Key Takeaways

- Rising administrative expenses and persistent higher lapse rates could pressure net margins and limit premium revenue growth.

- Regulatory inquiries and higher claims costs may pose risks to profitability and financial projections.

- Globe Life's solid revenue growth across life and health insurance, coupled with strong investments and share repurchases, highlights financial resilience and effective strategic execution.

Catalysts

About Globe Life- Through its subsidiaries, provides various life and supplemental health insurance products, and annuities to lower middle- and middle-income families in the United States.

- Despite expectations for revenue growth in 2025, increasing administrative expenses, especially IT and employee costs, could put pressure on net margins and earnings.

- The decline in net health sales and the associated higher claims costs at United American are anticipated to continue, which might limit growth in health underwriting margins as a percentage of premium, impacting overall profitability.

- The persistent higher lapse rates, particularly in the Direct-to-Consumer channel, could lead to lower retention rates, which might constrain life premium revenue growth.

- The impact of higher subsidiary dividends to the parent, coupled with lower growth in average invested assets due to reinsurance, might result in flat to declining excess investment income, potentially affecting overall earnings.

- Regulatory inquiries by the SEC, DOJ, and EEOC create uncertainty, and without clear resolutions, they may pose a risk to financial projections, along with any associated legal costs reflected in earnings.

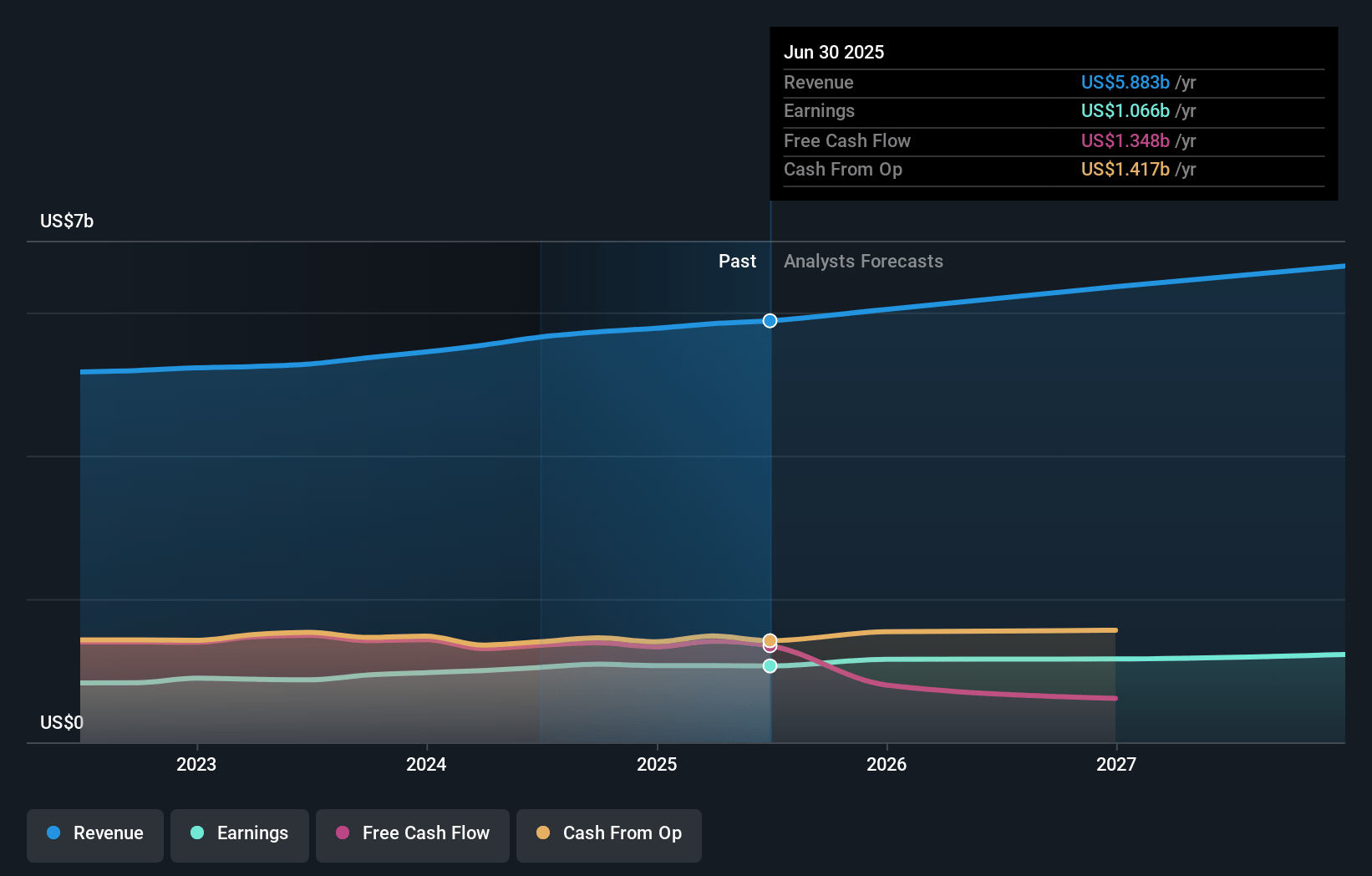

Globe Life Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Globe Life compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Globe Life's revenue will grow by 3.9% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 18.5% today to 18.9% in 3 years time.

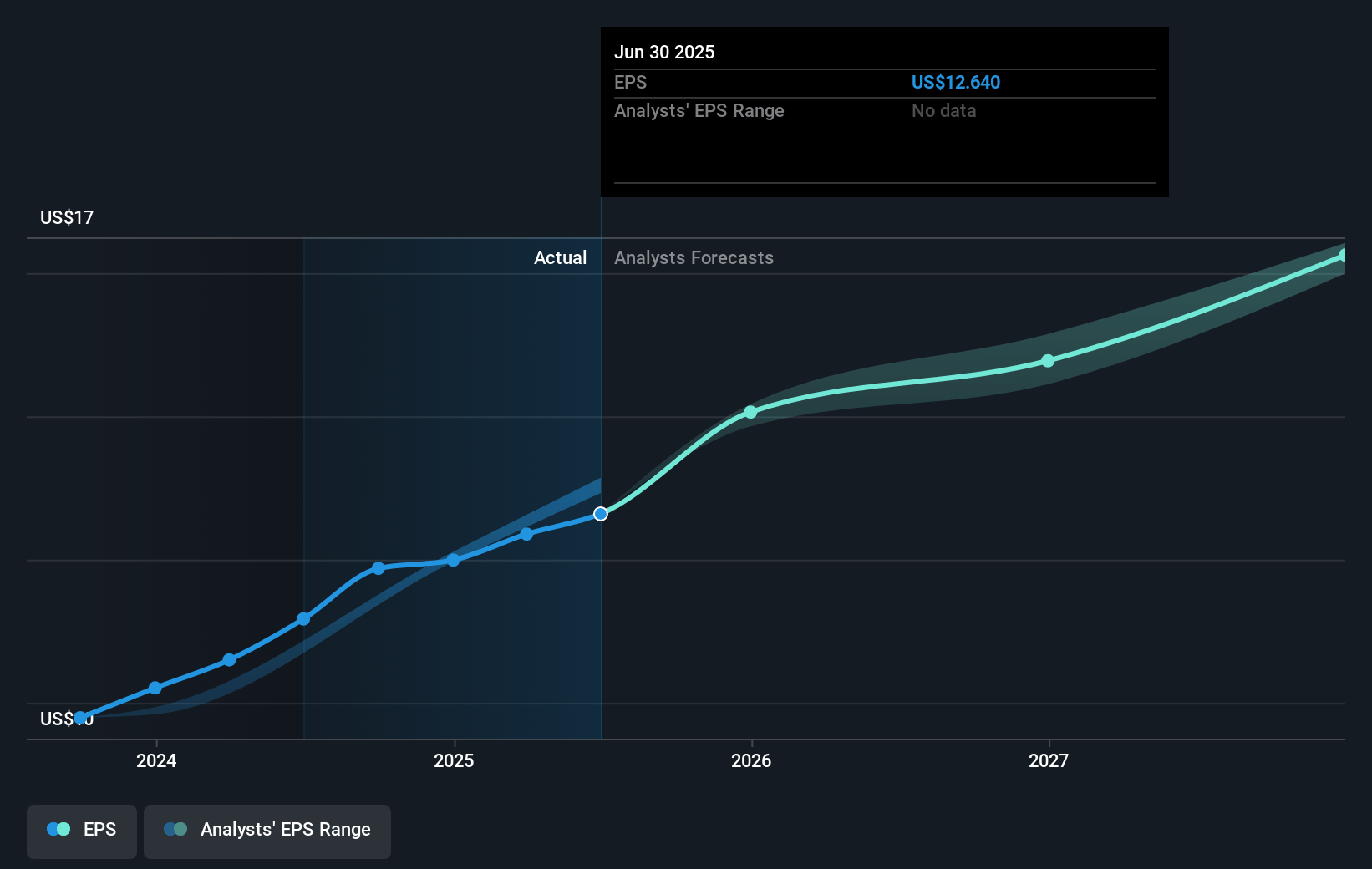

- The bearish analysts expect earnings to reach $1.2 billion (and earnings per share of $16.29) by about April 2028, up from $1.1 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 7.7x on those 2028 earnings, down from 9.6x today. This future PE is lower than the current PE for the GB Insurance industry at 13.5x.

- Analysts expect the number of shares outstanding to decline by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.21%, as per the Simply Wall St company report.

Globe Life Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Globe Life's life insurance premium revenue grew by 4% in the fourth quarter, demonstrating resilience in revenue generation and an ability to sustain growth despite economic conditions.

- The company is expecting further life premium revenue growth of 4.5% to 5% in 2025, suggesting a solid revenue outlook based on strong sales and agent recruiting efforts.

- Despite higher claim costs, health insurance saw a premium revenue increase of 7%, showing potential for revenue growth to continue as the company anticipates a 7.5% to 8.5% increase in 2025.

- With strong performance in their investments, Globe Life's net investment income increased by 4% supported by a 3% growth in average invested assets and higher interest rates, positively impacting earnings.

- Share repurchase efforts resulted in the company returning over $1 billion to shareholders in 2024, showcasing financial strength and the ability to positively influence earnings per share.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Globe Life is $119.23, which represents one standard deviation below the consensus price target of $141.18. This valuation is based on what can be assumed as the expectations of Globe Life's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $188.0, and the most bearish reporting a price target of just $111.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $6.5 billion, earnings will come to $1.2 billion, and it would be trading on a PE ratio of 7.7x, assuming you use a discount rate of 6.2%.

- Given the current share price of $123.92, the bearish analyst price target of $119.23 is 3.9% lower. The relatively low difference between the current share price and the analyst bearish price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is an employee of Simply Wall St, but has written this narrative in their capacity as an individual investor. AnalystLowTarget holds no position in NYSE:GL. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. This narrative is general in nature and explores scenarios and estimates created by the author. The narrative does not reflect the opinions of Simply Wall St, and the views expressed are the opinion of the author alone, acting on their own behalf. These scenarios are not indicative of the company's future performance and are exploratory in the ideas they cover. The fair value estimate's are estimations only, and does not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that the author's analysis may not factor in the latest price-sensitive company announcements or qualitative material.