Key Takeaways

- Strategic partnerships and content bundling are expected to drive streaming and subscription revenue growth, offsetting linear declines.

- Expansion of addressable advertising and new initiatives could enhance ad efficiency, boosting digital ad revenue while mitigating traditional advertising declines.

- Decreasing linear subscribers and ad revenue, reliance on volatile licensing, and international distribution issues risk AMC's overall revenue and earnings stability.

Catalysts

About AMC Networks- An entertainment company, distributes contents in the United States, Europe, and internationally.

- Strategic partnerships with major streaming platforms like Netflix and content bundling deals with providers such as Verizon and Vizio are expected to drive higher streaming revenue growth, offsetting linear declines. This positions AMC Networks to potentially increase their subscription revenue in the low to mid-teens percent range for 2025.

- The expansion of addressable and programmatic advertising through their Audience+ platform, along with the introduction of AMCN Outcomes for real-time insights, could enhance advertising efficiency and stimulate digital ad revenue growth. This could help mitigate declines in traditional linear advertising and improve overall advertising revenue.

- The return of U.S. streaming rights for The Walking Dead series and continued strong interest in AMC's popular franchises are likely to boost viewership and streaming subscriptions, potentially leading to increased streaming revenue.

- The planned launch of an ad-supported version of the Shudder streaming service later in the year is expected to widen audience reach and diversify revenue streams, contributing further to digital ad revenue.

- AMC Networks' disciplined content licensing strategy, focusing on leveraging world-class IP, is anticipated to continue driving licensing revenue growth with forecasted revenue of approximately $250 million for 2025. The strategic licensing of previous seasons to platforms like Netflix ensures wider exposure and can drive back-demand for current content.

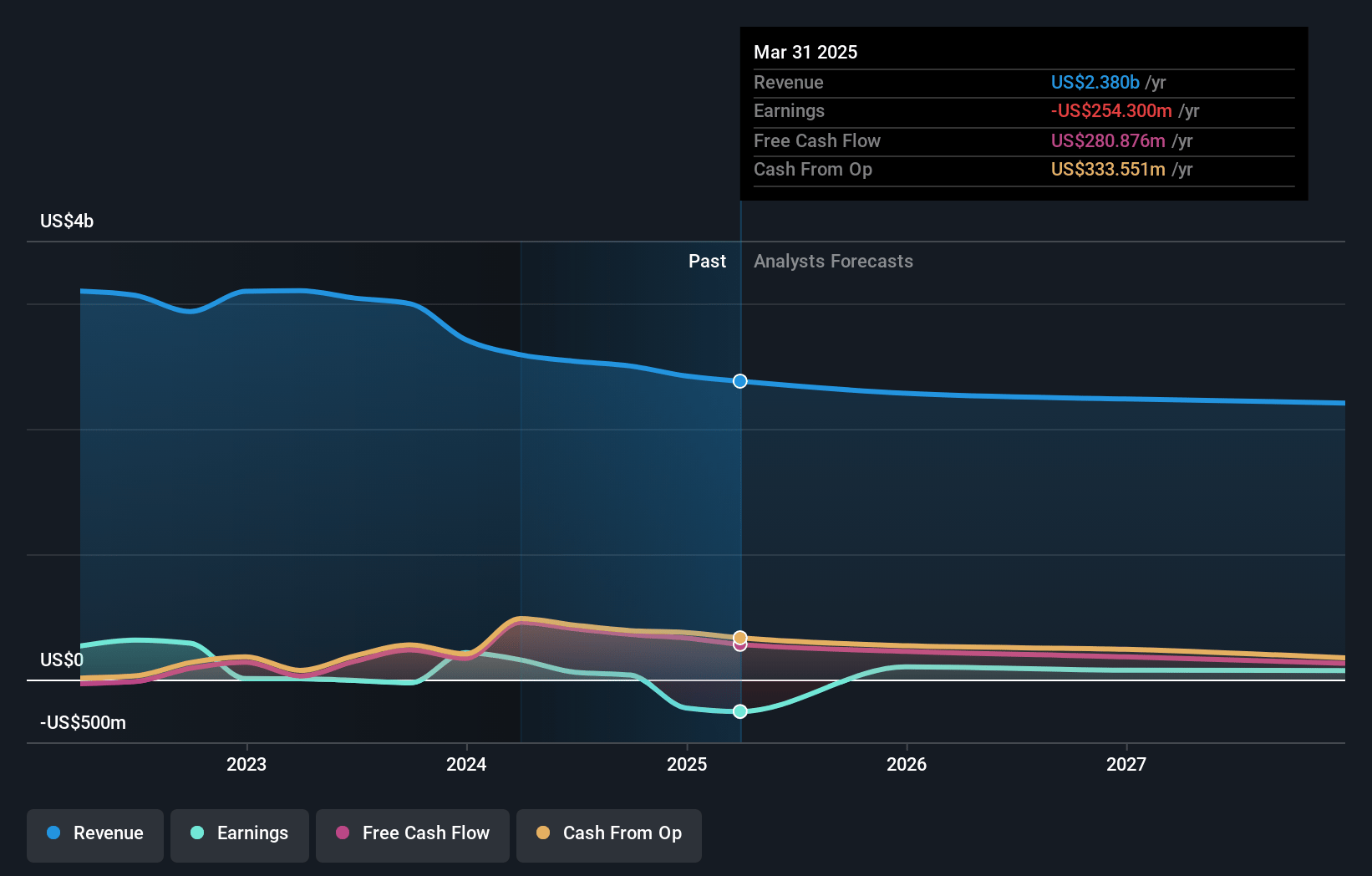

AMC Networks Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming AMC Networks's revenue will decrease by 2.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from -9.4% today to 4.2% in 3 years time.

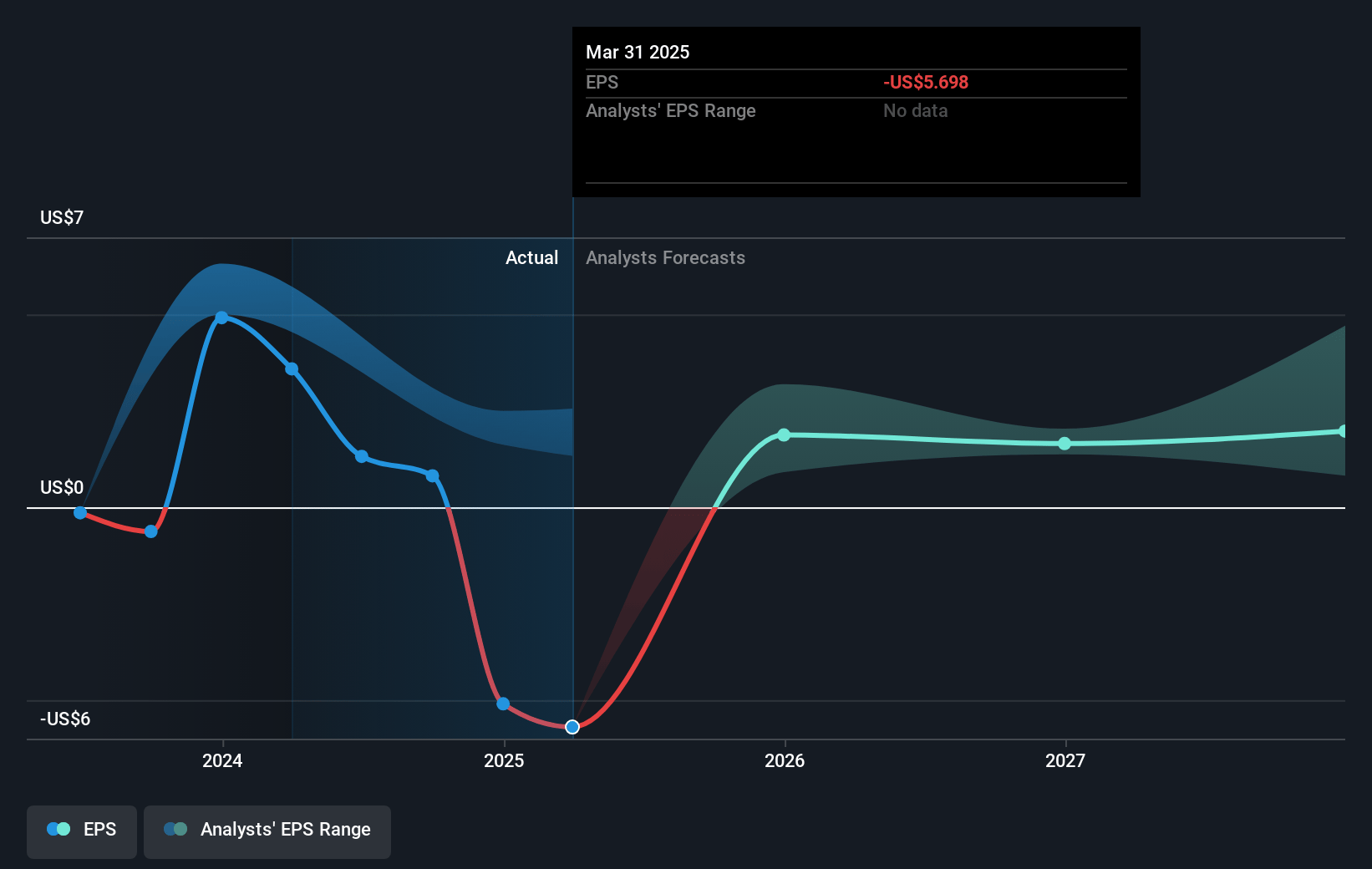

- Analysts expect earnings to reach $94.6 million (and earnings per share of $2.23) by about April 2028, up from $-226.5 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $126.0 million in earnings, and the most bearish expecting $66.3 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 5.3x on those 2028 earnings, up from -1.2x today. This future PE is lower than the current PE for the US Media industry at 13.6x.

- Analysts expect the number of shares outstanding to grow by 0.21% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 11.41%, as per the Simply Wall St company report.

AMC Networks Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Linear subscriber declines remain a significant concern, as they contribute to a decrease in affiliate revenue and negatively impact subscription revenue growth. This trend poses a risk to AMC Networks' overall revenue.

- The challenging linear ad market, alongside lower linear ratings, has resulted in a decline in advertising revenue. This presents risks to both total revenue and net margins, considering the increasing reliance on digital advertising growth.

- The company's heavy reliance on licensing revenue can be risky due to its potentially volatile nature and dependency on deal timing, which could lead to inconsistent earnings and cash flow.

- International subscription revenue declines, particularly due to non-renewal of distribution agreements, highlight vulnerability in international revenue streams and could impact overall revenue growth.

- Continual restructuring charges and impairment costs are causing operating losses, which can adversely affect net margins and earnings stability in the long run.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $8.286 for AMC Networks based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $15.0, and the most bearish reporting a price target of just $4.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $2.2 billion, earnings will come to $94.6 million, and it would be trading on a PE ratio of 5.3x, assuming you use a discount rate of 11.4%.

- Given the current share price of $6.27, the analyst price target of $8.29 is 24.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.