Key Takeaways

- Strategic shift to a trader distributor model enhances revenue stability by capturing favorable pricing and managing market seasonality.

- Long-term growth is driven by expansion efforts and sustainable practices, including lithium sulfate production, boosting revenue potential and market differentiation.

- Operational and financial challenges, including loan delays, cost management, and market strategy shifts, could threaten Sigma Lithium’s growth, profitability, and market stability.

Catalysts

About Sigma Lithium- Engages in the exploration and development of lithium deposits in Brazil.

- The ongoing optimization of Plant 1 is expected to increase production by 10% to 15%, which will potentially improve revenue and net margins by reducing costs and increasing output without major capital expenditure.

- The construction of Plant 2, funded in large part by a $487 million BNDES development loan with favorable terms, is expected to significantly expand production capacity, thus boosting future revenues.

- The strategic shift in commercial strategy to a trader distributor model allows the company to capture more favorable pricing and navigate market seasonality, enhancing revenue stability and growth.

- The ability to increase global recoveries and reprocess tailings indicates improvements in efficiency and output, which should support better net margins through optimal resource utilization.

- The development of Phase 3 and integration of lithium sulfate production by 2027 represent long-term growth drivers that will further scale up operations and increase revenue potential while leveraging traceable and sustainable practices for market differentiation.

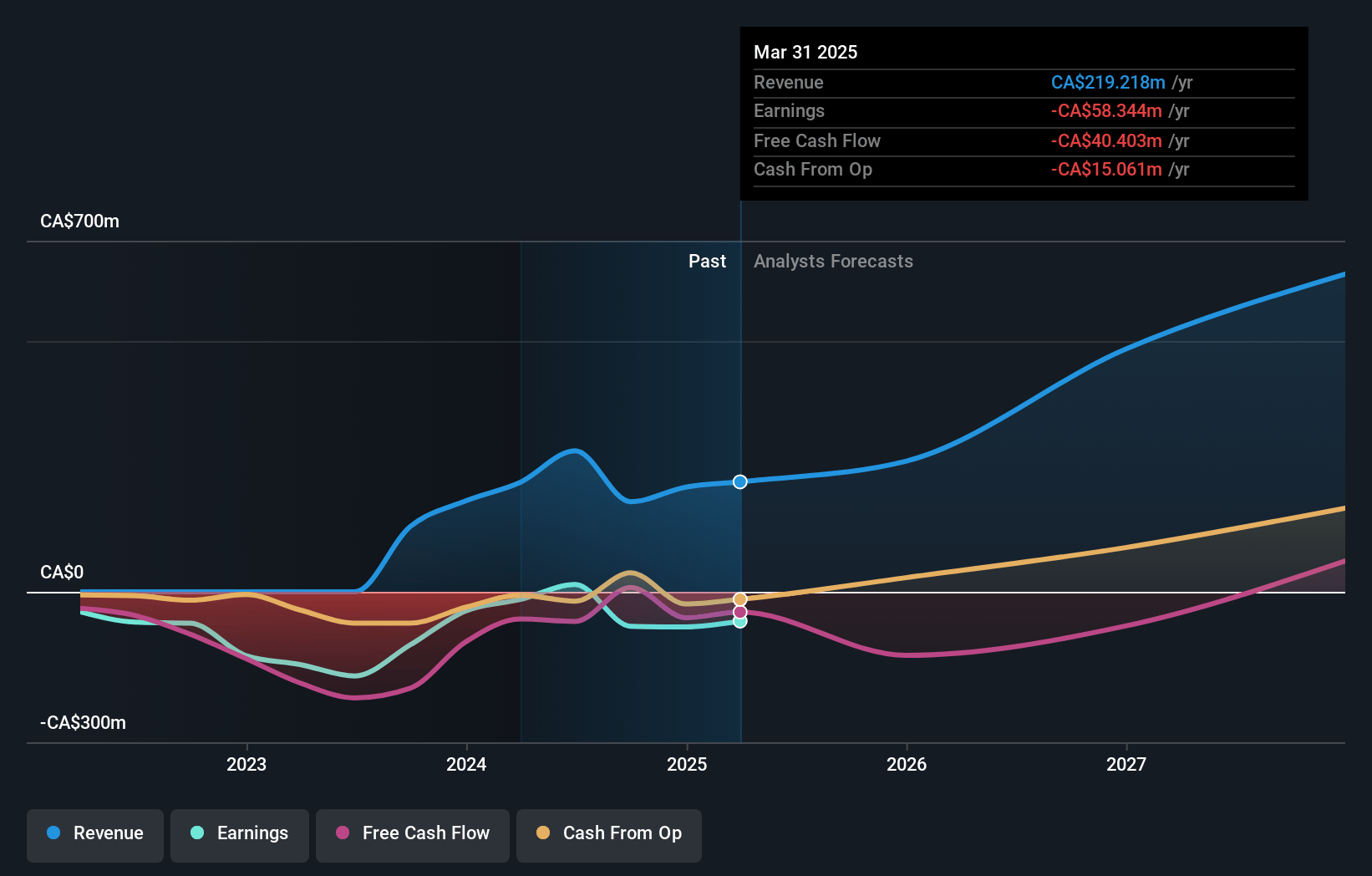

Sigma Lithium Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Sigma Lithium's revenue will grow by 76.3% annually over the next 3 years.

- Analysts are not forecasting that Sigma Lithium will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Sigma Lithium's profit margin will increase from -36.8% to the average US Metals and Mining industry of 8.6% in 3 years.

- If Sigma Lithium's profit margin were to converge on the industry average, you could expect earnings to reach CA$91.2 million (and earnings per share of CA$0.79) by about March 2028, up from CA$-71.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 42.3x on those 2028 earnings, up from -27.3x today. This future PE is greater than the current PE for the US Metals and Mining industry at 23.9x.

- Analysts expect the number of shares outstanding to grow by 1.16% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 11.32%, as per the Simply Wall St company report.

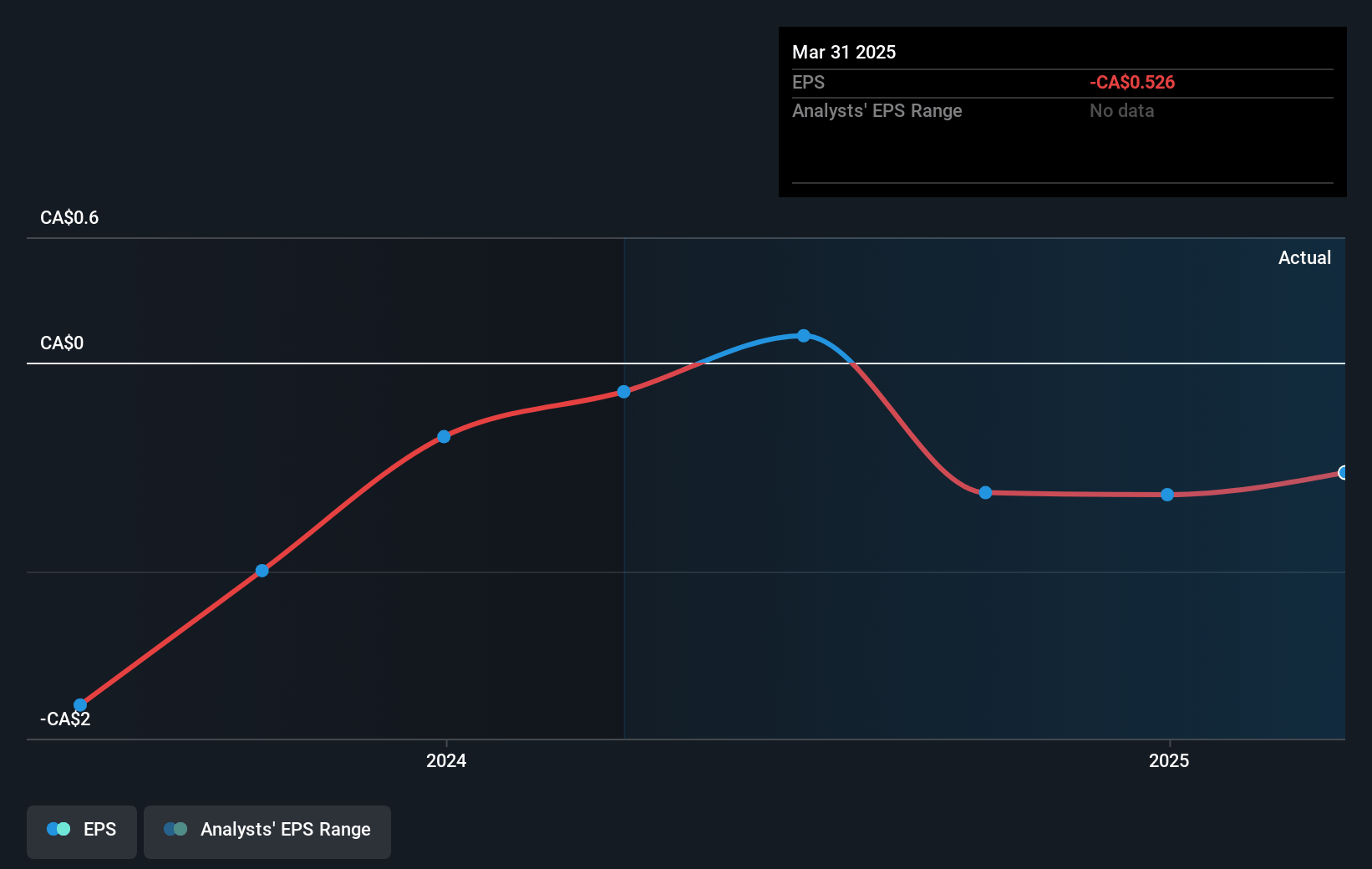

Sigma Lithium Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Potential delays in BNDES loan disbursements and changes in trade credit facilities could impact the company’s ability to fund construction projects on time, affecting future revenue growth.

- Timbered production guidance and operational issues related to crushers and recovery rates could lead to higher operational costs and lower-than-expected production volumes, impacting earnings.

- Shifting commercial strategies away from traders as principals may expose Sigma to increased market volatility and pricing risks, which could potentially reduce net margins if not managed well.

- Increased expenses related to plant optimizations and the ongoing construction of Phase 2, if not properly controlled, might strain cash flows and affect the company’s ability to maintain its low-cost position, impacting overall profitability.

- Dependencies on maintaining a strong ESG reputation amidst growing scrutiny over supply chain traceability could lead to increased compliance costs and affect market access, impacting future revenue streams.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $17.0 for Sigma Lithium based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be CA$1.1 billion, earnings will come to CA$91.2 million, and it would be trading on a PE ratio of 42.3x, assuming you use a discount rate of 11.3%.

- Given the current share price of $12.21, the analyst price target of $17.0 is 28.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.