Narratives are currently in beta

Key Takeaways

- Shifting focus from the insulin patch pump to debt reduction could improve financial flexibility and enhance profitability for future strategic investments.

- Potential pricing and currency exchange rate challenges might compress margins, impacting revenue and earnings growth in the near term.

- Embecta's restructuring and focus on core business, product expansion, and debt reduction aim to enhance profitability, revenue, and financial flexibility in the long term.

Catalysts

About Embecta- A medical device company, focuses on the provision of various solutions to enhance the health and wellbeing of people living with diabetes.

- Embecta's decision to discontinue the insulin patch pump program and focus on debt paydown could improve financial flexibility. This is expected to enhance profitability and position the company for strategic investments in higher-growth markets, impacting future earnings positively.

- Potential pricing headwinds as Embecta renews agreements could affect revenue in fiscal year 2025. This suggests potential challenges in maintaining pricing power, which could compress margins.

- Embecta's strategic reorganization, aimed at streamlining operations and reducing costs, is expected to deliver annualized pretax cost savings of $60 million to $65 million. This could improve net margins and overall profitability.

- The impact of foreign currency exchange rates is expected to be a headwind, with initial guidance suggesting a negative effect on revenue and earnings per share in fiscal year 2025, potentially impacting overall earnings growth.

- The growth opportunities in GLP-1 therapies, despite the potential short-term pricing headwinds, could contribute to revenue growth as it aligns with evolving medical administration methods that benefit Embecta’s products, aiding long-term revenue growth.

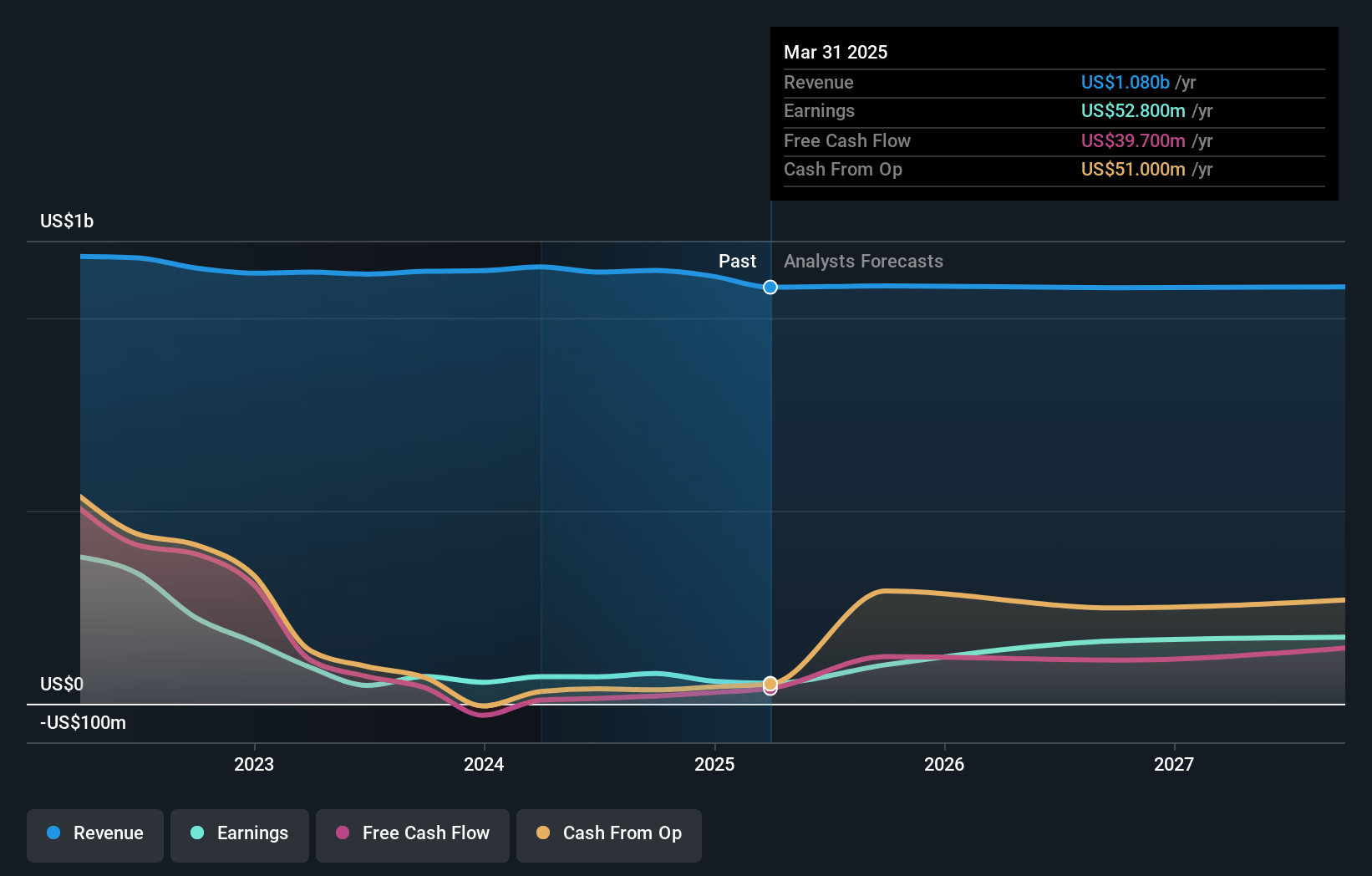

Embecta Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Embecta's revenue will decrease by 0.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.0% today to 16.7% in 3 years time.

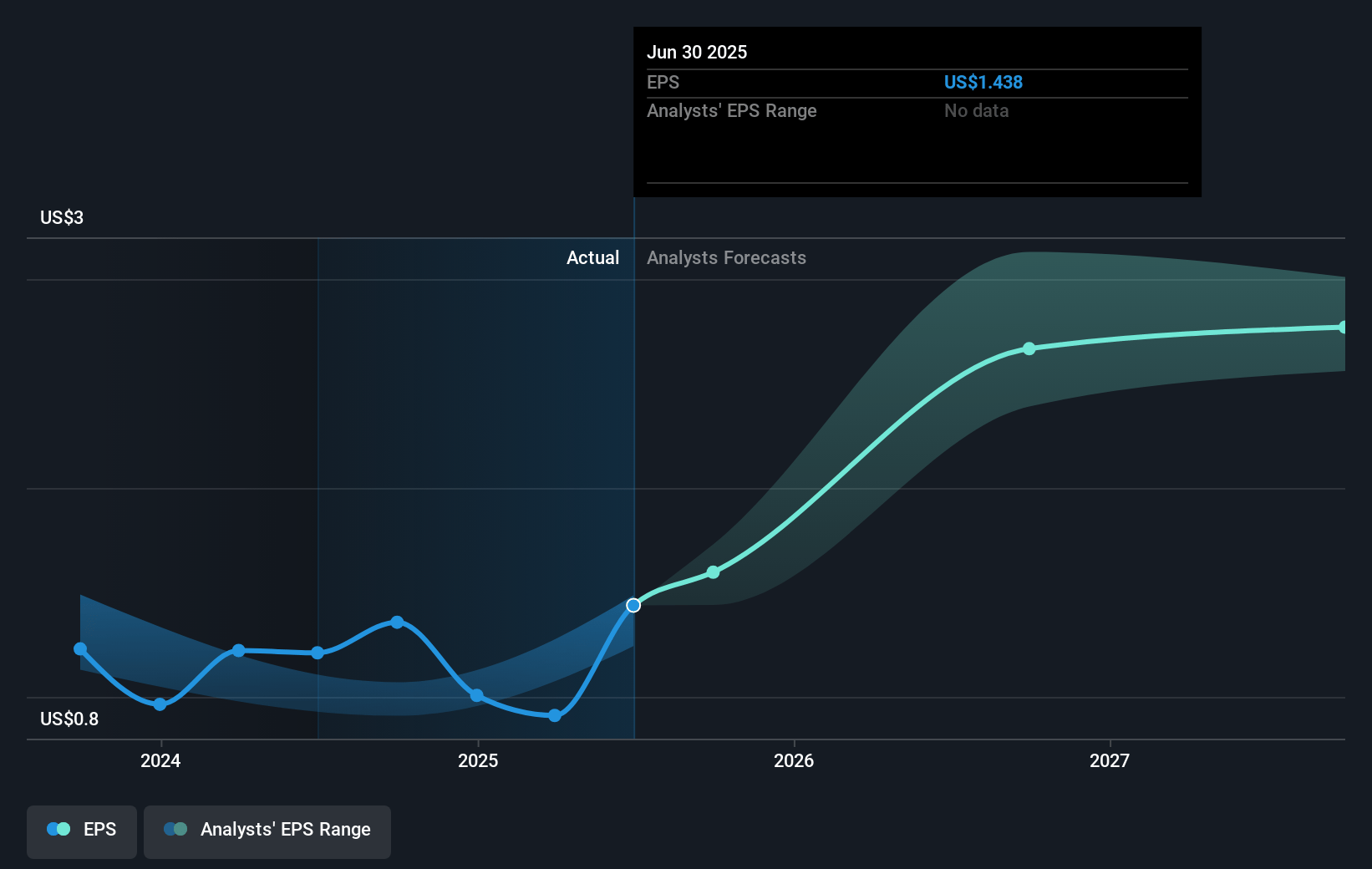

- Analysts expect earnings to reach $190.0 million (and earnings per share of $3.18) by about December 2027, up from $78.3 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 8.5x on those 2027 earnings, down from 14.7x today. This future PE is lower than the current PE for the US Medical Equipment industry at 37.3x.

- Analysts expect the number of shares outstanding to grow by 1.17% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.14%, as per the Simply Wall St company report.

Embecta Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Embecta's restructuring plan aims to streamline operations and reduce costs, potentially leading to improved profitability and enhanced cash flows as a result of savings from discontinuing the insulin patch pump program. This could positively impact net margins and earnings.

- The company's focus on strengthening its core business by deepening customer relationships and maintaining its leading share could stabilize or even increase revenue, especially as it plans to continue leveraging its brand transition plan across various markets.

- Embecta plans to expand its product portfolio, specifically within the GLP-1 therapy segment, which is expected to grow. This expansion could support future revenue growth as the demand for pen-based administration increases.

- The company is prioritizing debt reduction, which could create greater financial flexibility and provide opportunities for strategic investments or M&A. This strategy could help stabilize earnings and enhance financial health in the long term.

- Embecta has successfully increased product prices post-spin, contributing positively to its revenue. Despite expected pricing headwinds in 2025, their ability to manage pricing dynamics could still play a role in supporting revenue and profit margins if similar opportunities are seized.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $21.05 for Embecta based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $26.0, and the most bearish reporting a price target of just $18.2.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $1.1 billion, earnings will come to $190.0 million, and it would be trading on a PE ratio of 8.5x, assuming you use a discount rate of 9.1%.

- Given the current share price of $19.92, the analyst's price target of $21.05 is 5.4% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives