Key Takeaways

- Significant production increases in copper and zinc, driven by facility improvements, are expected to boost revenues and improve earnings.

- Extensive capital investment in projects aims to drive long-term growth, while operational cost reductions enhance competitiveness and net margins.

- Ongoing regional protests, water issues, surplus copper, and regulatory changes could raise costs, delay projects, and lower Southern Copper's margins and revenues.

Catalysts

About Southern Copper- Engages in mining, exploring, smelting, and refining copper and other minerals in Peru, Mexico, Argentina, Ecuador, and Chile.

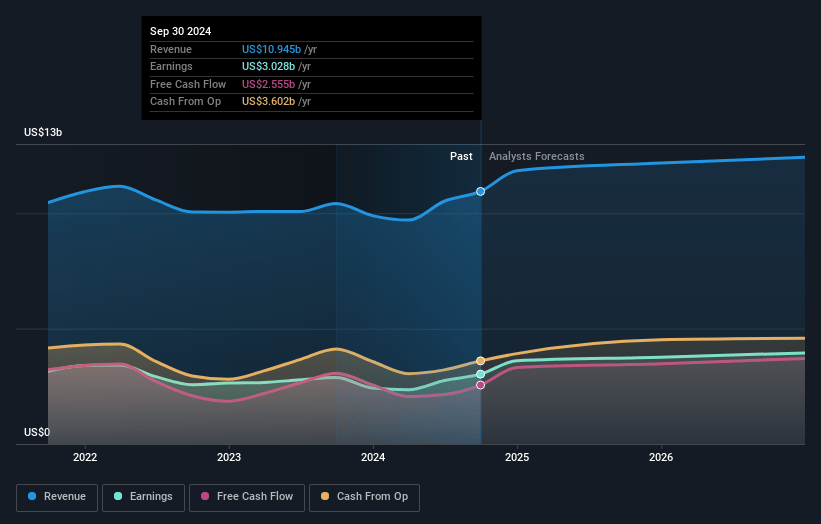

- Southern Copper anticipates increased copper production in 2024 by 7% over 2023, driven by recovery at the SX-EW facilities at Buenavista and enhanced production capacity at the Buenavista Zinc concentrator, likely leading to higher future revenues.

- The company expects an 84% increase in zinc production in 2024 due to the ramp-up of the Buenavista Zinc concentrator, which is already operating at full capacity. This substantial production increase is projected to boost sales and improve earnings.

- Southern Copper's significant capital investment program, exceeding $15 billion, includes projects like Tia Maria and Buenavista Zinc, which are poised to drive long-term growth and generate substantial returns by enhancing production capacity, positively impacting future revenue and earnings.

- A focus on operational improvements, such as reducing the operating cash cost per pound of copper to $1.95, positions the company to enhance net margins through strict cost control measures while maintaining competitiveness in the market.

- Higher anticipated production of silver and zinc for 2025, with forecasts of 22.9 million ounces and over 154,000 tons respectively, is expected to increase revenue and earnings, especially as these by-products see favorable price dynamics.

Southern Copper Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on Southern Copper compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Southern Copper's revenue will grow by 6.0% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 29.5% today to 36.0% in 3 years time.

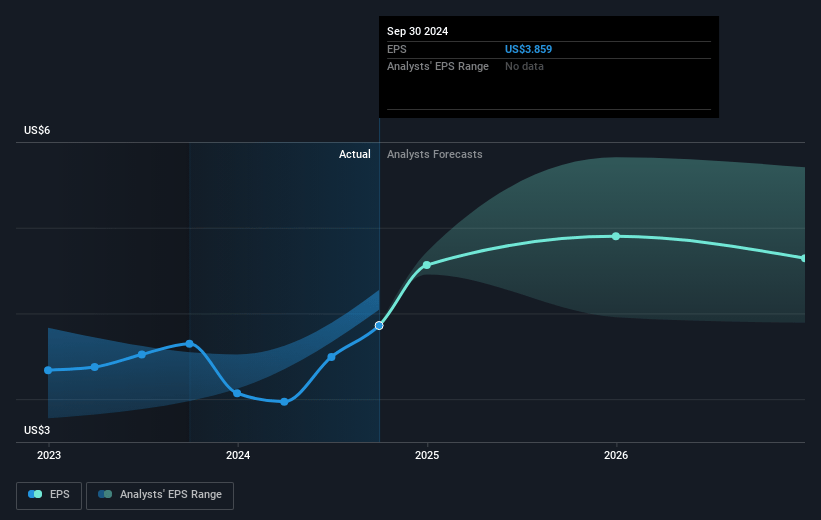

- The bullish analysts expect earnings to reach $4.9 billion (and earnings per share of $6.33) by about April 2028, up from $3.4 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 23.0x on those 2028 earnings, up from 20.5x today. This future PE is greater than the current PE for the US Metals and Mining industry at 21.5x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.44%, as per the Simply Wall St company report.

Southern Copper Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Ongoing protests and community opposition, particularly around the Tia Maria project in Peru, could lead to delays and increase project costs, ultimately impacting future revenues and net margins.

- Concerns around water availability at mining sites, such as the Buenavista mine in Mexico, could lead to increased operational costs if alternative water sources need to be secured, impacting net margins.

- The slight market surplus of copper expected for 2024, along with weak demand from key consumers such as China, may put downward pressure on copper prices, affecting revenues and earnings.

- Regulatory uncertainties in Mexico and Peru, such as changes in concession regimes or environmental regulations, could lead to higher compliance costs or project delays, impacting net margins and revenues.

- Changes in by-product prices, particularly a decrease in molybdenum prices, may reduce the benefit from by-product credits, resulting in increased cash costs per pound of copper and lower net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for Southern Copper is $113.82, which represents one standard deviation above the consensus price target of $93.83. This valuation is based on what can be assumed as the expectations of Southern Copper's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $130.0, and the most bearish reporting a price target of just $67.97.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be $13.6 billion, earnings will come to $4.9 billion, and it would be trading on a PE ratio of 23.0x, assuming you use a discount rate of 7.4%.

- Given the current share price of $86.83, the bullish analyst price target of $113.82 is 23.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is an employee of Simply Wall St, but has written this narrative in their capacity as an individual investor. AnalystHighTarget holds no position in NYSE:SCCO. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. This narrative is general in nature and explores scenarios and estimates created by the author. The narrative does not reflect the opinions of Simply Wall St, and the views expressed are the opinion of the author alone, acting on their own behalf. These scenarios are not indicative of the company's future performance and are exploratory in the ideas they cover. The fair value estimate's are estimations only, and does not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that the author's analysis may not factor in the latest price-sensitive company announcements or qualitative material.