Key Takeaways

- Expansion of premium formats and new loyalty tiers could boost attendance, customer retention, and overall revenue.

- Innovative food, beverage offerings, and home popcorn sales are expected to enhance revenue streams and financial stability.

- Economic challenges, competition from streaming, heavy leverage, and reliance on blockbusters all present risks to AMC's revenues and growth potential.

Catalysts

About AMC Entertainment Holdings- Through its subsidiaries, engages in the theatrical exhibition business in the United States and Europe.

- AMC plans to expand its premium large-format offerings, such as IMAX with Laser and Dolby Cinema screens, which could improve attendance and admissions revenue.

- Introduction of new loyalty and subscription tiers, including Premiere GO! and AMC A-List Classic, is expected to boost customer retention and ticket sales, potentially increasing revenue.

- AMC is actively expanding its food and beverage offerings, including movie-themed drinks and collectibles, which is likely to increase food and beverage revenue and improve net margins.

- The company's foray into home popcorn sales, currently profitable and expanding to 11,000 stores, is anticipated to enhance ancillary revenue streams and overall earnings.

- AMC's financial strategy, including leveraging equity capital to strengthen the balance sheet and restructure debt, is likely to improve financial stability and enhance earnings potential as the industry recovers.

AMC Entertainment Holdings Future Earnings and Revenue Growth

Assumptions

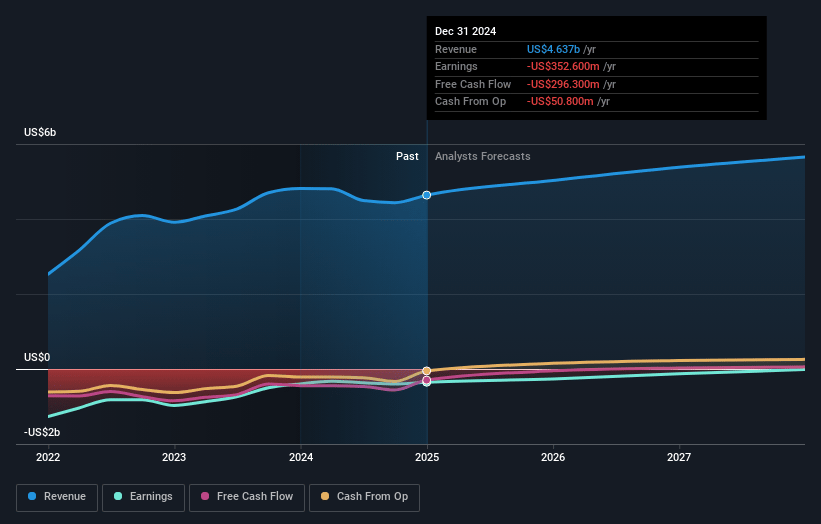

How have these above catalysts been quantified?- Analysts are assuming AMC Entertainment Holdings's revenue will grow by 8.0% annually over the next 3 years.

- Analysts are not forecasting that AMC Entertainment Holdings will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate AMC Entertainment Holdings's profit margin will increase from -8.6% to the average US Entertainment industry of 9.2% in 3 years.

- If AMC Entertainment Holdings's profit margin were to converge on the industry average, you could expect earnings to reach $528.8 million (and earnings per share of $1.0) by about July 2028, up from $-391.2 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 4.5x on those 2028 earnings, up from -3.9x today. This future PE is lower than the current PE for the US Entertainment industry at 26.9x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 11.6%, as per the Simply Wall St company report.

AMC Entertainment Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Risks such as economic downturns, inflation, or changes in consumer spending habits could reduce discretionary income, potentially impacting AMC's attendance and thus its revenues and profitability.

- The ongoing competition from streaming platforms, which offer consumers convenient alternatives to theatrical releases, may continue to pressure AMC's attendance figures and revenues.

- Despite efforts to improve the balance sheet, AMC remains highly leveraged, and limitations on access to growth capital could restrict its ability to make necessary investments, impacting both revenue growth and net margins.

- AMC's reliance on a steady pipeline of blockbuster movies for driving attendance poses a risk since any disruption to film production or poor performance of anticipated hits could adversely affect revenues.

- The successful implementation of initiatives, such as the AMC Go Plan, increased theater upgrades, and expanded loyalty programs, may face execution challenges that could impact expected financial improvements and overall earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $3.22 for AMC Entertainment Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $4.0, and the most bearish reporting a price target of just $2.6.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $5.7 billion, earnings will come to $528.8 million, and it would be trading on a PE ratio of 4.5x, assuming you use a discount rate of 11.6%.

- Given the current share price of $3.5, the analyst price target of $3.22 is 8.7% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.