Key Takeaways

- Relocating manufacturing to Panama and expanding Illinois capacity are strategic moves to reduce costs and increase production, boosting revenue and market share.

- Diversification with new food-grade and pharmaceutical ventures may drive future revenue, contingent upon successful operationalization and partnerships.

- Significant CapEx and reliance on tariff rebates introduce financial risks, while execution challenges and market fluctuations threaten revenue and profitability.

Catalysts

About Flexible Solutions International- Develops, manufactures, and markets specialty chemicals that slow the evaporation of water in Canada, the United States, and internationally.

- The new food-grade product contract, once operationalized with new clean rooms and equipment, is expected to significantly increase revenue by up to $30 million per year starting as early as Q4 2025, impacting overall revenue growth positively.

- Relocating manufacturing to Panama will reduce production costs and tariffs for international sales, improving net margins and boosting cash flow by eliminating lengthy rebate processes.

- Additional capacity in Illinois will allow for increased production of food-grade products, potentially increasing revenues and expanding market share in the food and nutrition space.

- The resumption of growth for the Florida LLC in 2025 is expected to lead to increased revenue streams as sales and profit-sharing from this asset improves over the payout period.

- The investment and planned entry into the pharmaceutical industry, with the acquisition of a GLP-1 drug production line, could unlock new revenue streams if advanced orders and partnership arrangements can be secured.

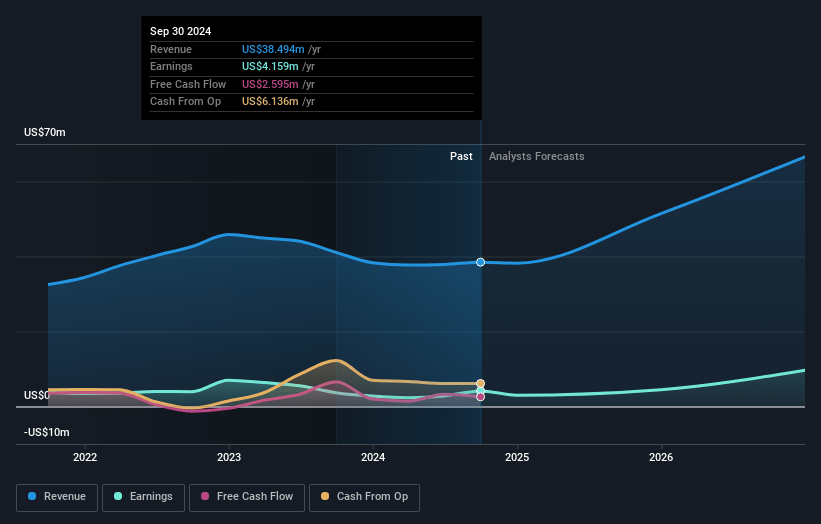

Flexible Solutions International Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Flexible Solutions International's revenue will grow by 29.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.9% today to 18.6% in 3 years time.

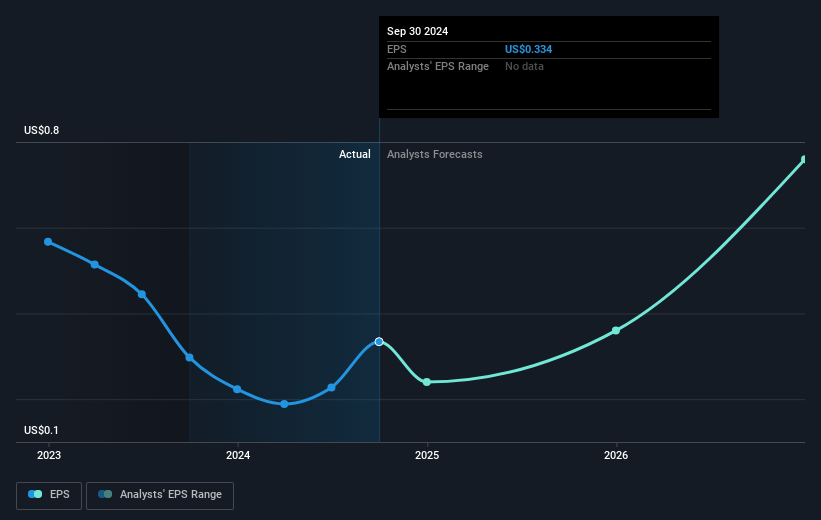

- Analysts expect earnings to reach $15.6 million (and earnings per share of $1.21) by about April 2028, up from $3.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 9.2x on those 2028 earnings, down from 16.0x today. This future PE is lower than the current PE for the US Chemicals industry at 17.7x.

- Analysts expect the number of shares outstanding to grow by 1.58% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.12%, as per the Simply Wall St company report.

Flexible Solutions International Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The need for significant capital expenditure (CapEx) to achieve production goals for the new food-grade contract introduces financial risk. If these new products do not meet customer expectations or do not generate the expected revenue, it could strain cash flow and hurt net margins.

- The company's reliance on pending tariff rebates from the U.S. government involves uncertainty. Delays or failures in obtaining these rebates can negatively impact cash flow and profits.

- The transition of production operations to Panama to avoid U.S. tariffs comes with execution risks. Any delays or issues with the new facility could affect revenue and increase operational costs.

- The potential revenue from the new food-grade contract is contingent on several factors being successfully executed, such as building clean rooms, installing specialized equipment, and satisfying customer price expectations. Any failure in achieving these could delay revenue realization or affect earnings.

- Commodity price fluctuation, coupled with the conflict between rising crop costs and low crop prices, might affect the agricultural sector's profitability, thereby impacting demand for Flexible Solutions International's products and affecting revenue.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $9.0 for Flexible Solutions International based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $83.7 million, earnings will come to $15.6 million, and it would be trading on a PE ratio of 9.2x, assuming you use a discount rate of 7.1%.

- Given the current share price of $3.84, the analyst price target of $9.0 is 57.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.