Key Takeaways

- Increased capital spending for network expansion and rural initiatives is expected to pressure cash flow and net margins due to high costs and slow revenue recovery.

- Operational disruptions and strategic challenges like paused buybacks and reduced political advertising revenue pose risks to revenue and earnings per share growth.

- Charter Communications' multiyear investment and strategic initiatives are driving rapid growth in mobile services and improving long-term earnings and cash flow potential.

Catalysts

About Charter Communications- Operates as a broadband connectivity and cable operator company serving residential and commercial customers in the United States.

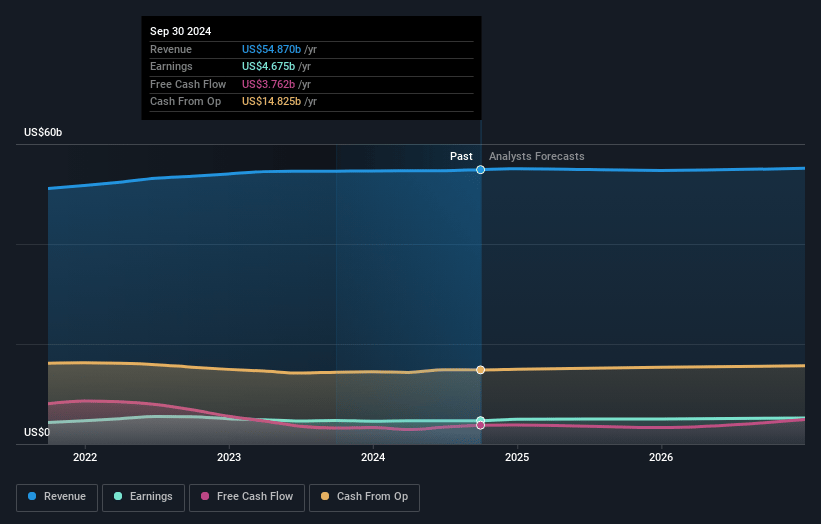

- Charter Communications anticipates higher capital expenditure in 2025 compared to 2024, with total spending expected to reach approximately $12 billion. This peak in capital investment, driven by network evolution and rural expansion, is likely to put temporary pressure on free cash flow growth in the near term.

- The company's participation in subsidized rural initiatives and network expansion is expected to increase line extension costs, which may affect net margins as these costs may not be immediately offset by revenue given the slower penetration in rural markets.

- Recent natural disasters, such as hurricanes and wildfires, have resulted in significant unexpected expenses, reducing EBITDA by $35 million and leading to over $125 million in capital expenditures. These events have also caused operational disruptions, affecting subscriber growth prospects and potentially delaying revenue realization.

- Charter's decision to pause its buyback program due to the pending Liberty Broadband transaction and potential economic conditions might lead to lower earnings per share growth, given that buybacks would normally help support EPS by reducing the share count.

- The ongoing challenges in political advertising revenue and the impact of the Affordable Connectivity Program's end have created headwinds that could result in slower-than-expected revenue growth, counteracting some of the benefits from mobile and video bundling strategies.

Charter Communications Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Charter Communications compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Charter Communications's revenue will decrease by 0.0% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 9.2% today to 7.5% in 3 years time.

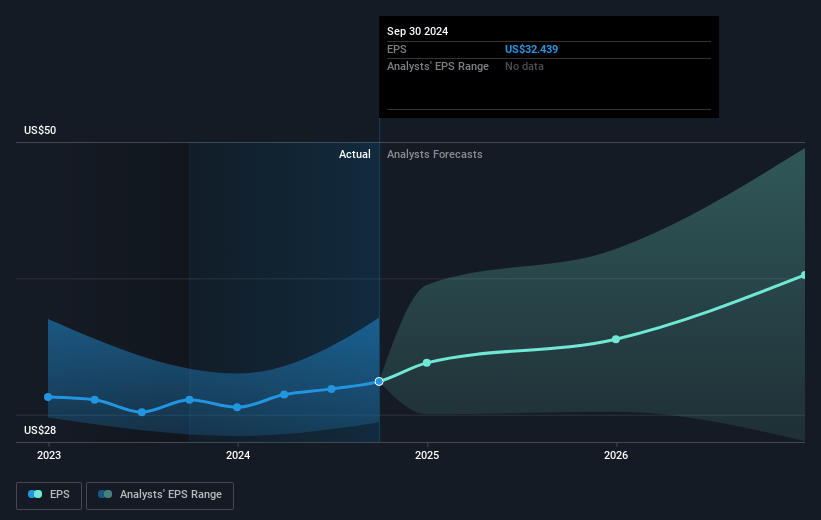

- The bearish analysts expect earnings to reach $4.1 billion (and earnings per share of $33.98) by about April 2028, down from $5.1 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 15.9x on those 2028 earnings, up from 9.3x today. This future PE is greater than the current PE for the US Media industry at 13.8x.

- Analysts expect the number of shares outstanding to decline by 1.45% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.01%, as per the Simply Wall St company report.

Charter Communications Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Charter Communications' Spectrum Mobile business is rapidly growing, making it the fastest-growing mobile provider in the U.S., which contributes to an increase in company revenue.

- The company's multiyear investment initiatives, including network evolution and expansion, are expected to provide tangible results that could enhance earnings.

- Charter's strategic initiatives launched in late 2022 are likely to improve its growth potential in the long term, potentially leading to increased free cash flow growth.

- The company has managed cost efficiency initiatives effectively, which helps maintain strong EBITDA growth, contributing positively to their net margins.

- Charter's commitment to improving customer service and satisfaction could result in lower churn rates, which supports steady revenue growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Charter Communications is $334.81, which represents one standard deviation below the consensus price target of $401.4. This valuation is based on what can be assumed as the expectations of Charter Communications's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $525.0, and the most bearish reporting a price target of just $273.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $55.0 billion, earnings will come to $4.1 billion, and it would be trading on a PE ratio of 15.9x, assuming you use a discount rate of 9.0%.

- Given the current share price of $334.38, the bearish analyst price target of $334.81 is 0.1% higher. The relatively low difference between the current share price and the analyst bearish price target indicates that the bearish analysts believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is an employee of Simply Wall St, but has written this narrative in their capacity as an individual investor. AnalystLowTarget holds no position in NasdaqGS:CHTR. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. This narrative is general in nature and explores scenarios and estimates created by the author. The narrative does not reflect the opinions of Simply Wall St, and the views expressed are the opinion of the author alone, acting on their own behalf. These scenarios are not indicative of the company's future performance and are exploratory in the ideas they cover. The fair value estimate's are estimations only, and does not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that the author's analysis may not factor in the latest price-sensitive company announcements or qualitative material.