Last Update08 Oct 25Fair value Decreased 1.68%

Analysts have modestly trimmed their price target for Marsh & McLennan Companies from $232.42 to $228.53. They cited persistent growth headwinds in commercial property pricing and continued sector-wide margin pressures.

Analyst Commentary

Recent research notes on Marsh & McLennan Companies reflect a dynamic insurance sector environment, with both supportive and cautionary observations from industry analysts. The commentary covers a range of factors impacting valuation and growth prospects for the company.

Bullish Takeaways- Bullish analysts see insurance brokers like Marsh & McLennan as being less impacted by the softer market conditions affecting other subsectors. They note continued advantages in resilience and business model stability.

- There is optimism regarding Marsh & McLennan's potential for organic and inorganic growth. Several analysts point to strong execution and defensive characteristics within the commercial lines segment.

- The firm’s Overweight rating by certain bullish analysts is supported by its positioning to benefit from ongoing sector transitions and the prospect of further market share gains.

- Over the longer term, the company’s ability to generate steady fee income and maintain strong underwriting margins is seen as a key driver for premium valuation multiples.

- Bearish analysts are trimming price targets on Marsh & McLennan, citing persistent headwinds in commercial property pricing and ongoing pressures on sector-wide margins.

- Concerns remain around slowing growth in both primary and reinsurance domains, which could weigh on near-term results and limit upside to consensus estimates.

- Some research notes point to increased competition in key insurance markets. Alongside irrational pricing trends, this adds risk to the firm’s forward growth outlook.

- Higher costs of capital in the reinsurance segment and softening pricing are noted as additional risks that could hamper future returns and compress profit margins if these trends persist.

What's in the News

- Marsh & McLennan Companies completed a $300 million share repurchase, buying back 1,331,866 shares from April 1, 2025 to June 30, 2025 (Key Developments).

- Since the launch of its buyback program in November 2010, the firm has bought back 146,802,738 shares, representing 28.01% of total shares, for $12,045.25 million (Key Developments).

Valuation Changes

- Fair Value: Lowered modestly from $232.42 to $228.53, reflecting updated analyst targets.

- Discount Rate: Remains unchanged at 6.78%.

- Revenue Growth: Edged up slightly from 5.95% to 5.96%.

- Net Profit Margin: Marginally increased from 17.42% to 17.45%.

- Future P/E: Decreased from 26.10x to 25.62x. This indicates a modest contraction in forward valuation multiples.

Key Takeaways

- Growing risk complexity and regulatory demands are fueling long-term global demand for the company's advisory, insurance, and consulting services.

- Strategic digital investments and acquisitions are driving operational efficiency, service breadth, and market expansion, supporting sustained earnings growth.

- Ongoing pricing declines, consulting demand uncertainty, acquisition challenges, liability cost pressures, and tech disruption risk threaten long-term revenue stability and profit growth.

Catalysts

About Marsh & McLennan Companies- A professional services company, provides advisory services and insurance solutions to clients in the areas of risk, strategy, and people worldwide.

- Rising global risk complexity-including increased litigation, extreme weather, catastrophic events, cyber threats, and evolving AI risks-is expected to drive higher demand for Marsh & McLennan's specialized risk advisory and brokerage services, supporting long-term fee revenue and new client growth.

- Expansion of the global middle class, particularly in emerging markets like Latin America, Asia, and EMEA, is fueling robust demand for insurance and risk management solutions, as reflected in continued high single-digit international revenue growth, which should expand the company's addressable market and underpin top-line growth.

- Ongoing regulatory tightening and evolving compliance requirements worldwide are increasing the need for consulting, actuarial, and risk management advisory expertise, creating resilient demand and supporting stable revenues for the firm's consulting divisions.

- Strategic investments in digital transformation, advanced analytics, and AI (e.g., proprietary data tools for risk modeling, agentic interfaces) are expected to enhance operational efficiency and improve product/service offerings, enabling margin expansion and net earnings growth through improved client retention and lower cost to serve.

- Acquisition-driven growth, demonstrated by recent transactions like McGriff and successful integration of wealth management businesses, is broadening Marsh & McLennan's service portfolio and geographic footprint, enabling scale advantages and contributing to higher consolidated earnings over time.

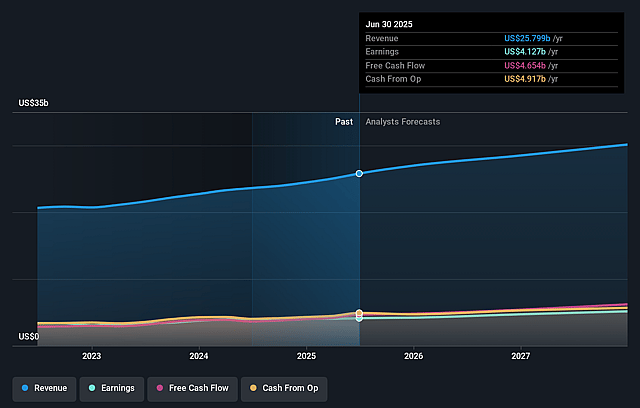

Marsh & McLennan Companies Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Marsh & McLennan Companies's revenue will grow by 5.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 16.0% today to 17.4% in 3 years time.

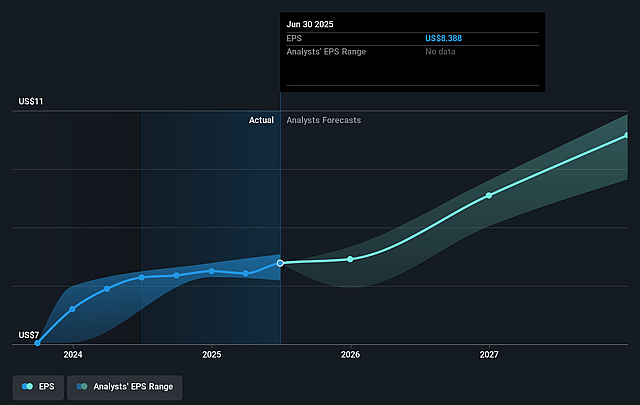

- Analysts expect earnings to reach $5.3 billion (and earnings per share of $11.3) by about September 2028, up from $4.1 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $4.8 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 26.1x on those 2028 earnings, up from 24.0x today. This future PE is greater than the current PE for the GB Insurance industry at 14.3x.

- Analysts expect the number of shares outstanding to grow by 0.1% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.78%, as per the Simply Wall St company report.

Marsh & McLennan Companies Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The persistent decline in property and reinsurance pricing, as highlighted by several consecutive quarters of price decreases and ongoing soft market conditions, threatens Marsh & McLennan's revenue growth and commission income, which may impact both top-line revenue and profitability over the long term.

- Structural decline and slowing demand in discretionary and project-based consulting services (notably in Mercer's Career segment and in project-based pension consulting) expose the company to greater revenue volatility and earnings risk, especially during periods of economic or labor market uncertainty that shrink client spend.

- The company faces elevated operational risk and margin pressure from integrating large acquisitions such as McGriff, further exacerbated by increased debt levels and significant acquisition-related charges, which could hinder net margin expansion and earnings growth if synergies fail to materialize as planned.

- Growing exposure to litigation-driven increases in U.S. liability insurance costs and the prevalence of "nuclear verdicts" create client hesitancy, higher insurance costs, and potential reductions in insurance demand, which may dampen both revenue and client retention rates in key U.S. markets.

- Rapid adoption of advanced analytics, AI, and insurtech across the industry poses a long-term risk of traditional service disintermediation; if Marsh & McLennan fails to keep pace with faster, more nimble digital-first competitors, its margins and fee-based revenues could be eroded by shrinking pricing power and client migration to tech-enabled alternatives.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $232.421 for Marsh & McLennan Companies based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $258.0, and the most bearish reporting a price target of just $197.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $30.7 billion, earnings will come to $5.3 billion, and it would be trading on a PE ratio of 26.1x, assuming you use a discount rate of 6.8%.

- Given the current share price of $201.88, the analyst price target of $232.42 is 13.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.