Narratives are currently in beta

Key Takeaways

- Expansion in 1,4-Dioxane and sulfate-free technologies and a cleaner fuel pipeline aligns with growth, driving future revenue across multiple segments.

- Strategic focus outside Latin America aims to boost growth, supported by strong finances enabling investments and potential M&A opportunities.

- Challenges with recent acquisitions, tax rate increases, and declining Oilfield Services revenue threaten Innospec's net margins and overall financial performance.

Catalysts

About Innospec- Develops, manufactures, blends, markets, and supplies specialty chemicals in the United States, rest of North America, the United Kingdom, rest of Europe, and internationally.

- Innospec continues to expand its industry-leading portfolio of 1,4-Dioxane and sulfate-free technologies, which is expected to drive growth in the personal care market and other diverse end markets such as home care and agriculture. This would positively impact future revenue and earnings.

- The company has a robust technology pipeline focused on cleaner and renewable fuels, which aligns with long-term trends in heavy transportation fuels and lower emissions, potentially driving sustained revenue growth and improved net margins in the Fuel Specialties segment.

- Innospec's strategy to focus on growth and margin improvement opportunities in its Oilfield Services segment outside Latin America, particularly in regions like the Middle East, could lead to sequential quarterly growth in 2025, enhancing future revenue and operating income.

- Performance Chemicals segment is experiencing growth due to a mix of acquisition growth and volume increases, despite an adverse price mix. This segment is expected to maintain stable operating profits, contributing positively to net margins and earnings stability.

- The company’s strong balance sheet, with over $300 million in cash and no debt, positions it well to continue organic investments and complementary M&A, which are expected to support long-term revenue growth and dividend returns to shareholders.

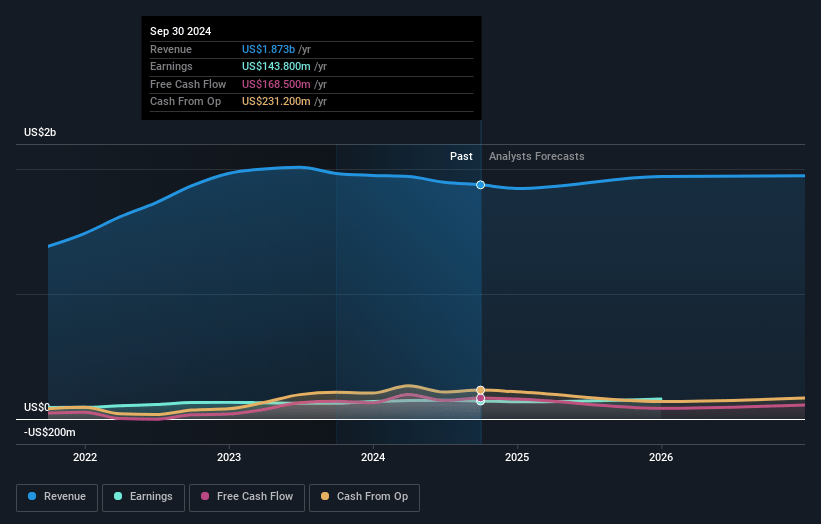

Innospec Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Innospec's revenue will grow by 1.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.9% today to 8.2% in 3 years time.

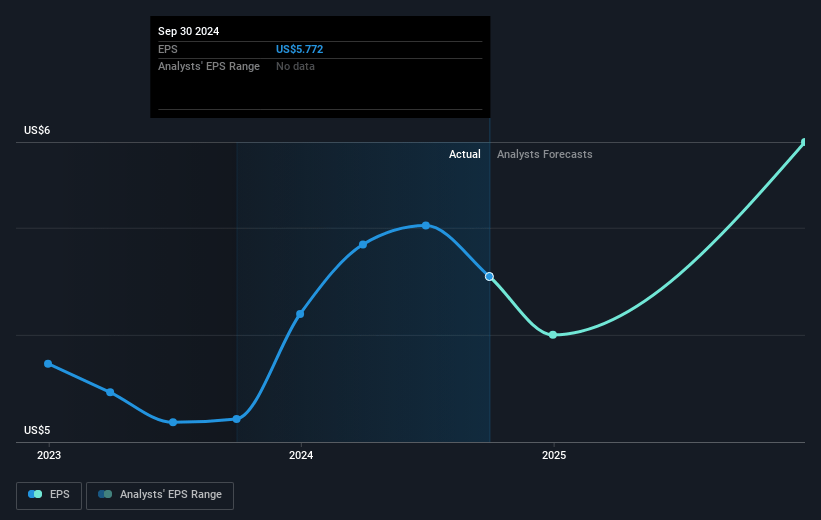

- Analysts expect earnings to reach $161.7 million (and earnings per share of $6.66) by about November 2027, up from $149.6 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 23.0x on those 2027 earnings, up from 18.5x today. This future PE is lower than the current PE for the US Chemicals industry at 25.5x.

- Analysts expect the number of shares outstanding to decline by 0.92% per year for the next 3 years.

- To value all of this in today's dollars, we will use a discount rate of 6.4%, as per the Simply Wall St company report.

Innospec Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Oilfield Services revenue has decreased by 24%, with a continued expectation of lower activity levels in Latin America into 2025, potentially impacting overall revenue and earnings.

- Despite efforts to improve margins, high dependence on Fuel Specialties and Performance Chemicals puts pressure on maintaining favorable sales mix and raw material pricing, affecting net margins.

- The effective tax rate increased significantly to 25.4% from 17.5% last year, and is projected to rise further to 27% in 2025, potentially impacting net income.

- Corporate costs have been volatile, with a one-off credit affecting current quarter costs; this volatility could impact net margins if not controlled in future quarters.

- The company faces challenges integrating recent acquisitions, and potential setbacks could affect revenue and operating income if synergy benefits are not fully realized.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $128.5 for Innospec based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $2.0 billion, earnings will come to $161.7 million, and it would be trading on a PE ratio of 23.0x, assuming you use a discount rate of 6.4%.

- Given the current share price of $111.13, the analyst's price target of $128.5 is 13.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives