Narratives are currently in beta

Key Takeaways

- Strategic Medicaid rate alignment and ACA market expansion could drive revenue growth as higher rates and expanded market share stabilize.

- AI investments and operational efficiencies aim to reduce costs and enhance margins through improved care management and customer satisfaction.

- Elevated medical costs, regulatory challenges, and market competition pose risks to Elevance Health's profit margins and earnings growth in Medicaid and Medicare sectors.

Catalysts

About Elevance Health- Operates as a health benefits company in the United States.

- Elevance Health is actively working with states to align Medicaid rates with member acuity, which is expected to improve revenue as these higher rates are implemented in the future.

- The company plans to enhance operational efficiencies and manage the cost of care through proactive actions, focusing on long-term operating efficiency, which could increase net margins.

- Elevance Health's strategic expansion into Individual Exchange markets by offering ACA plans in additional states is likely to drive revenue growth as the enrollment stabilizes and market share increases.

- The expansion of Carelon, including acquisitions such as Kroger Specialty Pharmacy and CareBridge, is expected to broaden service offerings and increase revenue and earnings from specialty care and home health businesses.

- Investments in AI-driven solutions are anticipated to reduce costs and improve customer satisfaction, eventually contributing to higher net margins through operational improvements.

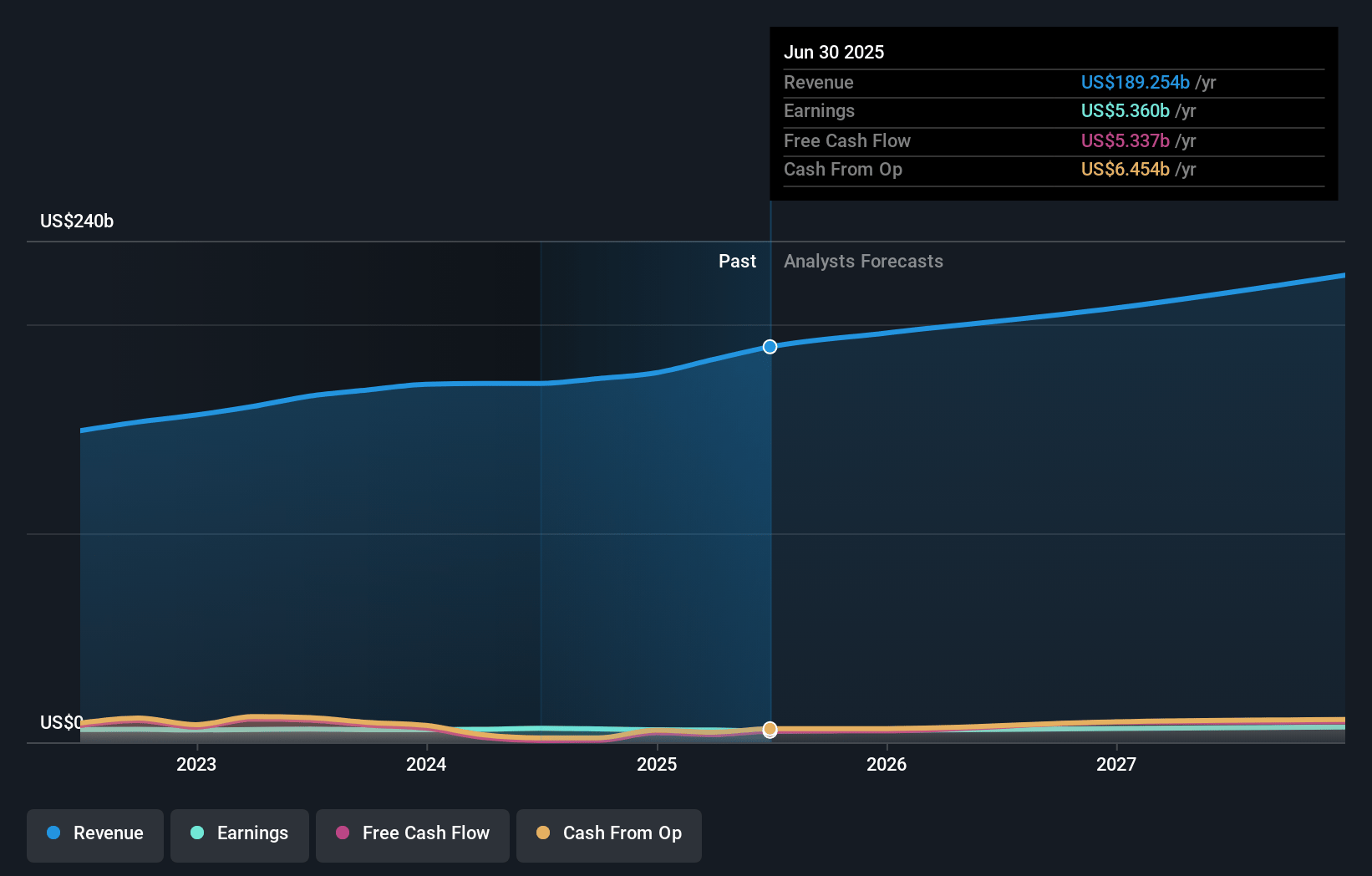

Elevance Health Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Elevance Health's revenue will grow by 7.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 3.7% today to 4.4% in 3 years time.

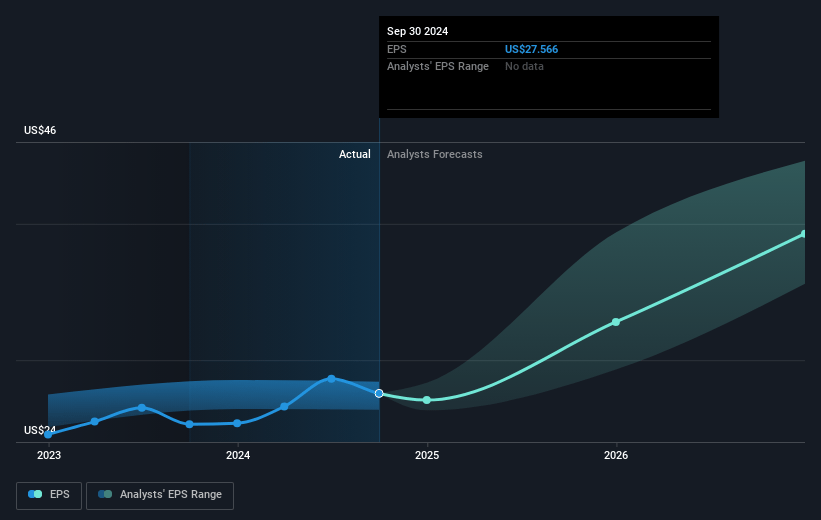

- Analysts expect earnings to reach $9.6 billion (and earnings per share of $44.41) by about January 2028, up from $6.4 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $7.6 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 13.4x on those 2028 earnings, down from 13.8x today. This future PE is lower than the current PE for the US Healthcare industry at 23.7x.

- Analysts expect the number of shares outstanding to decline by 2.35% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.97%, as per the Simply Wall St company report.

Elevance Health Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Elevated medical costs in the Medicaid business are creating headwinds, impacting Elevance Health's adjusted diluted earnings per share and benefit expense ratio, potentially affecting net margins.

- There is a mismatch between Medicaid rates and member acuity, with states often using outdated data to set rates, leading to inadequate rate increases and affecting the company's earnings visibility and profit margins.

- Unexpected accelerated cost trends and unfavorable prior period development, particularly affecting Medicaid, are challenging the company's ability to maintain desired profit margins and earnings growth.

- Regulatory and market pressures in Medicare Advantage, including rate cuts by CMS and reductions in star ratings, could challenge future earnings and market positioning.

- Competition in the Individual Exchange business, and expansion into new markets, though a growth opportunity, presents execution risks that could impact revenue sustainability and profit margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $500.87 for Elevance Health based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $625.0, and the most bearish reporting a price target of just $388.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $217.1 billion, earnings will come to $9.6 billion, and it would be trading on a PE ratio of 13.4x, assuming you use a discount rate of 6.0%.

- Given the current share price of $380.75, the analyst's price target of $500.87 is 24.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

NA

NateF

Community Contributor

ELV Market Outlook

Elevance Health, Inc. (NYSE: ELV) is a prominent player in the health benefits industry, offering a range of services including medical, pharmaceutical, dental, and behavioral health plans.

View narrativeUS$390.54

FV

1.3% undervalued intrinsic discount6.79%

Revenue growth p.a.

0users have liked this narrative

0users have commented on this narrative

6users have followed this narrative

12 days ago author updated this narrative