Narratives are currently in beta

Key Takeaways

- Expansion of care facilities and new Medicaid programs could enhance acute care revenue and overall financial potential.

- Strategic initiatives in behavioral health pricing and outpatient services could stabilize margins and drive long-term growth.

- Aggressive payer practices and increased costs from regulations and liabilities could threaten revenue growth and profitability in acute and behavioral segments.

Catalysts

About Universal Health Services- Through its subsidiaries, owns and operates acute care hospitals, and outpatient and behavioral health care facilities.

- Expansion of inpatient and ambulatory care capacity, with new hospitals opening in Las Vegas, Washington D.C., and Palm Beach Gardens, expected to enhance future acute care revenue as these facilities begin and expand operations.

- Approval of new Medicaid supplemental payment programs in Tennessee, Washington D.C., and Nevada, which, if actualized, could provide significant additional revenue, potentially $40 million to $85 million annually from each program.

- Continuing margin recovery and efficiency initiatives, particularly in managing labor costs, are expected to stabilize expenses and improve net margins.

- The shift towards higher pricing in the behavioral health segment, with a transition from lower-paying managed Medicaid to higher-margin contracts, could positively affect revenue and net margins.

- The strategic focus on expanding outpatient and telehealth services, alongside increased alignment with physicians, could drive long-term revenue growth by capturing more patient volume and enhancing service offerings.

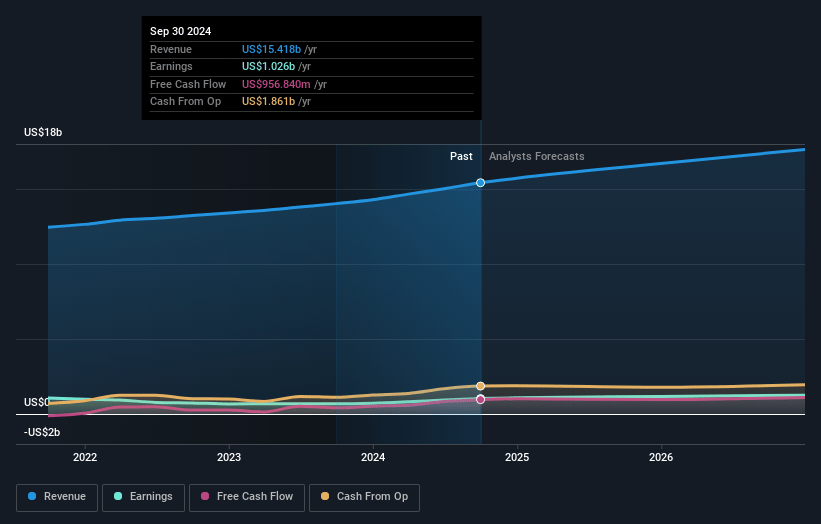

Universal Health Services Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Universal Health Services's revenue will grow by 6.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 6.7% today to 7.2% in 3 years time.

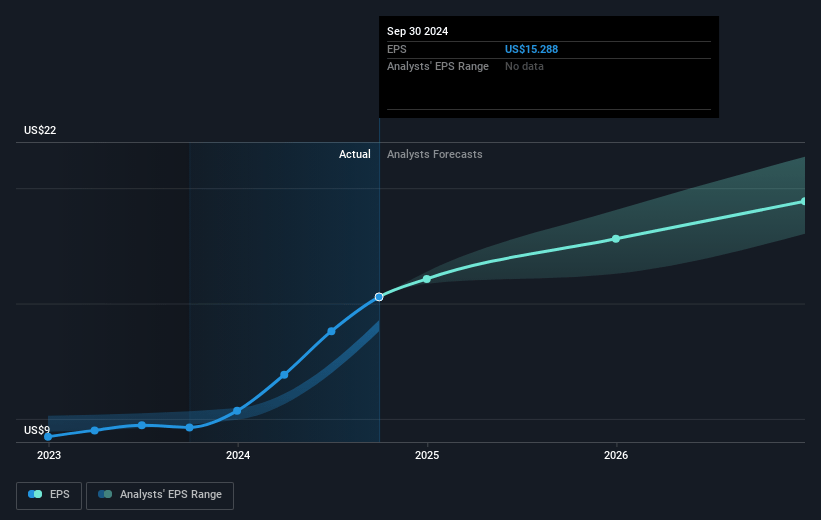

- Analysts expect earnings to reach $1.3 billion (and earnings per share of $21.06) by about December 2027, up from $1.0 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 13.4x on those 2027 earnings, up from 11.7x today. This future PE is lower than the current PE for the US Healthcare industry at 22.0x.

- Analysts expect the number of shares outstanding to decline by 1.42% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.03%, as per the Simply Wall St company report.

Universal Health Services Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Managed care payers have become more aggressive with patient denials and status changes, potentially impacting revenue growth in both acute and behavioral segments.

- Physician expenses, particularly for emergency room and anesthesiologists, could rise due to billing changes and regulations like the No Surprise billing act, which may increase net margins pressure.

- The future approval and timing of state Medicaid supplemental payment programs are uncertain, which could affect expected revenue streams and overall earnings.

- The impact of hurricane-related disruptions in certain geographic regions may lead to variability in quarterly revenues, as noted with behavioral health volume impacts, affecting earnings stability.

- Rising reserves for self-insured liability claims could signal increased legal and settlement costs, negatively impacting net margins and profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $238.21 for Universal Health Services based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $274.0, and the most bearish reporting a price target of just $197.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $18.4 billion, earnings will come to $1.3 billion, and it would be trading on a PE ratio of 13.4x, assuming you use a discount rate of 6.0%.

- Given the current share price of $181.22, the analyst's price target of $238.21 is 23.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives