Key Takeaways

- Strategic innovation and new product offerings are enhancing customer adoption, providing diversified revenue growth opportunities for Veeva Systems.

- Reduced reliance on third-party platforms and better service project execution could improve profit margins and earnings stability.

- Dependence on continuous innovation and regulatory uncertainties could stagnate growth, with macroeconomic factors potentially affecting future revenue and customer behaviors.

Catalysts

About Veeva Systems- Provides cloud-based software for the life sciences industry.

- Veeva Systems anticipates continuous innovation of features for its Vault CRM, which is expected to improve customer adoption and retention, positively impacting future revenue growth.

- The development of MLR Bot as a separate license offers additional monetization opportunities, suggesting an increase in future revenue streams from Commercial Cloud products.

- Strategic partnerships in Development Cloud are expected to expand Veeva’s customer base and enhance product adoption, supporting increased revenue and earnings in the long term.

- The transition to Vault CRM among existing customers implies a potential reduction in reliance on third-party platforms, which could improve margins due to lower royalty obligations.

- Improved execution in service projects, leading to faster completion rates, may enhance service revenue growth and overall earnings stability moving forward.

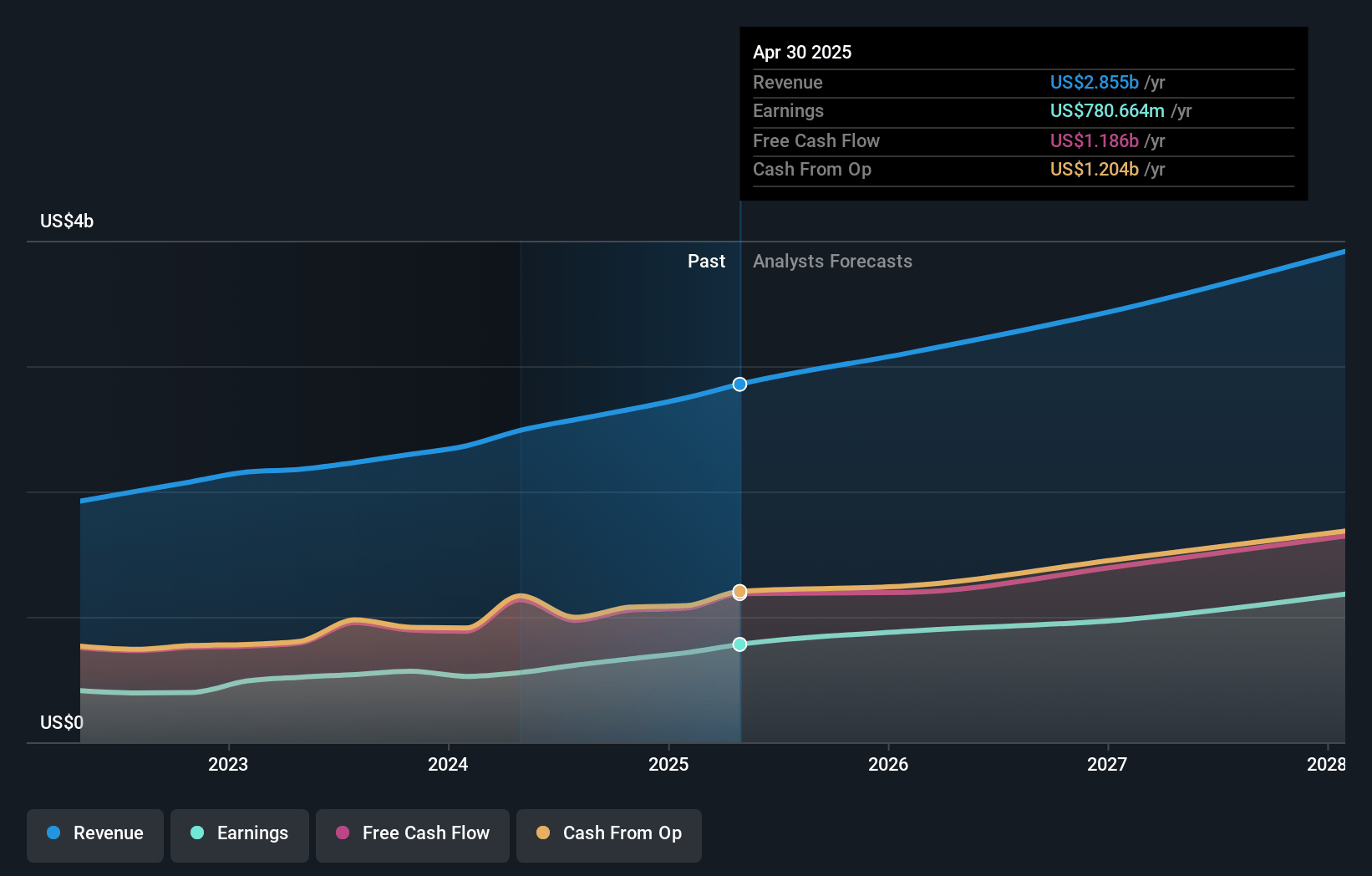

Veeva Systems Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Veeva Systems's revenue will grow by 12.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 25.1% today to 27.3% in 3 years time.

- Analysts expect earnings to reach $1.0 billion (and earnings per share of $6.15) by about January 2028, up from $665.9 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 52.1x on those 2028 earnings, down from 56.6x today. This future PE is lower than the current PE for the US Healthcare Services industry at 58.9x.

- Analysts expect the number of shares outstanding to grow by 1.14% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.67%, as per the Simply Wall St company report.

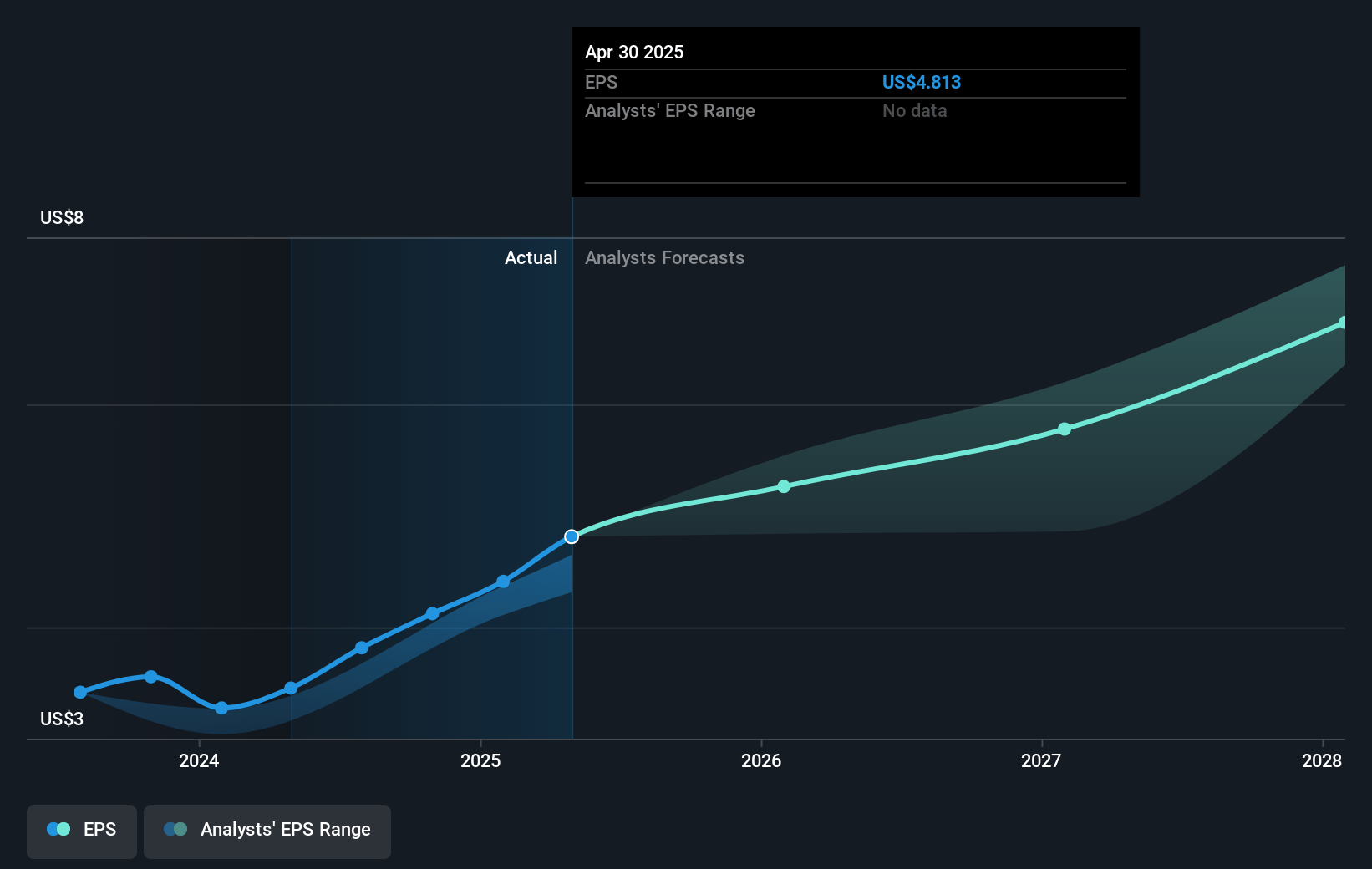

Veeva Systems Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The necessity of multi-year ramps and predefined billings in CDMS indicates that growth in these areas is slower and predictable, potentially leading to stagnation in revenue streams over time.

- The potential requirement of a separate license for MLR Bot reflects uncertainty in monetization and could result in lower-than-expected additional revenue growth in the commercial sector.

- While innovation is emphasized, dependence on continuous feature enhancement and migration (e.g., Vault CRM) involves transition risks that may deter some large-scale customers, potentially impacting earnings.

- Regulatory shifts, particularly regarding direct-to-consumer advertising, present uncertainties that could disrupt commercial strategies and affect revenue streams and net margins in the long term.

- Potential macroeconomic uncertainties and geopolitical tensions could lead to disruptions or changes in customer spending behaviors and priorities, which might impact future revenue growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $265.43 for Veeva Systems based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $320.0, and the most bearish reporting a price target of just $195.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $3.8 billion, earnings will come to $1.0 billion, and it would be trading on a PE ratio of 52.1x, assuming you use a discount rate of 6.7%.

- Given the current share price of $232.24, the analyst's price target of $265.43 is 12.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives