Last Update07 May 25

Key Takeaways

- Molina's successful RFP wins and Medicaid strategy are poised to enhance revenue, EPS growth, and net margins through efficient care coordination.

- Strategic acquisitions and disciplined medical cost management are expected to stabilize margins and boost future earnings, supporting capital deployment and growth.

- Potential Medicaid funding cuts and operational challenges may hinder Molina Healthcare's revenue growth and earnings stability amid rising medical costs and integration risks.

Catalysts

About Molina Healthcare- Provides managed healthcare services to low-income families and individuals under the Medicaid and Medicare programs and through the state insurance marketplaces.

- Molina's successful track record of winning RFPs, including new contracts in Nevada and Illinois, is expected to drive significant revenue growth, with projected incremental annual premium revenue of approximately $800 million. This should positively impact revenue and EPS growth.

- The company's focus on leveraging its existing Medicaid footprint to serve high-acuity, low-income Medicare beneficiaries is working well and may enhance net margins by streamlining care coordination and administrative costs.

- Expected Medicaid rate adjustments indicate a slightly higher outcome than previously anticipated. This adjustment is likely to impact revenue favorably by aligning payments more closely with anticipated medical trends.

- Molina's acquisition pipeline, comprising many actionable opportunities, could lead to accretive additions and contribute to future earnings. Their strategy to deploy capital in acquisitions is expected to support EPS growth.

- Molina's disciplined approach to medical cost management, amidst enhancements in the rate environment, is likely to stabilize or improve net margins by mitigating the impact of rising medical costs.

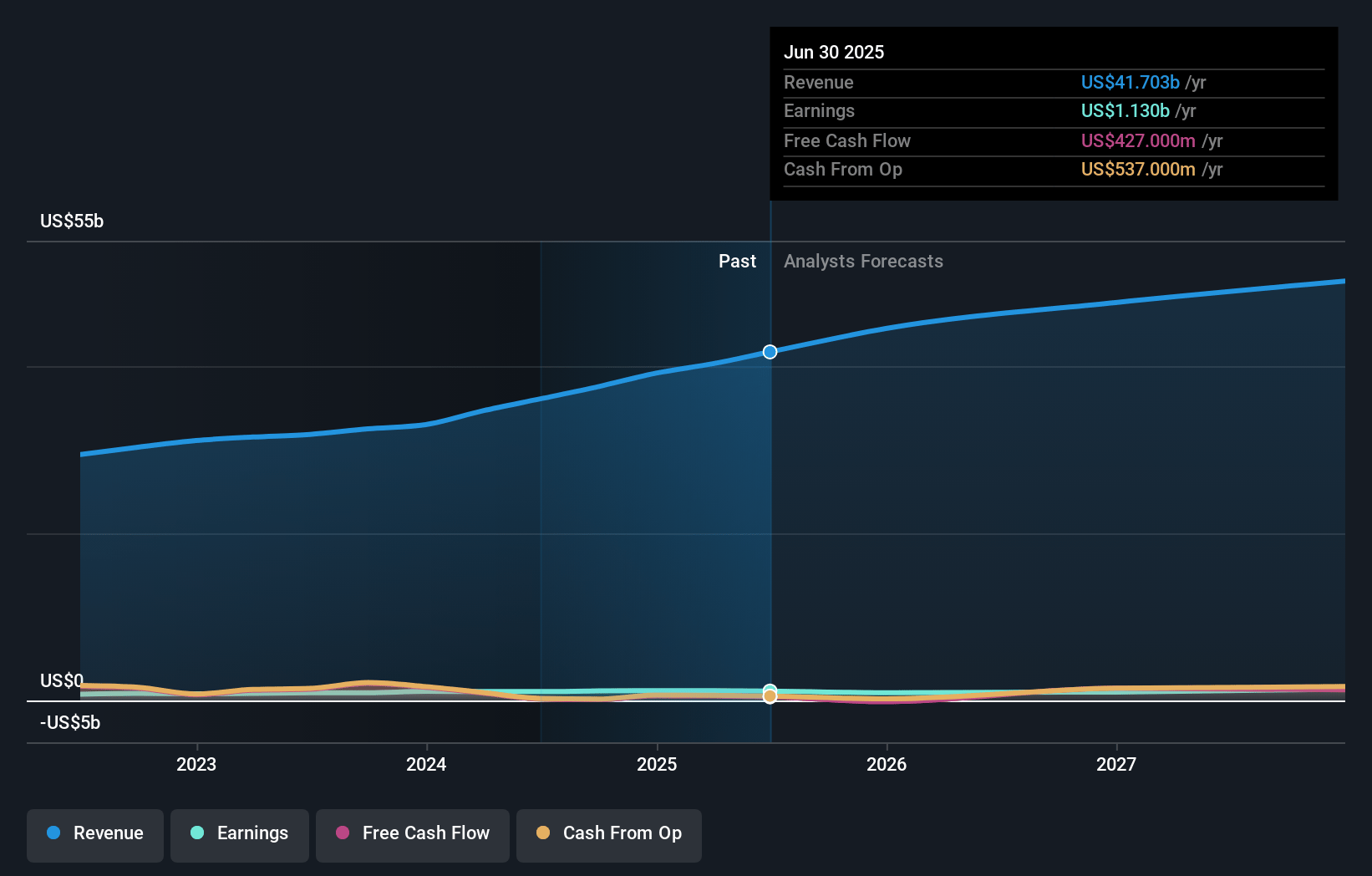

Molina Healthcare Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Molina Healthcare's revenue will grow by 8.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 2.9% today to 3.3% in 3 years time.

- Analysts expect earnings to reach $1.7 billion (and earnings per share of $32.24) by about May 2028, up from $1.2 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 10.8x on those 2028 earnings, down from 14.6x today. This future PE is lower than the current PE for the US Healthcare industry at 19.7x.

- Analysts expect the number of shares outstanding to decline by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.21%, as per the Simply Wall St company report.

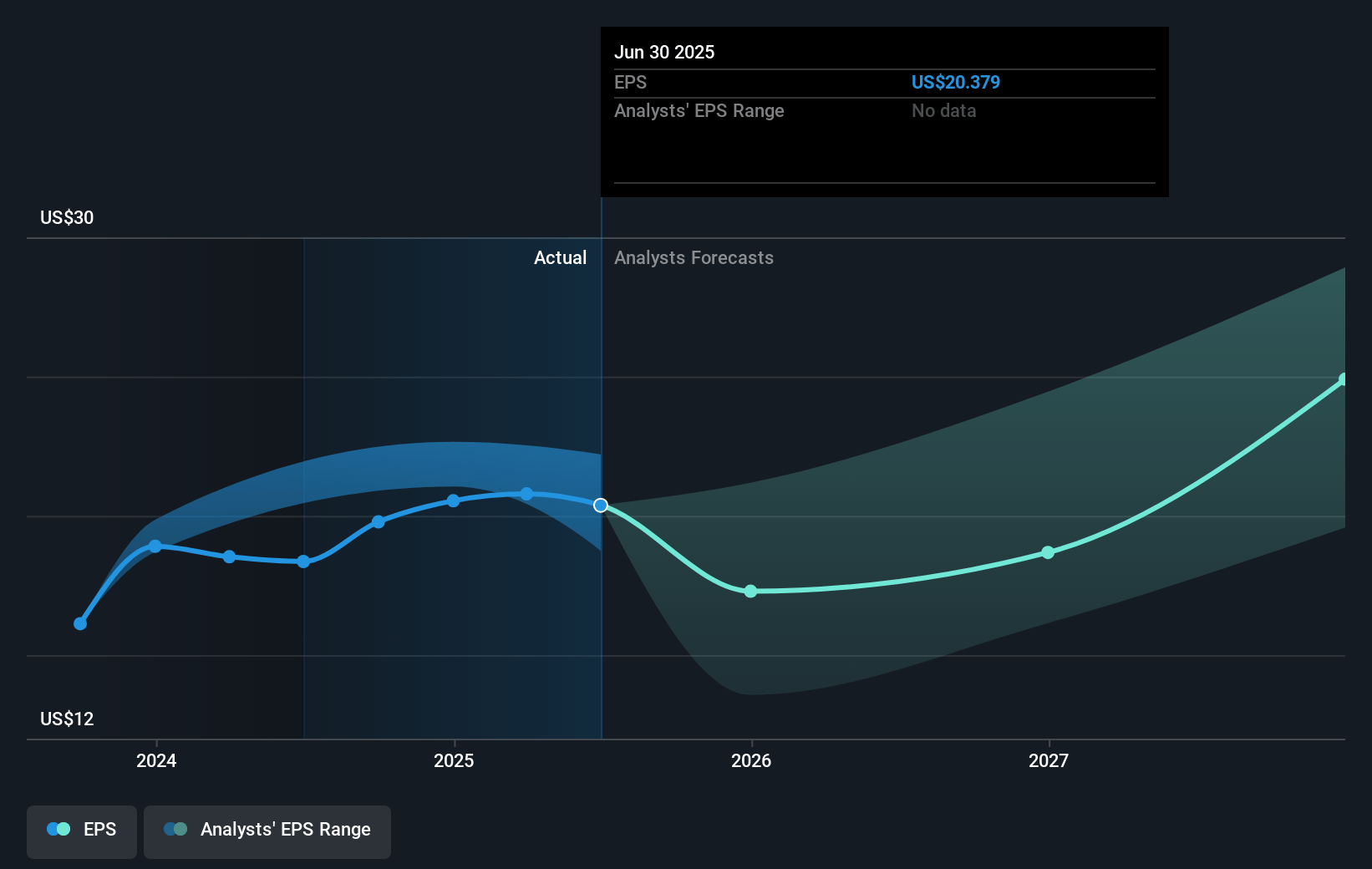

Molina Healthcare Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Potential Medicaid funding cuts or program changes could negatively impact Molina Healthcare's revenue and earnings trajectory.

- The implementation of new Marketplace program integrity initiatives and changes to enhanced subsidies could affect membership growth and lead to potential revenue fluctuations.

- The loss of the Virginia Medicaid contract midyear could reduce projected revenue and earnings if not offset by other membership gains.

- The moderate increase in medical costs due to high-cost drugs and behavioral health services may put pressure on net margins if rate adjustments do not adequately cover the trend.

- New acquisitions, such as ConnectiCare, running higher than target MCR initially could impact earnings if Molina is unable to effectively manage costs and achieve expected integration efficiencies.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $358.75 for Molina Healthcare based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $414.0, and the most bearish reporting a price target of just $291.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $51.9 billion, earnings will come to $1.7 billion, and it would be trading on a PE ratio of 10.8x, assuming you use a discount rate of 6.2%.

- Given the current share price of $316.2, the analyst price target of $358.75 is 11.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.