Narratives are currently in beta

Key Takeaways

- Improved reimbursement rates and favorable policy changes are expected to enhance DaVita's earnings outlook.

- Strategic debt management and international growth initiatives could strengthen DaVita's overall financial performance.

- Rising costs, regulatory challenges, and supply chain disruptions impact DaVita's profits, growth prospects, and require cautious adjustment of financial expectations.

Catalysts

About DaVita- Provides kidney dialysis services for patients suffering from chronic kidney failure in the United States.

- DaVita expects to resume new PD patient starts and normalize supply dynamics by the first quarter of 2025, which could improve future revenue and patient care capability.

- Improved reimbursement rates from CMS for ESRD care, including the integration of oral-only drugs into the Medicare Part B bundle, are anticipated to enhance earnings if implemented favorably.

- DaVita's leverage and interest expense management, with debt maturities pushed to 2028 and interest rate caps in place, could provide a stable earnings outlook.

- Continued growth and integration of the international business and acquisitions in Latin America may bolster overall earnings performance.

- Share repurchases and capital allocation strategies are expected to drive earnings per share (EPS) growth as DaVita continues to return capital to shareholders.

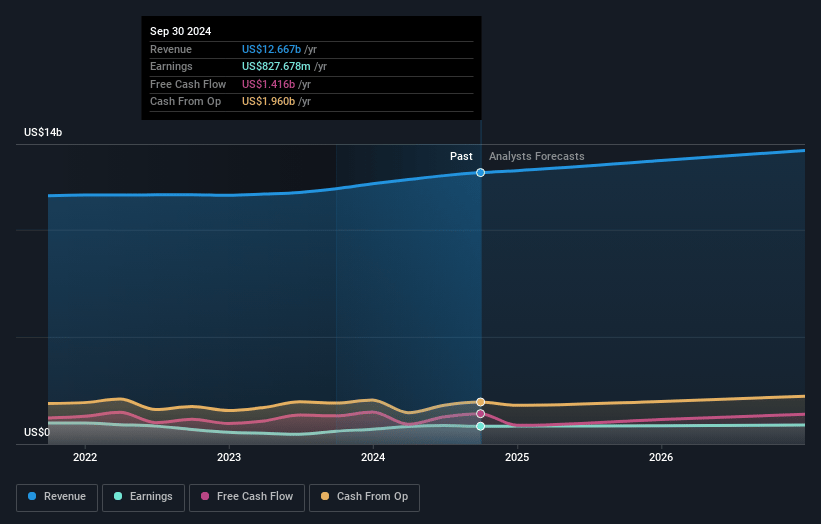

DaVita Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming DaVita's revenue will grow by 3.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 6.5% today to 6.6% in 3 years time.

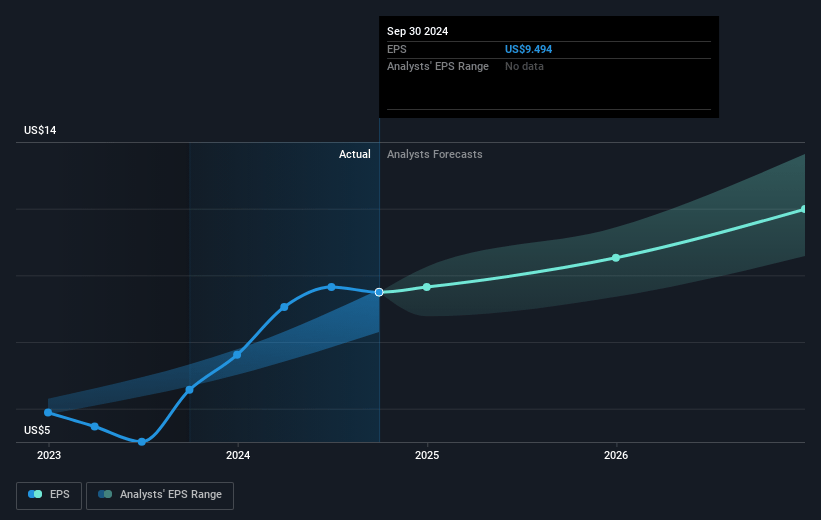

- Analysts expect earnings to reach $940.5 million (and earnings per share of $13.12) by about January 2028, up from $827.7 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $1.1 billion in earnings, and the most bearish expecting $762 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 14.6x on those 2028 earnings, down from 17.2x today. This future PE is lower than the current PE for the US Healthcare industry at 23.7x.

- Analysts expect the number of shares outstanding to decline by 4.37% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.67%, as per the Simply Wall St company report.

DaVita Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Recent hurricanes and related supply chain disruptions have increased costs and impacted productivity, resulting in a projected $10-$20 million impact on fourth quarter financials and potential continuing impact into 2025, affecting operating income and profitability.

- Elevated mortality rates and mistreatment rates due to inclement weather have negatively affected treatment volume growth, which may require downward adjustments to future revenue expectations.

- The supply challenges related to Baxter's closure may lead to temporary suspension of new patient starts on peritoneal dialysis, possibly affecting patient volume growth and future revenue.

- Debt expense has increased significantly due to expired interest rate caps and new debt issuance, which could negatively impact net income due to higher interest obligations.

- Ongoing advocacy and regulatory costs, particularly around issues like the inclusion of orals in the Medicare bundle, could affect general and administrative expenses, thereby impacting net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $159.48 for DaVita based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $186.0, and the most bearish reporting a price target of just $134.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $14.2 billion, earnings will come to $940.5 million, and it would be trading on a PE ratio of 14.6x, assuming you use a discount rate of 6.7%.

- Given the current share price of $173.21, the analyst's price target of $159.48 is 8.6% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives