Narratives are currently in beta

Key Takeaways

- Recovery in Nurse Staffing demand and international business conditions indicate potential revenue growth and improved margins from 2025 onwards.

- Investments in technology and diversified solutions enhance operational efficiencies and revenue streams, supporting sustained growth and margin improvements.

- Competitive pressures and industry challenges, including overcapacity and visa issues, threaten profitability, revenue growth, and future margin recovery for AMN Healthcare Services.

Catalysts

About AMN Healthcare Services- Provides healthcare workforce solutions and staffing services to healthcare facilities in the United States.

- AMN Healthcare expects stabilization in the demand for Travel Nurse Staffing, with demand increasing 60% above its low point in April 2024, indicating potential revenue growth in 2025 as market dynamics improve.

- The company is likely to benefit from its investment in technology solutions, such as the WorkWise integrated technology suite, which has received positive feedback. This can enhance operational efficiencies and potentially improve net margins.

- AMN Healthcare is seeing increased client interest in using multiple solution services, with the average number of solutions used by its top clients growing. This diversification could lead to higher revenue streams.

- The international Nurse business, impacted by visa retrogression, is expected to recover as conditions normalize, providing an opportunity for margin improvement and revenue growth from 2025 onwards.

- With the proactive increase in leverage capacity on its revolving line of credit, AMN Healthcare is well-positioned to manage financial flexibility, which can support continued growth initiatives and leverage management, positively impacting earnings.

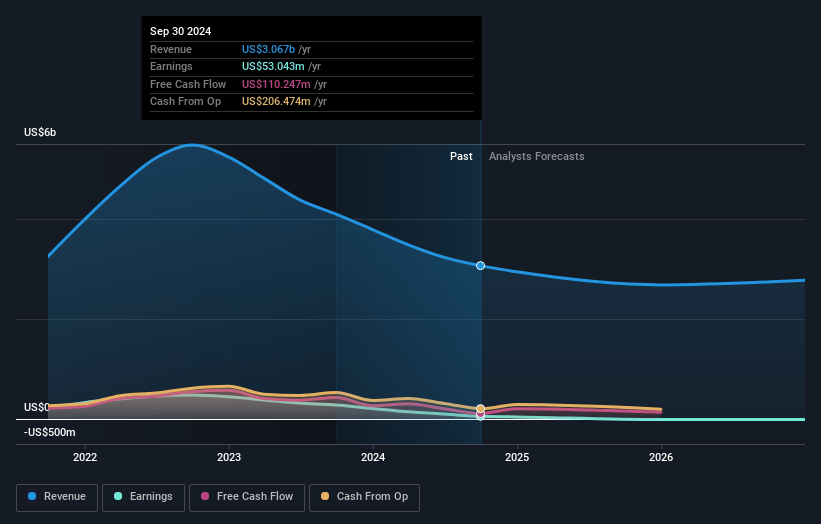

AMN Healthcare Services Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming AMN Healthcare Services's revenue will decrease by -5.2% annually over the next 3 years.

- Analysts are not forecasting that AMN Healthcare Services will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate AMN Healthcare Services's profit margin will increase from 1.7% to the average US Healthcare industry of 4.4% in 3 years.

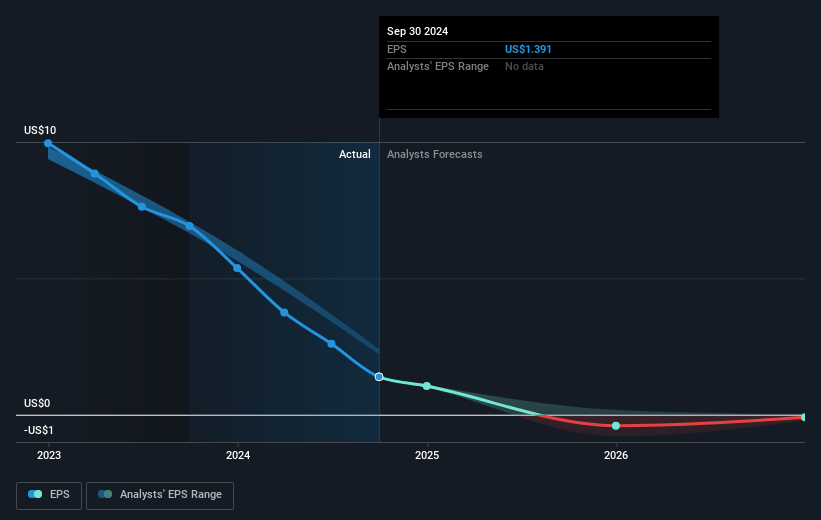

- If AMN Healthcare Services's profit margin were to converge on the industry average, you could exepct earnigns to reach $116.0 million (and earnings per share of $0.0) by about January 2028, down from $53.0 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 57259.6x on those 2028 earnings, up from 19.8x today. This future PE is greater than the current PE for the US Healthcare industry at 23.7x.

- Analysts expect the number of shares outstanding to grow by 1466.88% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.02%, as per the Simply Wall St company report.

AMN Healthcare Services Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The competitive landscape in the staffing industry is intense, leading to compressed gross margins as the fight for orders continues, which can impact overall profitability.

- The overcapacity in the Travel Nurse industry and increased unfilled orders signify a misalignment between client expectations and clinician pay expectations, which may affect revenue growth.

- The decline in Locum tenens revenue and lower demand in interim leadership could result in a negative impact on earnings from the Physician and Leadership Solutions segment.

- Gross margin pressure is compounded by a revenue mix shift and challenges in maintaining bill pay spreads, potentially affecting adjusted EBITDA margins negatively.

- Visa retrogression impacting the international nurse business remains a headwind, decreasing revenue and delaying growth recovery in this segment, which may affect future net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $37.0 for AMN Healthcare Services based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $47.0, and the most bearish reporting a price target of just $27.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $2.6 billion, earnings will come to $116.0 million, and it would be trading on a PE ratio of 57259.6x, assuming you use a discount rate of 7.0%.

- Given the current share price of $27.54, the analyst's price target of $37.0 is 25.6% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives