Key Takeaways

- Tech-driven product launches and market expansion promise robust revenue growth by tapping into underserved segments and boosting membership.

- Strategic use of AI promises operational cost reductions and fixed cost efficiencies, aligning with the goal of reaching profitability soon.

- Oscar Health's reliance on Medicaid redeterminations and SEP memberships affects revenue stability, with increased MLR and government subsidy changes posing risks to margins and growth.

Catalysts

About Oscar Health- Operates as a health insurance in the United States.

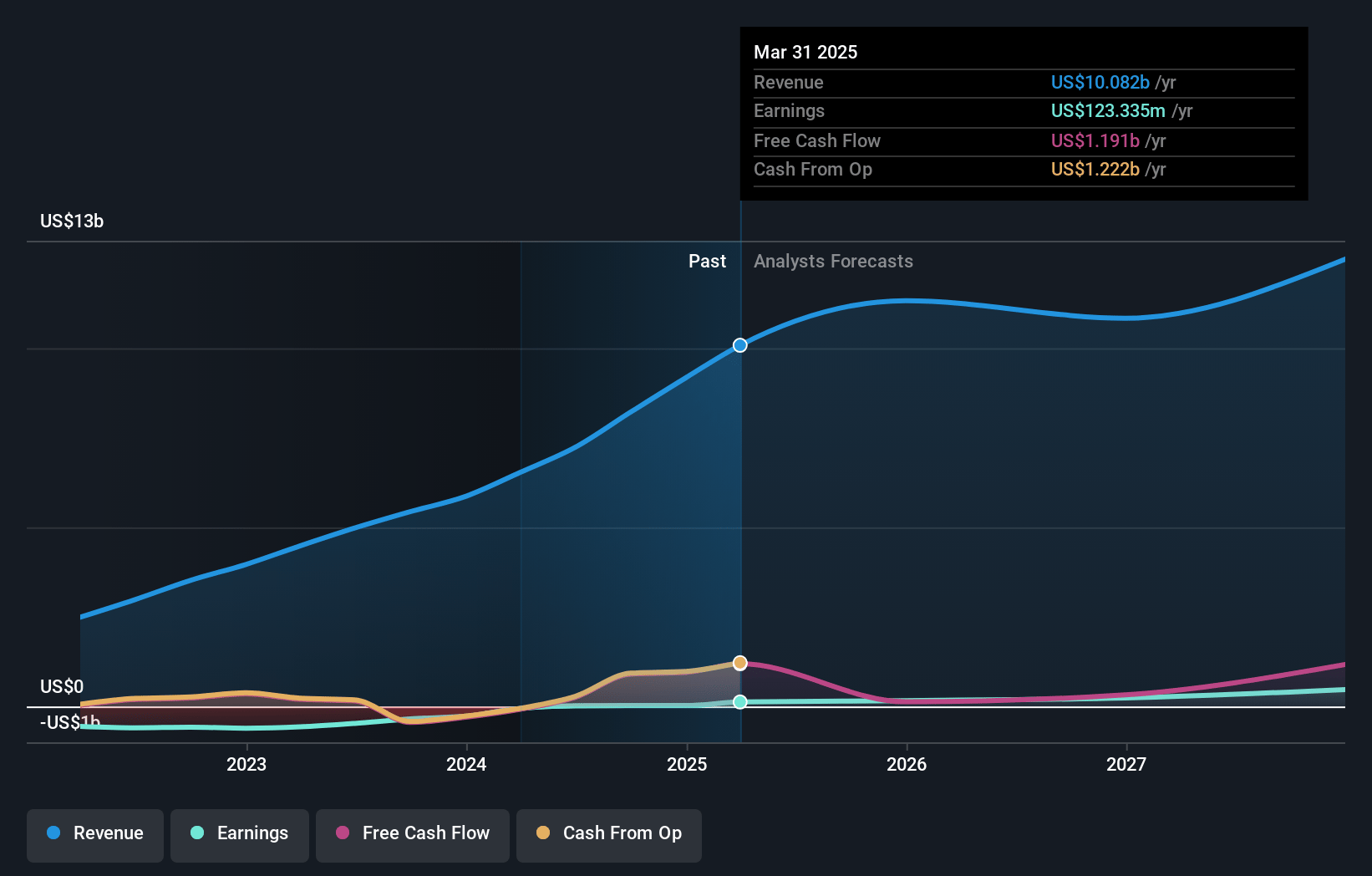

- Oscar Health's 68% year-over-year revenue increase to $2.4 billion and a projected 20% revenue CAGR through 2027 highlight expectations for continued strong top-line growth. This growth is driven by increased membership, new product offerings, and market expansion. (Revenue)

- The company is implementing AI tools to enhance operational efficiency and reduce fraud, waste, and abuse, which is expected to drive down operational costs and enhance net margins. (Net Margins)

- Oscar's rollout of new, tech-focused insurance products, such as a multi-condition plan and a Spanish-first solution, targets underserved segments, potentially boosting membership and revenue. (Revenue)

- With Oscar's recent expansion to new markets, increasing its total addressable lives by 700,000 to approximately 11 million, the company is positioning itself for significant membership growth. This expansion supports future revenue growth. (Revenue)

- A focus on leveraging fixed cost efficiencies and reducing SG&A expense ratios through technology and AI applications is anticipated to lead to improved earnings and profitability, aligning with the company's target of achieving profitability in 2024. (Earnings)

Oscar Health Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Oscar Health's revenue will grow by 18.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 0.4% today to 3.0% in 3 years time.

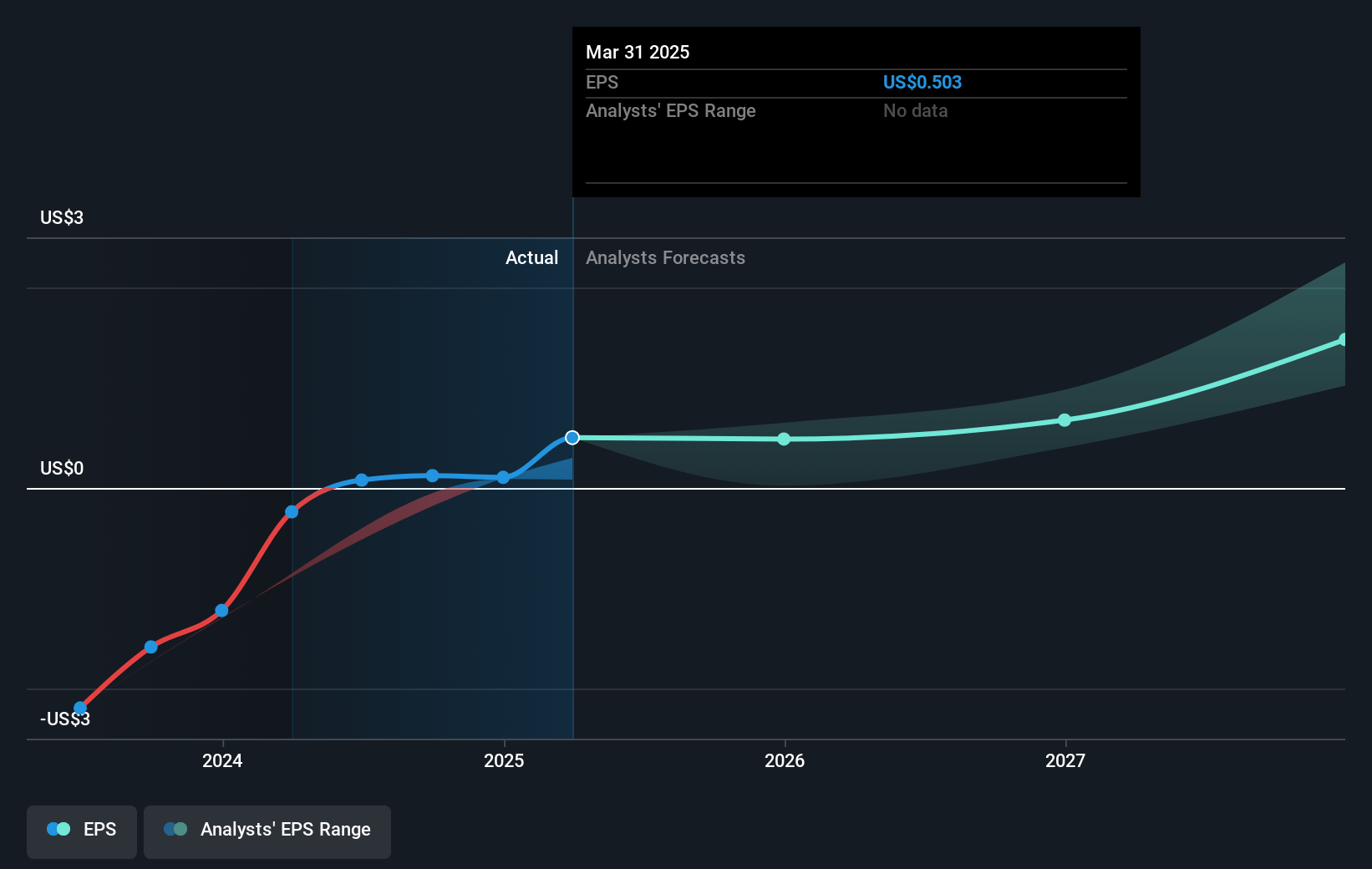

- Analysts expect earnings to reach $410.4 million (and earnings per share of $1.25) by about January 2028, up from $28.9 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $508.8 million in earnings, and the most bearish expecting $59.7 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 18.4x on those 2028 earnings, down from 138.9x today. This future PE is greater than the current PE for the US Insurance industry at 12.8x.

- Analysts expect the number of shares outstanding to grow by 9.94% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.05%, as per the Simply Wall St company report.

Oscar Health Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Oscar Health's medical loss ratio increased by 80 basis points, mainly due to higher SEP membership and a late summer COVID uptick, which could suggest higher medical costs and pressure on net margins.

- The company's reliance on Medicaid redeterminations for growth creates dependency on a potentially unpredictable factor, which may impact revenue stability and growth.

- SEP memberships, though anticipated to be a tailwind in future years, currently lead to a higher MLR and added pressure on in-year financials, affecting earnings in the short term.

- Changes in government subsidies for ACA plans pose a risk to long-term revenue assumptions, potentially affecting both revenue and margins if not renewed or modified unfavorably.

- Competitive pressures, including potential price undercutting by market players, could affect Oscar Health's ability to execute its pricing strategy effectively, impacting revenue growth and profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $19.36 for Oscar Health based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $28.0, and the most bearish reporting a price target of just $12.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $13.5 billion, earnings will come to $410.4 million, and it would be trading on a PE ratio of 18.4x, assuming you use a discount rate of 6.0%.

- Given the current share price of $16.28, the analyst's price target of $19.36 is 15.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives