Key Takeaways

- Goosehead's growth strategy focuses on expanding its franchise network, enhancing agent productivity, and leveraging technology to boost revenue and net margins substantially.

- Strategic partnerships with mortgage servicers and investments in top talent and technology aim to expand its client base and earnings while enhancing shareholder value.

- Reliance on pricing and growth strategies could pressure margins, while franchise consolidation and macroeconomic risks impact revenue and earnings potential.

Catalysts

About Goosehead Insurance- Operates as a holding company for Goosehead Financial, LLC that engages in the provision of personal lines insurance agency services in the United States.

- Goosehead Insurance is planning an ambitious growth strategy by expanding its franchise network, focusing on high-quality franchise owners, and potentially doubling agent productivity. This strategic shift is expected to significantly boost revenue growth.

- The introduction of new technologies, including AI and automation, aims to enhance operational efficiencies and client experience, potentially increasing net margins and positioning the company for exponential revenue and earnings growth.

- Goosehead's focus on developing a robust enterprise sales channel, particularly through partnerships with large mortgage servicers, could expand its client base and significantly increase earnings and revenue through strategic B2B alliances.

- The company is investing heavily in attracting top-tier talent and has a strategic expansion plan for corporate offices in geographically advantageous markets. This is expected to improve agent productivity and increase revenue and net margins over time.

- Goosehead's high cash flow generation allows for strategic capital deployment, including a $100 million share repurchase authorization, aimed at enhancing shareholder value by growing earnings per share.

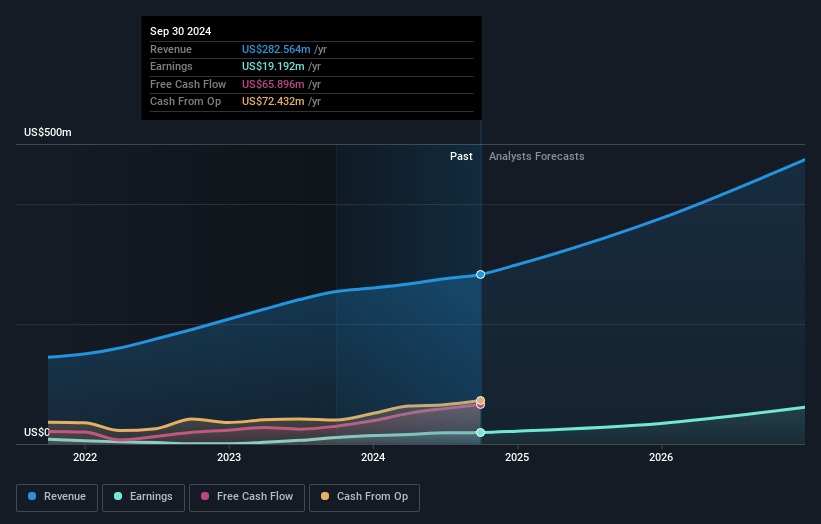

Goosehead Insurance Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Goosehead Insurance's revenue will grow by 21.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 9.5% today to 11.6% in 3 years time.

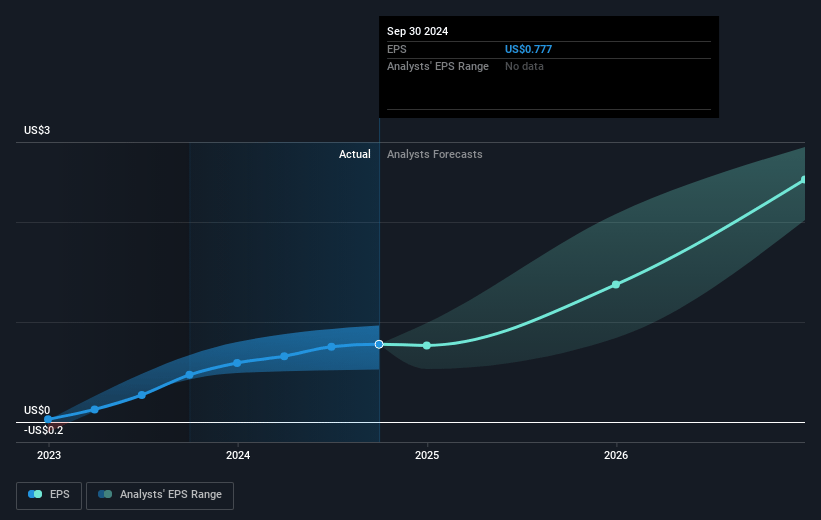

- Analysts expect earnings to reach $67.4 million (and earnings per share of $2.47) by about April 2028, up from $31.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 74.3x on those 2028 earnings, down from 77.6x today. This future PE is greater than the current PE for the US Insurance industry at 14.1x.

- Analysts expect the number of shares outstanding to decline by 0.71% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.21%, as per the Simply Wall St company report.

Goosehead Insurance Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The reliance on desired pricing stability for growth, particularly given historical pricing pressures in key markets like Texas, may impact net margins if price increases continue to exceed retention-improving thresholds of less than 25%.

- While there is optimism about recovery in product availability, particularly in the auto and home insurance sectors, continued adverse conditions or new market entrants could pressure revenue and margins, delaying the anticipated recovery.

- Emphasis on investment in technology and new talent could put upward pressure on G&A expenses, potentially affecting net earnings if the expected revenue growth does not materialize adequately to offset these costs.

- The acquisition and consolidation within the franchise network highlight potential risks regarding franchise stability and productivity; if less productive franchises do not improve under new ownership, this could impact revenue growth and earnings.

- The potential recessionary impacts and macroeconomic uncertainties are noted as having little effect on the guidance but could nonetheless challenge revenue, especially if client retention does not rebound as anticipated in a recovering market.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $116.111 for Goosehead Insurance based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $150.0, and the most bearish reporting a price target of just $43.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $581.9 million, earnings will come to $67.4 million, and it would be trading on a PE ratio of 74.3x, assuming you use a discount rate of 6.2%.

- Given the current share price of $95.92, the analyst price target of $116.11 is 17.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.