and earnings per share of $6.04) by about April 2028, up from $480.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 19.4x on those 2028 earnings, down from 272.4x today. This future PE is lower than the current PE for the US Biotechs industry at 20.2x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.72%, as per the Simply Wall St company report.

Gilead Sciences Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Gilead Sciences' HIV portfolio demonstrates consistent growth, with sales exceeding expectations and a strong pipeline for treatment and prevention options. This suggests sustained revenue growth as demand for their HIV treatments continues to climb.

- The company is expanding its liver disease portfolio with products like Livdelzi, which has shown strong initial sales and is anticipated to boost revenues as it gains market approval in more regions, positively impacting overall revenue.

- Gilead's oncology segment is progressing, particularly with Trodelvy showing promising results and being positioned for further market expansion, which could enhance sales revenues within its oncology division.

- Despite the Medicare Part D reform creating short-term headwinds for revenue growth in 2025, the company's strategic planning anticipates future growth with its long-acting HIV treatments, potentially leading to increased net revenues and overall earnings.

- Gilead has no major loss of exclusivity until late 2033, providing stability and the potential for sustained earnings and margin improvements, supported by a robust pipeline that is well-diversified across therapeutic areas.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Gilead Sciences is $97.3, which represents one standard deviation below the consensus price target of $112.5. This valuation is based on what can be assumed as the expectations of Gilead Sciences's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $140.0, and the most bearish reporting a price target of just $82.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $29.3 billion, earnings will come to $7.6 billion, and it would be trading on a PE ratio of 19.4x, assuming you use a discount rate of 6.7%.

- Given the current share price of $104.88, the bearish analyst price target of $97.3 is 7.8% lower. The relatively low difference between the current share price and the analyst bearish price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is an employee of Simply Wall St, but has written this narrative in their capacity as an individual investor. AnalystLowTarget holds no position in NasdaqGS:GILD. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. This narrative is general in nature and explores scenarios and estimates created by the author. The narrative does not reflect the opinions of Simply Wall St, and the views expressed are the opinion of the author alone, acting on their own behalf. These scenarios are not indicative of the company's future performance and are exploratory in the ideas they cover. The fair value estimate's are estimations only, and does not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that the author's analysis may not factor in the latest price-sensitive company announcements or qualitative material.