Key Takeaways

- Manufacturing and leadership enhancements aim to improve operational efficiency, potentially expanding margins and driving revenue growth.

- Divestiture and strategic acquisitions position the company as a specialized medtech player, promising focused growth and higher earnings.

- Integer Holdings' focus on medical technology and ambitious growth plans carries risks of revenue volatility, margin pressure, and reliance on execution success amidst market uncertainties.

Catalysts

About Integer Holdings- Operates as a medical device outsource manufacturer in the United States, Puerto Rico, Costa Rica, and internationally.

- Integer Holdings has implemented Manufacturing Excellence Initiatives which are improving direct labor turnover, material scrap reduction, and labor efficiency, indicating potential future margin expansion. This is likely to impact net margins positively.

- The creation of the Chief Operating Officer role and leadership promotions are aimed at driving strategic execution and operational efficiency, which could result in stronger revenue growth.

- There is a strong sales outlook of 10% to 11% growth for 2024, supported by high visibility into customer demand and capacity expansion in key markets, which should drive future revenue growth.

- The divestiture of the Electrochem business transforms Integer into a pure-play medical technology company, potentially improving focus and efficiency, aiding in higher revenue and net margin growth.

- Recent acquisitions and new product ramps in high-growth areas such as electrophysiology and structural heart are anticipated to accelerate growth, contributing positively to future revenues and earnings.

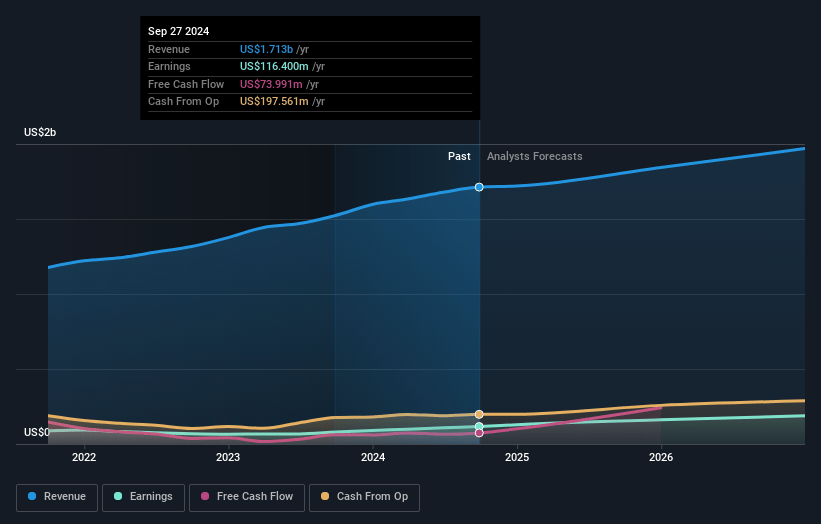

Integer Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Integer Holdings's revenue will grow by 6.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 6.8% today to 10.7% in 3 years time.

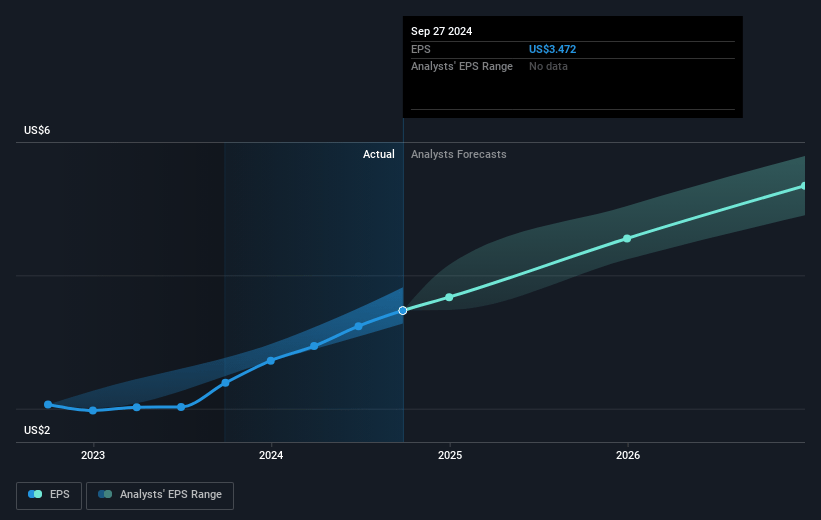

- Analysts expect earnings to reach $220.1 million (and earnings per share of $6.15) by about January 2028, up from $116.4 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 28.8x on those 2028 earnings, down from 41.6x today. This future PE is lower than the current PE for the US Medical Equipment industry at 34.7x.

- Analysts expect the number of shares outstanding to grow by 2.16% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.94%, as per the Simply Wall St company report.

Integer Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Integer Holdings' decision to divest its non-medical Electrochem segment to become a pure-play medical technology company carries the risk of limiting diversification, potentially impacting revenue stability if the medical technology markets face downturns or slower growth.

- The shift in order patterns and softer organic growth in certain segments like Cardiac Rhythm Management could signal demand fluctuations, potentially affecting revenue projections and growth expectations.

- Higher interest expense driven by increased debt levels from acquisitions might pressure net margins and earnings if not offset by operational improvements and robust revenue growth.

- The company's reliance on emerging PMA customers for Neuromodulation growth may introduce volatility if these customers face delays or hurdles in their growth plans, impacting Integer's revenue and earnings projections.

- Integer's ambitious growth targets and margin expansion plans place significant reliance on successful execution of Manufacturing Excellence Initiatives, and any deviations or challenges could affect margins and profitability expectations.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $148.12 for Integer Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $163.0, and the most bearish reporting a price target of just $138.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $2.1 billion, earnings will come to $220.1 million, and it would be trading on a PE ratio of 28.8x, assuming you use a discount rate of 6.9%.

- Given the current share price of $144.36, the analyst's price target of $148.12 is 2.5% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives