Narratives are currently in beta

Key Takeaways

- Centene's focus on Medicaid rate adjustments, operational efficiency, and Medicare Advantage could enhance earnings and stabilize future net margins.

- Revenue growth in the Marketplace and Part D segments is expected despite modest margins, supported by policy reforms and legislative acts.

- Medicaid redetermination, inflationary pressures, and regulatory influences challenge Centene’s revenue and profitability across key business segments and strategic growth targets.

Catalysts

About Centene- Operates as a healthcare enterprise that provides programs and services to under-insured and uninsured families, commercial organizations, and military families in the United States.

- Centene is actively engaging with state partners to align Medicaid rates with post-redetermination member acuity, aiming to adjust rates upwards between 4.5% to 5%, which could enhance revenue and stabilize future net margins.

- The company is improving operational efficiency through AI, potentially reducing SG&A expenses over time, which can increase future net margins and earnings.

- Centene is strategically focusing its Medicare Advantage business on low-income and dual-eligible members, with a view to increase its Star ratings, reduce SG&A, and expand margins, which could significantly impact earnings positively.

- The Marketplace segment is expected to maintain margins within the 5% to 7.5% range due to policy reforms that enhance operational integrity, supporting stable revenue and earnings growth.

- Centene anticipates significant revenue growth in its Part D business due to the Inflation Reduction Act, which will enhance earnings, despite expecting a modest 1% margin due to a large revenue base in 2025.

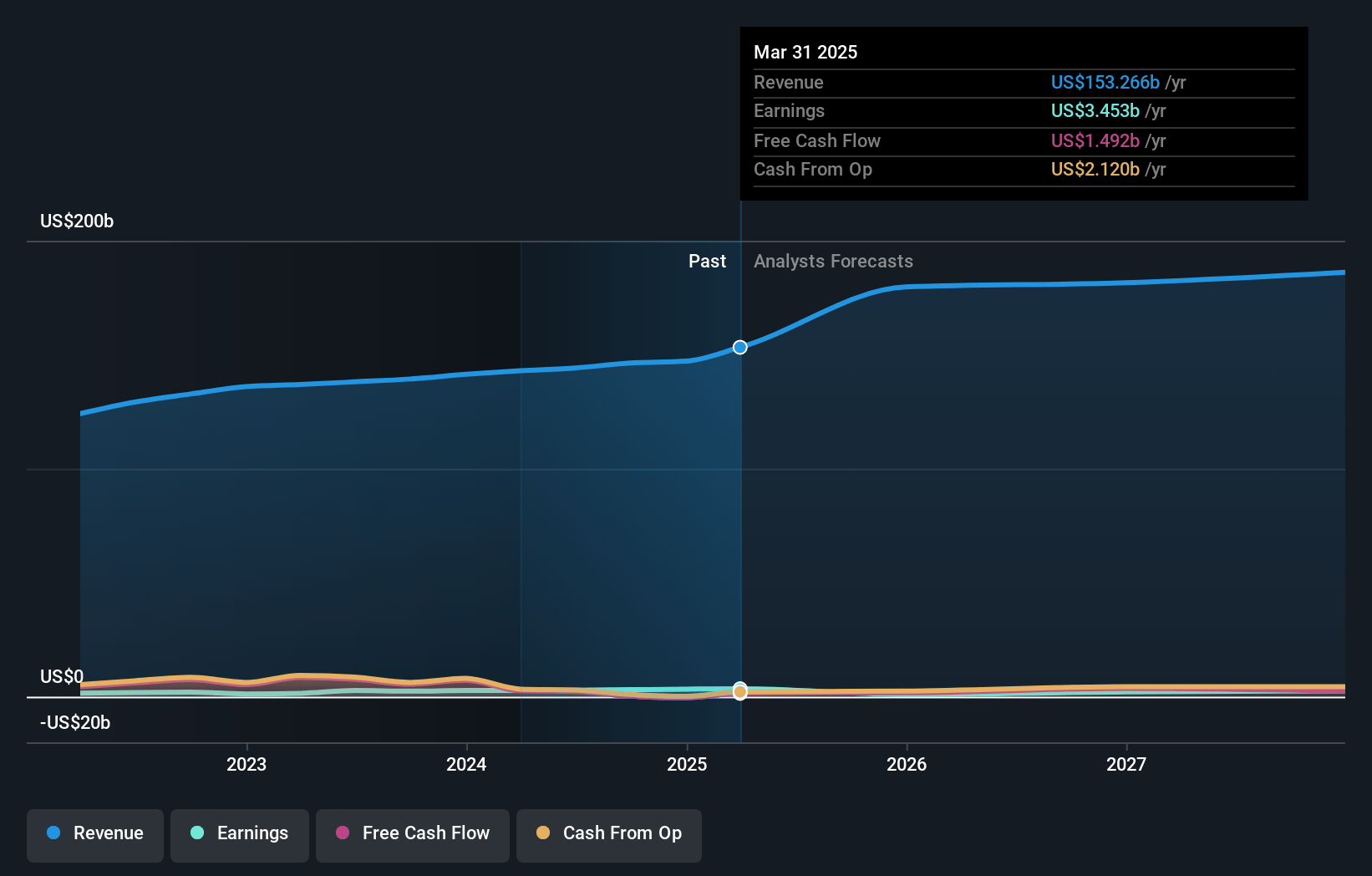

Centene Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Centene's revenue will grow by 6.9% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 2.1% today to 2.0% in 3 years time.

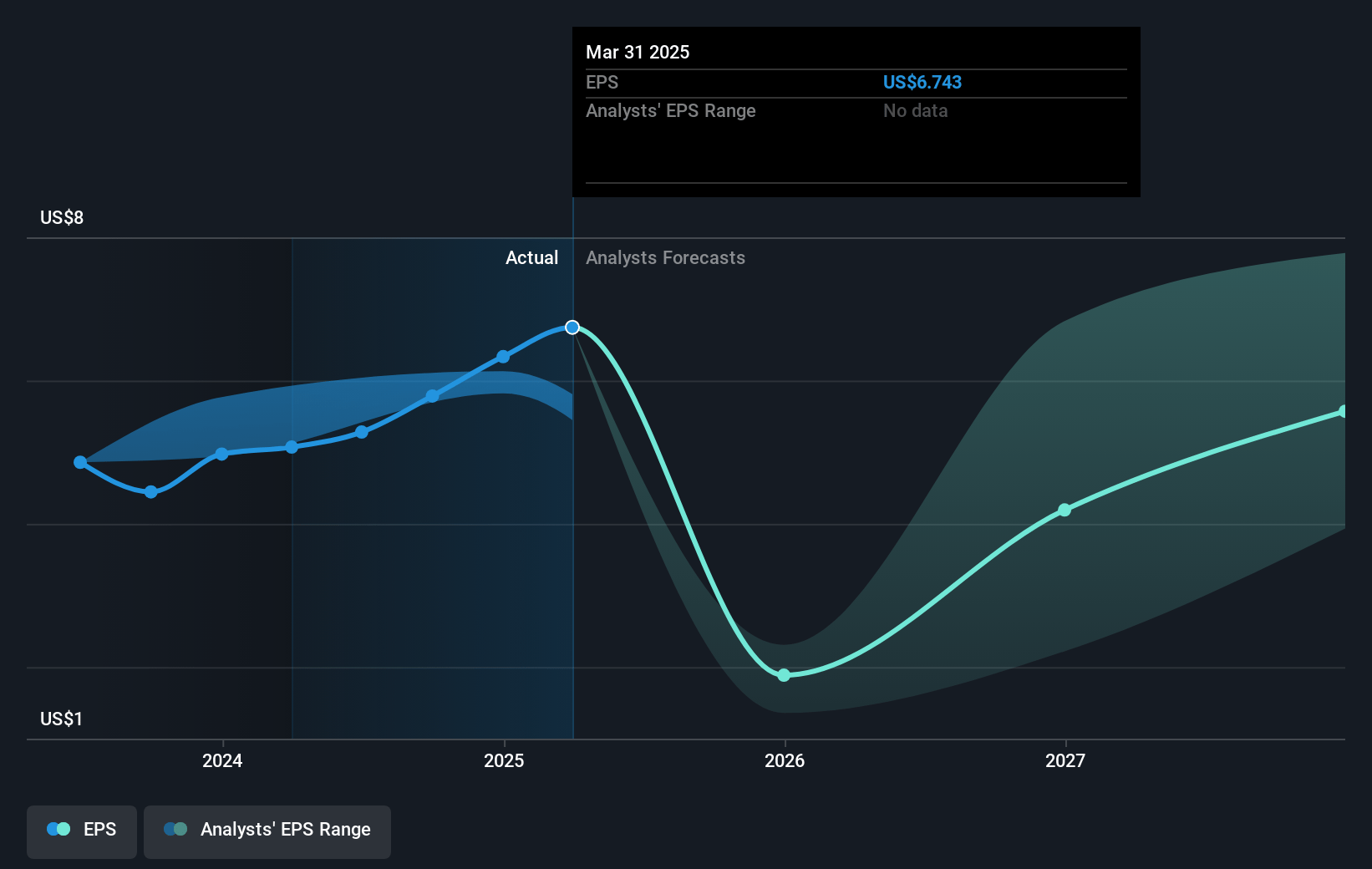

- Analysts expect earnings to reach $3.5 billion (and earnings per share of $7.61) by about January 2028, up from $3.1 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $2.4 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 12.5x on those 2028 earnings, up from 10.7x today. This future PE is lower than the current PE for the US Healthcare industry at 23.7x.

- Analysts expect the number of shares outstanding to decline by 2.77% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.26%, as per the Simply Wall St company report.

Centene Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The ongoing Medicaid redetermination process has created significant pressure on Centene's Medicaid MLR, with rejoiners causing artificial pressure due to gaps in coverage, potentially affecting net margins and overall earnings.

- Some states need to make additional rate adjustments to fully match rates with acuity, creating uncertainty around future revenues and profitability in Centene's largest business segment.

- The inflationary pressures and cost trends, such as increasing utilization in behavioral health and GLP-1 drugs, may not be fully matched by rate increases in all states, impacting Centene's cost structure and net margins.

- The regulatory landscape in the Marketplace segment, including program integrity and IRS reporting requirements, could moderate overall market growth, potentially impacting Centene's revenue expectations and earnings in this segment.

- Centene's efforts to balance Medicare Advantage growth and profitability by exiting certain states may lead to decreased revenue in that segment, affecting overall revenue growth targets and strategic financial outcomes.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $79.45 for Centene based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $93.0, and the most bearish reporting a price target of just $52.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $178.6 billion, earnings will come to $3.5 billion, and it would be trading on a PE ratio of 12.5x, assuming you use a discount rate of 6.3%.

- Given the current share price of $64.72, the analyst's price target of $79.45 is 18.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives